Imagine you are 38 year old. You hate your job.

You been working in this industry for the past 14 years. Having been in this industry for some time, you realize that you have hit a plateau in your scope of work. If you move on to another job, you be subjected to the same stress, just that the amount of work, responsibilities would be slightly different.

If you stay in the current company, 6 months down the road, the management will make the decision on where the regional technical office will be: Singapore or Malaysia.

You tell your wife you had enough.

Jumping into the healthcare IT industry seems daunting, both in terms of not knowing what you are getting yourself into, and having to rebuild your domain and connections all over again.

However, you can take it because you could rely on your $300,000 dividend portfolio giving $18,000/yr in residual cash flow if you need to supplement your work income if you need to. Plus, your wife is still working.

How possible is the scenario above? The work situation is very possible. Having a dividend portfolio generating 6% in dividend yield is rare among the mainstream crowd.

However, I do think that your wealth can be rather functional even before you attain the amount needed for retirement.

And perhaps, advocating folks to save for retirement, forces people to choose between solving an immediate pressing need (providing financial peace of mind) versus a longer term one, that are at risk of not happening (retirement)

Vox media has an interesting piece written by E.J Roller titled My Parents give me $28,000 a year.

And I find that in a certain sense, it explains how functional your wealth could be, before the retirement stage.

Ms Roller shared with us her experience as a person struggling with a career in the arts. Not just that, her wife is also in the career of the arts and so are a lot of her peers. The article starts off when Ms Roller asks her wife if she would advise a student from a low income background to pursue a career in the arts to which her wife replied she would.

Many financially savvy folks would have warned their friends from committing a large student loan to major in an arts subject. This is because they think that it is very difficult to make adequate money in the field of the arts, even if you have a very reputable university degree.

It gets worse, when you have friends like my friend Chris, who would even go to the extend of providing monetary incentives to his children next time to take up a technical degree or certification such as CFA.

The article took a sharp turn, when Ms Roller’s wife told the audience her parents gave her $28,000/yr as a recurring gift.

Now at Investment Moats, I often encourage you to create self-funded wealth machines. There are the folks who have what we called Bank of Mom & Dad. In the case of the writer, this is the case.

And the article explains to us, from her point of view, the immerse upside of having $28,000/yr on a recurring basis.

After reading the whole article, Ms Roller’s parents over her young adult life have given her some upside:

- Paid for tuition, room and board during undergraduate degree at Yale

- While the school have generous financial aid, writer does not qualify and had to pay a 4 year $180,000 tuition fee. So she graduated debt free versus 71 percent of American students who graduate with student loans

- Funded the remainder of her MFA in musical theater writing at New York University ($70,000)

These are one time only.

And in very rich Singapore, you can see a lot of parents giving you that upside. By not having a huge debt to clear off, it allows you to contribute your disposable income to other life’s milestones instead of clearing debts.

I would say, a lot of people do not have the support of a wealth machine churning out $28,000/yr, but if you do, Ms Roller explains a list of potential financial anxiety that the cash flow helped alleviate:

- When her boyfriend suddenly left, she had to pay a $17,400/yr rent, excluding utilities on her own. Her work-study position could not cover basic living expenses. The $28,000/yr came in very useful

- Instead of working 50-60 hours a week like her peers in a low income state, she was able to work 20-30 hours only per week. She was able to mesh 20-30 hours of reffing adult sports league, “match making: for a dating company, typing payroll for a law firm, coordinating a youth tennis league

- The time saved allows her not to miss career enhancing opportunities such as workshops, unpaid internships, teaching artist residencies

- She was able to have more time to write

- Covered emergencies such as a hard disk crash and upgrading to Macbook Air

- Money to pay for recordings and submission fees for workshops and contests

- Does not have to rely on a partner or spouse

The experience that she describes does not really sound like the financial independence lifestyle that financial bloggers like to put out.

And she did struggle:

- She still has to work in jobs that is not what she is pursuing

- She still needs to build up her resume and network over time

- She has to remain frugal and not eat expensive meals, shop at the cheapest grocer, almost never shopped for clothes

- Those are areas that her parents could not give her.

The gifted cash flow alleviates her of worrying about the basic necessities on life.

The Pursuit of Building Your Wealth Machines increases that Financial Security

The $28,000/yr recurring gift provides in my definition, financial security.

In financial security, it doesn’t mean you lead the best quality of life. By alleviating the most basic and necessary aspect of living (according to the Maslow’s hierarchy of needs), it allows you to focus on what I would call, meaningful struggles.

In Ms Roller’s case pursuit in theater writing is a struggle that she voluntary put herself through. Meaningful struggles do create joy when you overcome it. It may be why so many folks run half marathons and triathlons. Those are painful, but to those who understand them, its a struggle that they volunteer for and if you overcome it, it brings immerse satisfaction.

Rich parents create a trust fund for their kids.

We cannot choose our parents, but we may have the chance to create something similar.

University have their own endowment funds, which is funded by donations. The manager of that endowment have to grow and reserve this sum of money. They have to have a system of spending so that they do not overspend and kill their endowment fund.

In a certain sense, my concept of different wealth machines are similar to the concept of an endowment. Perhaps I should just called it a personal endowment.

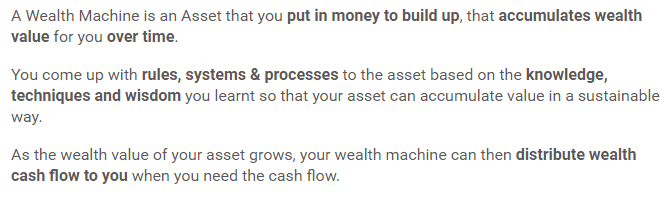

Here is a description of what is a wealth machine, lifted from my article on wealth machines here:

To explained the graphics using an example of a wealth machine based on a passive portfolio of exchange traded funds:

- You spend some years doing some aggressive wealth accumulation by putting a large part of your personal free cash flow from your disposable income annually into a portfolio of exchange traded funds (ETF)

- The ETF grows at a compounded rate of return

- Over 15 years you might accumulate $400,000 worth of ETF portfolio value

- When you need, you could spend part or all of the dividend income from the ETF portfolio. Suppose the ETF portfolio gives 3% in dividend income so that produces a wealth cash flow of $12,000/yr. If this is not enough, and the compounded growth rate is good, you can choose to sell some of the units of ETF to generate a further 0.5-1% in wealth cash flow

If you have not identify your goals or no concrete plans, your wealth machine accumulates to provide some financial peace of mind (read the importance of financial peace).

Just as Ms Roller’s case, $12,000 to 15,000/yr isn’t going to give your family comfortable living. However, it might take care of the bare necessities such as rent, utilities, food.

It is very suitable if you are working on something but the cash inflow is very volatile:

- Switching field of work. Going back to be an apprentice

- Starting a potential business

- Making a job switch to a commission based one

- Going back to school, then starting off as a junior again

- Making a job switch in your late thirties

Even $100,000 has a lot of Utility

I would contend that even if your wealth machine(s) do not provide a sizable wealth cash flow now, it can be very useful for the situations listed above.

$100,000 could potentially allow you to sustain 5 years of survival expenses before being totally exhausted.

And 5 years is lengthy enough for you to struggle, and work something out.

However, you have got to make sure that whatever that you decide to do, there needs to be a positive financial outcome to it.

Unlike the ETF example I have given, you are spending down the actual capital, which means your capital is not intact, and you would have to find a way to re-accumulate the wealth back.

Make Positive Use of that Privilege you are Given

Whether your parents provided you a trust fund allowance, or that you worked hard to create your own site of wealth machines, it is important to recognize that privilege.

When you are a recipient of this privilege, you are probably defined by what you do with that stream of cash flow over time.

For Ms Roller, her parents told her to take this gift as an “investment”.

And what she did was to ensure that the money they provided her, eventually reaped a good return on investment.

Now that the couple is self sustaining, she said that they could passed off that cash flow gift to others.

Even if you worked hard to create your own wealth machine(s), you probably need to acknowledge that while we worked hard, you were on the receiving end of some privileges, and you are defined by what you do with your result.

Her story was rather positive because she showed what an alternate stream of cash flow can do to a person with a challenging situation. Had this be about how parents paid for her college, her post grade masters, so that she could go into investment banking, you would be wondering how come Kyith will bring up this “Ah Sia Kia” story.

Summary

There were a lot of times that I felt that the mainstream media couldn’t articulate well the utility why we channel our personal free cash flow into build wealth.

And hence people do not see why they should choose to defer their spending to a later time when it is so clear spending money today brings higher personal utility to our lives.

If you do not see the utility of retirement, and that goal requires you to defer so much of your cash flow, for so long, then it is no wonder we do not put away money for the purpose of retirement.

I think the concept about saving for retirement is broken, yet the mainstream media is still asking for us to save for retirement. It would be better articulated to build your personal endowment fund that gives you security, and over time supports what you wish to do in life.

Essentially, this is what most middle income people should be modelling after because:

- retirement is not high on their agenda

- they might have some goals, plans and dreams that they wish to get fulfilled now

- they might want to fulfill #2 in the future instead of now

- they might not have a good idea what is their goals, plans and dreams now but in the future they might need money for it

- they have no idea how much they need to fund #2 to #4

You might or might not realize it, but #2 to #4 should be something that you eventually feel strongly about. And chances are, these would need some cash flow to support.

Do Like Me on Facebook. I share some tidbits that is not on the blog post there often.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Gracd

Monday 19th of November 2018

Hi Kyith. I like your advise and write up. I tried to subscribe a month ago but I’m still not receiving any emails. Can you help?

Kyith

Monday 19th of November 2018

Hi Gracd, what is your email address perhaps i can take a look.

Jenny

Sunday 18th of November 2018

Hi I can’t seem to receive your updates after you change platform ..

Can you add mi again?

Kyith

Monday 19th of November 2018

Hi Jenny, were you able to receive the most recent articles?

Kyith

Monday 19th of November 2018

Hi Jenny, I think wait for 1 day. i am also befuddled why its not sent out.

Jez

Sunday 18th of November 2018

That was a good write up. Cuts to the point quickly with a real life scenario of retrenchment and loss of income. The GIG economy is here to stay.

Building passive income from an early stage of life is crucial and having mom & dad's leg up is certainly a privilege. Yet few recognise the importance and significance.

It is very difficult for anyone below 25 to resist the temptation to buy a new device, clothes, basically to spend and consume rather than to invest. It is just too far down the road and the gestation period is usually very, very long.

Setting aside $1,200 plus dollars to buy 100 shares in OCBC is a big chunk for most 25 year olds and even 35 years old. But it is doable as long as they believe in the concept. Faith & trust rules here.

However, when approached by a long lost classmate offering life insurance ( endowment or investment linked of course )... they fall into the life-long payment of premiums. Sigh.... then again that's how life unfolds....

Thanks for all your writings and sharing, one of the very few writers that are sincere as demonstrated by your lack of promoting bad products. You are a good man Kyth.. xxx

Kyith

Monday 19th of November 2018

HI Jez, thanks for the sharing. I try to do my best. those below 25 can resist if they have it for some times. its a lot about prioritization of what is important to a person. for sure when you are that age, studies come first haha

Mathieu Monic

Monday 19th of November 2018

Hi, strongly agreed with the last paragraph. Avid reader of your writings for over a year now.