I saw this video posted at SGHardTruth where Minister Tan Chuan Jin points out that with the power of compounding on the CPF, the retirement of todays youths are in a healthy shape. You can take a look at the presentation here.

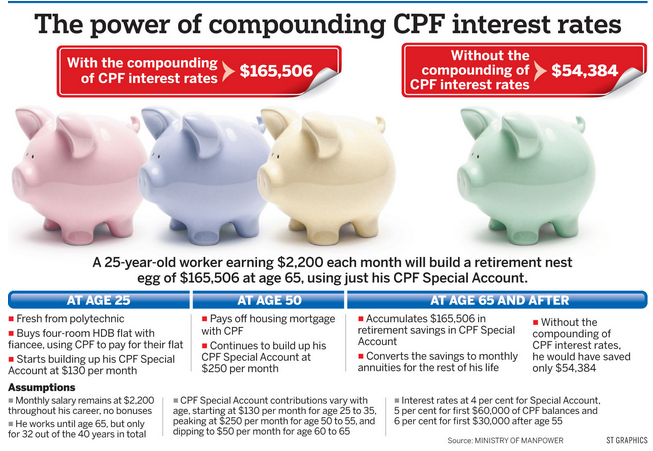

A summary of his presentation as an illustration is shown below:

Here is my take:

- I remained unconvinced that the planners know the situation on the ground other than planning by statistics. In his illustration he cites a person fresh from polytechnic at the age of 25. From what I have learnt from past experience and current, polytechnic students graduate at 19 years old and then serves 2 years in the army. Usually they take the time to study in a local university or a private distance overseas university program graduating at the age of 25. How is it that a poly grad will start work with 4 years of hiatus and not have upgraded?

- In all the narrative of the words retirement, CPF they have to litter with using the CPF to buy housing. If the purpose of a HDB flat is to have at least a dwelling over our heads, and we are spending the best part of our human capital period on repaying mortgage, and not building up wealth, isn’t this not heeding the advice of compounding? The problem with housing is that it is not cheap, most are not prudent in managing their take home pay, and thus other than CPF Special account, they don’t compound their money out of it.

- There are some assumptions provided, that there isn’t any salary increment for the poly grad, and that compounding can accumulate a retirement savings of $165k at the age of 65. That argument does not look very assuring, considering the minimum sum then would be $521,926 at 3% inflation growth over 40 years. Since majority of the CPF OA is going to repay mortgage, will the person build up to that amount? Either this wasn’t put down as an assumption, or that the minister’s guys make a boo boo using today’s figures 40 years from now.

This isn’t really convincing. To make the matter worst, Wilfred Ling, an IFA provides this tidbit in his assessment of the CPF Changes:

What did not change is that the solvency of CPF Life is not guaranteed by Government. I wrote to Straits Times to complain about this ridiculous feature of CPF Life and the Ministry of Manpower replied stating that CPF Life members bear all the bankruptcy risk by having their CPF Life payout reduced. To me this is terrible from financial planning stand point.

If the CPF life annuity is to provide a floor to take care of necessities to hedge longevity risk, having an annuity where the first payout is the ceiling and that there is a chance due to bankruptcy the payout will go down, this really is not a very assuring thing, and seems to me like a potentially deflationary annuity.

To get started with dividend investing, start by bookmarking my Dividend Stock Tracker which shows the prevailing yields of blue chip dividend stocks, utilities, REITs updated nightly.

Make use of the free Stock Portfolio Tracker to track your dividend stock by transactions to show your total returns.

For my best articles on investing, growing money check out the resources section.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- New 6-Month Singapore T-Bill Yield in Late-April 2024 to Drop to 3.70% (for the Singaporean Savers) - April 18, 2024

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024