On 21 November, Channel News Asia reported a record sale for a HDB Terrace.

The terrace home in Jalan Bahagia, categorized as a 3 Rm HDB Terrace, was sold for S$1.185 mil. The home is 237 square meter and its land lease has only 52 years left.

Much of the discussion about this transaction is how stupid are Singaporeans to pay so much for this terrace home.

When I first heard about this, I thought it is still workable. It does not sound like this terrace was purchased by a buyer who do not know what he or she is doing.

However, when I examine the numbers, I started to think may be there isn’t an investment rental case for this.

Challenging to Secured a Loan for such a HDB Terrace

I think it is damn challenging to purchase this terrace due to its short land lease.

If your flat has a remaining lease of less than 60 years, there is a limit to how much you can use your CPF OA to finance this home.

1. No CPF can be used if the remaining lease is less than 30 years.

This purchase does not violate this rule.

2. A flat owner is eligible to use his CPF savings for the flat only if his age plus the remaining lease of the flat is at least 80 years.

Ok so suppose the person is 35 years old, so 35 + 52 = 87 <= Eligible.

If you are 28 or below, you cannot use your CPF savings for the flat.

3. The maximum amount of CPF savings that can be used is a percentage of the lower of the purchase price or the value of the flat at the time of purchase. The percentage is computed based on the remaining lease of the flat when the youngest eligible member using CPF reaches age 55.

So if I am 35 years old, I have 20 years till I am 55 years old.

The remaining lease then would be 52 -20 = 32 years.

So the maximum CPF savings that I can use is 32/52 x 1.18 mil = 726k.

So you will need 1180 – 726 = $454,000 in cash to finance this.

To compound the matter, you might find it challenging to secure a bank loan for a property with less than 60 year land lease.

Given the price, it is likely to be purchase by someone with deeper pockets.

The Return on Investment struggles to Make Sense

My original thoughts is that there should be a value point somewhere. This value point is such that your purchase price earns a respectable internal rate of return, after factoring the maintenance and operating expenses.

When I check the HDB transactions, the typical rental per month for that area ranges from $1,200/mth to $1,800/mth. Those are typically 3 Room HDB rental rates.

If I were to compute the internal rate of return based upon:

- 1200-1800/mth gross rent x 10 months (the typical property agent assumption)

- start only after 5 years minimum occupation period

- rental growth of 2%/yr

- a limited lease of 52 years

The following is the XIRR:

- 1200/mth: -0.50%

- 1400/mth: -0.03%

- 1600/mth: 0.38%

- 1800/mth: 0.76%

So from a rental perspective it does not make much sense. My suspect is that all these were 3 room HDB rental and not terrace rentals.

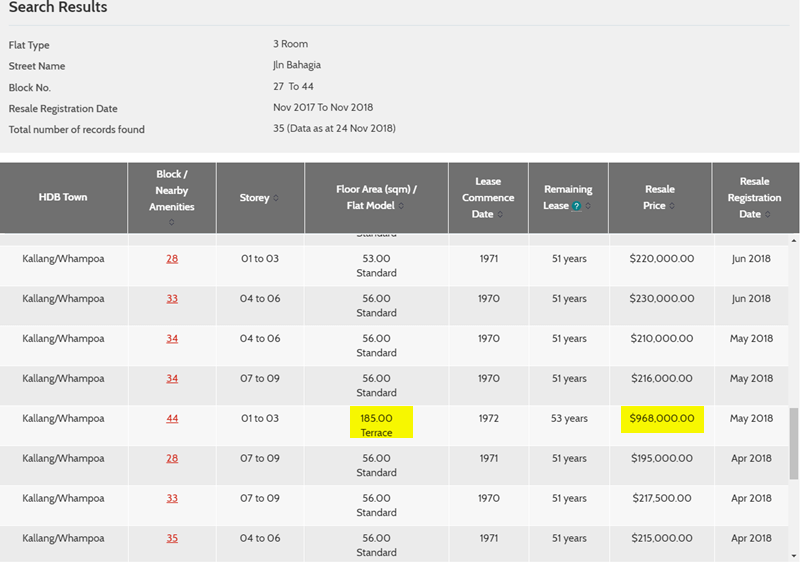

If we look at the recent resale transactions for the year, we can find a similar deal in May 2018 going for $968,000. Thus, it is not just one stupid person but that these folks sees some value in these terrace HDB.

Some of the latest transactions were cheaper at $700,000++ but their size are also halved the previous one.

I thought I missed it but behold, the 1.18 mil terrace. If we compare the size, this one is truly unique. Its much bigger than the rest, and perhaps why its price is higher than the 185 square meter one.

There were no rental transactions, which I could compare with. However, on SRX, we did find a rather old listing, or some agent trying to rent out a terrace:

This terrace is 103 sqm which should value it at $800k++

This terrace is 103 sqm which should value it at $800k++

This rent looks doubled, and if I were to compute the internal rate of return, the XIRR is 2.50%.

If I look upon this terrace as a bond that I could not get back the principal, getting a 2.50% does not seem like a great reward. Not to mention that I will have to manage tenants.

Using it as a Live and Work Concept

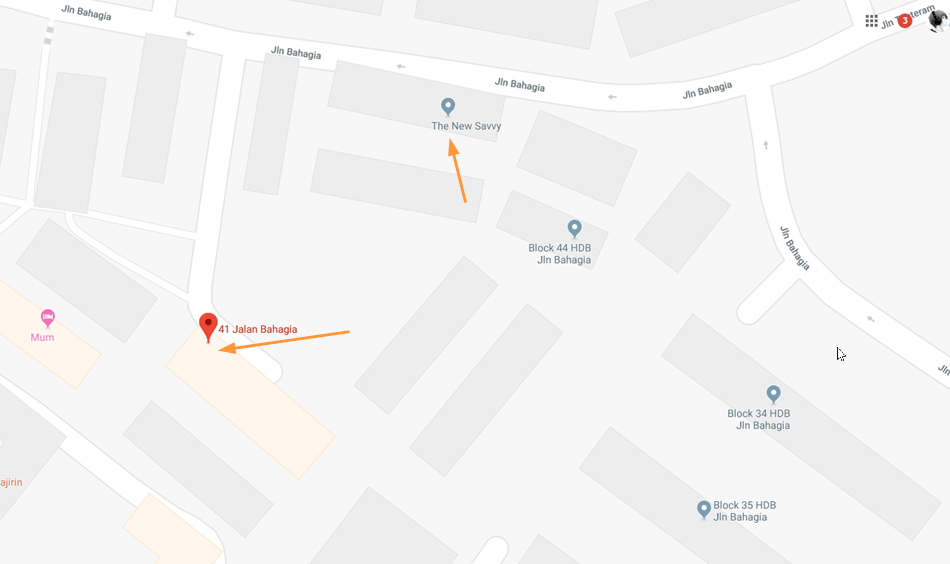

I was not familiar with the area so I didn’t notice it.

But as I searched to find where is this HDB Terrace, I saw a familiar office pop up on the map. Turns out that our friends at The New Savvy is pretty close by.

It then occurred to me that perhaps what appealed to the buyer is to make use of the HDB Terrace as his or her work and live premises. The new owner had the choice to rent or buy.

If the owner chose to rent, she could not retrofit the place to a configuration conducive for work and live.

Thus, by buying the premises, she could pay the 52 year rent upfront.

If she doesn’t get the place, an investment in nearby offices might cost more than this. And she would have to get another home to stay at.

The total cost of long term office rental plus home for living, might be more than this.

With this, she could optimize the space, her needs for living and work.

So this might make sense.

If this place is permissible to be used as a home office, then those folks saying its stupid might not have ponder deep enough.

What is the XIRR for the Non Terrace Jalan Bahagia Flat?

While we are at this, why not see what is the XIRR if I were to purchase these flats, with 50 year lease left, and rent them out after a 5 year MOP?

The average resale value for the 3 room looks to be $210,000.

Since I am 38 years old, by 55 years old, I would have used up 17 years of lease. The lease left would be 50-17 = 33 years.

So I can only use 33/50 x 210000 = $138,600 from my CPF.

I would have to come up with the remaining $71,400 in cash.

If I were to compute the internal rate of return based upon:

- pay $210,000 for the home + $50,000 for renovation and furnishing

- 1200-1800/mth gross rent x 10 months (the typical property agent assumption)

- start only after 5 years minimum occupation period

- rental growth of 1%/yr

- a limited lease of 50 years

The following is the XIRR:

- 1200/mth: 3.87%

- 1400/mth: 4.58%

- 1600/mth: 5.22%

- 1800/mth: 5.81%

Looks like a decent XIRR but I wonder is it better to buy this or just put in a portfolio of dividend stocks.

You let me know about your choice if you were in my shoes.

Do Like Me on Facebook. I share some tidbits that is not on the blog post there often.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Createwealth8888

Monday 26th of November 2018

Public transport is not so convenient at that location.