My private hospital and surgical health insurance (H&S) premiums have been through the roof.

So much so that at the age of 37, I am partially paying cash with it.

And now, the health ministry announced that those who are on these H&S plans with comprehensive rider that covers all the cost would have to share the financial burden with the insurance company.

I am not sure whether I am affected. I do have a rider that covers the co-insurance but not the deductible. Based on what is written, it seems I am affected.

I do know one thing. I am not happy about it.

The Hospital and Surgical Insurance (H&S) is a critical fundamental protection that you should be aware of.

The government knows this, and thus in Nov 2015, they mandated that all Singaporeans are at least covered under Medishield Life, the default H&S plan. This covers H&S if you stay in restructured government hospital ward C and B2. This covers even those people that have illnesses or aliments that will be excluded in public or private H&S coverage. In exchange, the premiums paid by the pool of assured (you and me) all increase, with those previously have exclusion paying a higher premium.

Our healthcare scheme of Medisave, Medishield have always been respected in the international arena. However, if we are not careful, it may degenerate into the same healthcare nightmare other countries are facing.

How the fish did we arrive to what transpired on 7th of March 2018?

Let me try to deconstruct this from what I remember off the top of my head, why we are in this mess, and who got us here.

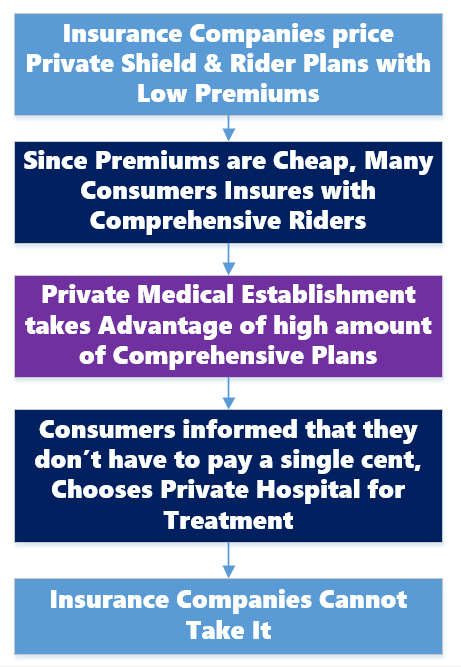

Insurance Companies Used to Provide Comprehensive Plans

Back before H&S Shield plans were privatize, insurance companies used to carry comprehensive insurance plans that assure that you do not have to pay $1 of your medical bills.

However, the premiums paid was not cheap.

These comprehensive insurance plans in this case has to be sold by the advisers because it was not so widely known back then and since the premiums are not cheap, those that were able to pay form what is a smaller pool of clients. They pay for what they get.

Private Shield Plans came Along…. with Lower Overall Comprehensive Premiums

Then government allow the private insurer to provide higher coverage for the Medishield Plans. Premiums of these private shield plans from Aviva, Great Eastern remain cheap.

If I remember its always the smaller insurers who pushed the envelope of what kind of coverage that they can offer. Soon, Aviva became the first insurer to make a lot of the categories ‘As Charged’ (this is in 2005), thus ensuring that for a lot of line items like daily room charges are covered by the private shield plans. Then all the large insurers like AIA and eventually Prudential jumped in.

The premiums are higher, but still affordable.

During this period, the insurance company decide to upsell you and me by providing riders that cover 2 areas.

Now the usual H&S shield plan wants you to co-share part of the medical cost.

Extracted from Great Eastern

So there is a deductible lump sum of $1,500 to $5,000 depending on the grade of hospital services you make use of (C,B2, B1, A, Private)

There is also a 10% co-insurance that you need to pay as part of sharing the cost.

This co-insurance can be bigger, or smaller than the deductible.

For example if your total bill after all subsidy is $3000, 10% is $300.

However if its a transplant, the bill might come up to $250,000. 10% is $25,000.

The H&S shield works best to take away the large catastrophic inpatient and outpatient costs. The assured shares this cost together with the medical providers.

It used to be the case that the old Medishield don’t work so well. After Medishield, you still pays a large part of the $250,000 medical cost. Thus there was an improvement to what it is now.

The private insurers then offer riders that cover the deductible or the co-insurance or both. From what I understand from my most recent adviser, only a few offer you the choice of either covering either deductible or co-insurance.

With these riders, the assured can pay the annual premiums and be covered without having to pay a single cent.

And the overall premiums are lower than the old comprehensive full coverage insurance plans. Thus the old plans could not survive and die off (are you still on this plan? If yes, do hit me up on the comments and let me know your experience with them)

These riders + private shield plans have affordable premiums. This is especially so when most of those who signed up are in their early 20s when they are still adulting and those in the 30s.

Even the most comprehensive plans that cover all the cost in private hospitals are affordable.

The take up rate is high.

Senior Minister of State for Health Chee Hong Tat said 29% of Singapore residents are on these full riders.

The Economic Bias of Private Medical Establishments

Doctors is suppose to solve our health problems.

However, how they go about doing this is debatable.

The Medical profession do have an economic bias to be more profitable.

Many of the local medical companies are listed on the SGX such as:

- Raffles Medical

- Singapore O&G

- Talkmed

- Q&M Dental

- HMI

If you are an investor, you would invest in these companies because their free cash flow, profits are increasing year on year. The more medical establishment they open up, the potential for higher free cash flow, the higher their stock price goes.

Since the owners of these medical companies have stock options or stakes in their own company, they have a greater economic bias to ensure they have higher revenue.

If their clients do not have to pay a single cent on their medical bills, it becomes a great opportunity to:

- recommend procedures that are helpful for the patient but would otherwise be expensive

- increase the number of checks ‘just to be more certain’ but would otherwise be expensive

The clients don’t feel it since all the cost is borne by the insurance companies.

Pamphlets that inform clients that they are covered by the H&S plans. My friends share with me their experience in private hospitals where they go in for a simple procedure, incur a large medical bill but its all paid by these comprehensive riders and H&S shield plans.

However what they notice is that on the wall of these hospital, there are posters educating the clients how to claim from the insurer and that all these are comprehensively covered.

This gives assurance to the clients that they can have peace of mind to pursue the best course of action and not worried about the bills.

Listed Medical Establishments Marketing their Business to Retail and Institutional Investors. As retail investors, you just have to go through the financial statements to see how lucrative the medical industry is.

However, as the management of these companies, you will still need to provide evidence to investors that there are good future growth ahead.

In some of these sessions, the things that explain seem to be indirectly thanking Ministry of Health on recent rule changes that enable them to bring their financial figures in line. This allows them to charge near the MOH average.

Since MOH average cost of line items can be somewhat optimistic, bringing their charge rate to that would be a boost to their business.

The usually Cost Conscious Consumers is unleashed

When my mom got cancer, I distinctly remember the lead associate professor in NUH ask me, does she have a critical illness coverage.

That could be just trying to help this seemingly uneducated engineer make sense of what he must do in this trying situation but it could very well be whether I can afford some experimental drug.

I also have friends that encounter the same kind of check from their doctors “do you have private insurance coverage?”

Now I am not sure this is wrong but it seems if there is a way of curing the person but the cost is too high, they would not tell you. They probably do not wish to put a dilemma on you whether to break your bank and take on efforts to save yourself or your loved ones and end up in dire straits.

At the same time, since you have already pay for a private insurance that lowers your cost to zero, and you love yourself or your love one enough, why not just go with the one that is the most appropriate, gives the best result?

However what is most negative is that people used to have different grade of health insurance. If they are more well to do they go for higher grade of care in private hospital. If they are less well to do, they go for lower grade of care in lower class government restructured hospital.

When the higher grade is affordable to even those not so well to do, what happens? People don’t choose people go for the best.

And there are the Kiasu (afraid to lose) Singaporeans who will say pay already just take the best la!

The Insurance Companies Cannot Take It

What happens is the insurance companies have to pay out more claims then the premiums that they take in.

In last year’s Sep 2017 Business Times article, it was reported that despite the hiking of the premiums paid for the integrated shield plans, all insurance companies suffer underwriting losses in 2016.

AXA got in at 2016 and started their tenure suffering losses (God knows their reasons for getting in. Must have been a great lead generation tool).

The big insurance powerhouses are AIA, Prudential and Great Eastern.

NTUC Incomeshield is one of the cost effective and popular plans among the community. Aviva was one of the pioneers that pushes for many changes.

Firstly, see how problematic Aviva is. (disclosure: yours truly is on Aviva). They likely have a smaller customer base and as the amount of claims go up in a year, they cannot spread the cost around. From what I understand Great Eastern, together with Aviva have some of the more expensive shield plans, but on and off they do suffer from underwriting losses. That, despite them being one of the big three insurers.

What is noticeable is that AIA, Prudential have been doing very well but in 2015 to 2016, even they also suffered.

Between 2005 to today, the percentage of claims ratio, with respect to the insurance company’s cost on the product went up from 42% to 84%.

- In 2013 the insurance companies review their private H&S premiums

- In 2015,Medishield Life was rolled out. The insurance companies agreed to freeze the premium of the main H&S plans for a year but not the riders

- In Nov 2015, Prudential raised the rider premiums by 5-35%

- In Apr 2016, AIA raised the rider premiums by 13-35%. Aviva increase by 30-60%

- In Oct 2016, NTUC Income increase. Only GE didn’t raise the premiums

- When the 1 year freeze on H&S plans expired, Prudential, Aviva and AIA raise the premiums on their H&S plans covering private hospital treatments and stays. Not long later NTUC Income and Great Eastern also raise their premiums

- Prudential raise 5.6-13.4%

- Aviva raise 10-25%

- AIA raise 2-23%

- NTUC raise by 5-15%. They also raise the rider by 10 and 30%

- GE raised by 2-4.2% for all categories except B1

- In Jul 2017, AIA raised the rider premiums by 18-54%

- In Oct 2017, NTUC Income raised the rider premiums by 8-35%

On 7 Mar 2018, 6 insurers appealed that their customers should co pay at least 5% of the treatment costs EVEN if they bought fully comprehensive riders.

Shortly in the day, Senior Minister of State for Health Chee Hong Tat announced that if you are going to purchase a new H&S shield plan rider, you will have to co-pay 5% of the cost. This is capped at $3,000. The $3,000 limit was placed so that they would not suffer from catastrophically large hospital bills.

The people most affected are those who are thinking of getting comprehensive H&S coverage. They will transit to the new rider in Apr 2021.

What went Wrong Here

This seems like some kind of circle jerk culminating to the insurance companies having to raise their premiums and proposing that we should co-pay the cost.

As a consumer I am not happy about how this healthcare situation turned out.

Here are areas I think are culpable for this problem.

1. The Government. The government failed to provide the leadership in this instance (and a few others) and have often adopted a wait and see attitude. They did not anticipate well how this domino effect will turn out and provide cautionary measures accordingly.

Mr Chee said this is coincidentally NOT to bail out the insurers but to put the citizens on the best of behavior because a lot of us adopt this “buffet” syndrome. However, this means that they are not doing a good job sensing the situation on the ground and stemming the problem before it blow up.

If they are really competent, and their big data and data scientist are formidable, they would have outlawed full comprehensive plans or put out cautionary guidelines what could go wrong.

Secondly, no one wants to go to hospital. Sure, we might want to take MC just to escape work. I wish to see the data whether these incidence of buffet behavior forms a large majority of the private admission.

It is more likely that more are choosing to go private hospital because, firstly they are suffering some problems, and they chose private hospital because cost became a non issue.

The reason why there are more claims is likely that we are also getting more unwell.

In the same 3 short month that my mom passed away, I have 2 neighbors concurrently passed away due to cancer and I have 4 separate incident of co-workers and friends relatives undergoing cancer treatment.

If you ask me, something is seriously wrong. Its either I am at the age where most of us have parents or peers suffering from these aliments.

Perhaps they can form a task force and see if the big data can tell something. At times, I was horrendously shocked by some of the health campaign advice provided. They seem to be much slower than some of the other countries proposed. Eventually we will adopt their guidelines but everything just feels so wait and see.

Lastly, People would rather go to private hospital to carry out every kind of check because they don’t feel the cost but also that in comparison to government restructured hospital, they get better treatment.

One of my friend just did a day surgery and he said, given the choice again, he would have chosen a private hospital due to better care. This might not be that the private hospital provides better care. It might be that the government hospital care is not up to it.

2. The Insurance Companies. They were the first ones who came up with these policies. To a certain extend, I believe there is a demand for such comprehensive plans. Thus, if you do not provide and your competitors provide then you cannot get good revenue for this segment.

The problem seems to be that they are pricing the comprehensive riders too cheaply. The dilemma here is that if you priced it to factor a lot of the risks, and your competitor is lenient in their pricing, you cannot sell well.

I always felt it strange last time when my friend told me that the older comprehensive plans were more expensive. Why are these riders cheaper. The argument is that you have a larger pool of customers to spread the claims cost, so the premiums is lower.

If you have priced a comprehensive plan as something that I need to consider carefully with my limited disposable income, I would have chosen not to take up the comprehensive plans.

Majority of the citizens would be purchasing plans that they pay the co payment and deductible. There will be less of this buffet syndrome.

So now it becomes the case where they come up with the plans, priced the premiums cheaply to capture part of the market, now that they cannot take it, they tell us we have to share the co-payment.

Like WTF.

Might as well don’t buy comprehensive riders in the first place (to be fair with these recent changes to the comprehensive riders it would cut your large treatment bills to at most $3,000, so there are benefits)

3. The Shareholders and the Management of Private Medical Establishments.

When you invest in Raffles Medical, you are investing because it is a good business. There are ways to run a good business.

You can create more branches, more hospitals so that you can touched people with your services. You can choose to offer alternative treatments that have greater success in solving people’s aliments.

If you wish for higher profits, then the management have to think of all avenues how to do better than last year.

Medical companies typically have more than 20 times Price Earnings.

This is a testament of the defensiveness of the nature of their business.

However, it also mean to generate a better growth it is tough.

If you are mad about the economic bias of insurance advisers, the line between what are morally correct or not is even more fine.

My friend Mr 15 Hour Work Week found some symmetry with what he just read in Nassim Taleb’s latest book, Skin in the Game:

“Beware of the person who gives advice, telling you that a certain action on your part is “good for you” while it is also good for him, while the harm to you doesn’t directly affect him.”

4. You and Me. We cannot escape the blame from this. I have heard of many accounts of friends and family choosing the private hospital treatment. That is not wrong if the reasons are well justified. If Minister of State could raised those examples, and I have my own private war stories on this, that means that a fair share is culpable of this.

There was a lot being said about the escalating insurance costs, but all things equal, if they are escalating it might mean overall we are getting more sick and more sick.

The onus is that we have to take part of the responsibility of not taking care of our health.

If We Don’t Fix This Mess Together….

Then we are going to have a bigger mess.

Many politicians tried to fix the United States healthcare system but its a big challenge. Some where down the line in history, something went wrong.

My understand of the problem is that their healthcare plans are essentially private and not mandatory. This is before the Affordable Care act which tries to make things compulsory (Which the Republicans are trying to repeal).

As it is not compulsory:

- Those who have health problems, and what the insurers do not want wish to get on the health insurance, wants to be insured

- Those without health problems, do not prioritize health insurance when they are in good health. Due to #1, insurance premiums are not cheap. This dissuade them from signing up.

In Singapore, we have the option of going with the minimum government health plan (Medishield Life) or the private enhanced health plans. We are not so bad.

However, in the private realm, if we are not careful, we may get to something like that:

- More and more people are getting sick, making more claims

- Those that have made a claim might stay on the plans, having no choice but to bear the heavy insurance premium

- Those that are healthy after all this, might choose to downgrade

- The result is less premiums earned and at the same time the overall cohort is generally making more claims over time

- The premiums have to go further up

This becomes a domino effect.

To prevent an unsustainable healthcare system, there needs to be an effective plan to make us less sick.

I feel utterly discouraged that we are being blamed for consuming a lot of healthcare when there are bigger elephants in the room. The private medical companies get off freely in this whole mess. The insurance companies can now have a better profitability.

Me?

My premiums are not coming down. And now we are being told we are a big part of the problem.

WTF.

To get started with dividend investing, start by bookmarking my Dividend Stock Tracker which shows the prevailing yields of blue chip dividend stocks, utilities, REITs updated nightly.

Make use of the free Stock Portfolio Tracker to track your dividend stock by transactions to show your total returns.

For my best articles on investing, growing money check out the resources section.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- New 6-Month Singapore T-Bill Yield in Late-April 2024 to Drop to 3.70% (for the Singaporean Savers) - April 18, 2024

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

Rajan

Tuesday 1st of May 2018

Hi Jojo Thanks for your sharing. I am also considering taking up the IP plan however using the B1 plan - would you know if they would allow me to choose my doctor. There is nothing stated in the insurers application.

Timothy Sipples

Saturday 10th of November 2018

When you stay in B1 ward or higher in a public restructured hospital, you can choose your doctor(s) as long as they practice at your chosen hospital — still subject to their schedule availability and willingness, of course. Charges might vary somewhat depending on the doctor’s status, and charge variations can show up in deductibles and/or co-pays, so you should still pay some attention to physician charges. For stays in B2+ ward and below, the hospital assigns qualified doctors according to the hospital’s rotation/staffing rules, whatever they are. You are free to ask for a particular doctor, informally or formally, but the hospital isn’t required to honor your request even if the doctor is agreeable.

Doctors can always ask other doctors for their professional assessments, no matter what ward you’re in. You can always ask a particular doctor to do that, and there’s sense in doing so if you have an unusual condition. For example, “Doctor, you seem to be saying this condition is rare. Could you ask your colleagues whether anyone in the medical community has experience with my condition? I’d appreciate your reaching out to any of your colleagues who have seen this condition before, to see if they have useful advice to offer you.” Most conditions are not unusual or rare, but if you’re the “lucky” one, go ahead and gently ask your doctor in that sort of way.

In Singapore (like other countries), you don’t enjoy the public hospital’s subsidized rates when you simply walk into the hospital out of the blue. Start with either a polyclinic appointment or, if a real medical emergency, the A&E. Then get referred from there to the hospital (if merited of course). Even if you’re insured, it’s still often important to follow that referral protocol. (Carriers are just starting to reduce coverage for unreferred hospital care in their plan revisions, I’ve noticed.) Keep all receipts since all the Integrated Shield plans provide some coverage for pre-hospitalization care that’s related to the hospitalization, and you don’t always (or even very often) know that your polyclinic visit will lead to a hospital admission. For example, Great Eastern’s “as charged” public hospital B1 ward Integrated Shield plan (“Supreme Health B Plus”) covers related specialist outpatient care up to 120 days before the admission (and up to 180 days after), but it has reduced coverage if you didn’t get a referral and thus aren’t enjoying the subsidized pricing.

Jojo Tan

Monday 26th of March 2018

I am insured under NTUC Enhanced Incomeshield with Rider (which NTUC is no longer offering for new clients) for private plan. However as I chose to seek treatment at a restructured hospital, there is a pro-ration clause where NTUC pays a reasonable expenses (which was S$150/day during my last ops few years back, there is no fixed amount stated on their terms) since I was admitted to a hospital lower than my entitlement to compensate for my stay. In other words, I bought a private shield plan but I chose to stay in a public hospital hence NTUC pays me some compensation on per admitted day basis since I did not stay in private hospital which I am entitled to.

Kyith

Monday 26th of March 2018

Ah I see. In that case many of our plans are like this with pro-ration. I tried to take a look at MyShield and it does not seem to have this lower benefit.

Jojo Tan

Monday 19th of March 2018

Even though I am on private plan, I usually choose my treatment based on which specialist can offers me the best advice and not whether private or public hospital. My first choice is usually the Senior Registrar or the Head of Department at SGH. Our political leaders seek treatment there as well hence SGH has very comprehensive medical equipment and expertise.

Private hospital gives me 5-star bed but to me, it's more important to be operated by a 5-star surgeon. Also, I had past experience at SGH and private hospital for the same diagnosis, I can tell you SGH's doctor treatment is conservative style. They will not ask you to go for surgery if it's not required unlike private. The only downside is the waiting time can take a while and crowded at the clinic.

Kyith

Monday 19th of March 2018

Hi jojo, thanks for sharing your valuable perspective. For myself, I would think if we want to get cured, the quality of the doctors matter high. I do note that some friends do share the same experience that its not always government doctors are poorer in grade. My original intention for a private shield is to guard against the scenario that i do not have a choice but to seek a private doctor of repute. Turns out pleasantly that might not always be the case. Even them we would still need some private shield plan to cover a higher grade of government hospitalization.

SeekingPrivateReturns

Tuesday 13th of March 2018

Should have a few more boxes at the end of the article.

---> Insurance Companies cannot take it ---> Govt blames consumers.

E. Ng

Tuesday 26th of March 2019

Agree with this totally! The government cannot control how these private hospital charge consumers so instead of a helping hand to lessen the consumer's load, they are adding on it. All knows Singapore's medical cost is among the highest worldwide. What is the government doing to help the commoners?

Sinkie

Monday 12th of March 2018

I've said many times before that this was unsustainable ... it simply causes 15%-20% annual inflation in private medicine, and similar if not higher inflation in private medical insurance. It will eventually lead to US-style pricing of $20++K premiums for comprehensive H&S insurance.

Frankly, all parties are to be blamed. And yes, I & my relatives have ever been asked the "Do you have full coverage private insurance?" by many specialists. Unfortunately, govt chooses to put the blame squarely on "buffet-crazy" singaporeans.

Insurers, medical providers & consumers all are guilty, becoz all are human ... and humans by genetic evolution are selfish, self-centered with moral hazard behavior. Sorry, this is my default belief of humans, even newborn babies.

However govt has to take the lion's share of the blame, coz they're supposed to operate at higher level consciousness above individualistic self-serving needs. But becoz S'pore govt operates more like corporation, it ended up wanting to have its cake & eat it too --- low healthcare budget/expenditure, leaving too much self-regulation to private companies (healthcare & insurers), promote corporate profits & GDP, passing of costs to consumers who can afford, etc.

Govt allowed the old Medishield to become obsolete & too far behind the curve ... maintaining too low caps on each line item for many years ... ending up the old Medishield could barely cover 40% of the average bill even for C patients.

It should have been much more proactive in guiding Medishield progress & directing private shield plans. 100% coverage riders should never have been approved. Yes, it means more nitty gritty tasks for people in CPF, MOH, MOM and having to say No to the powerful financial / insurance / healthcare industries. But that's why S'pore ministers & civil service are among the best paid in the world --- to do their jobs, and to do them properly.

Kyith

Monday 12th of March 2018

HI Sinkie, a lot of the wait and see, wait too long. its so easy to put the blame on the people being the issue. i agree with the majority you said.