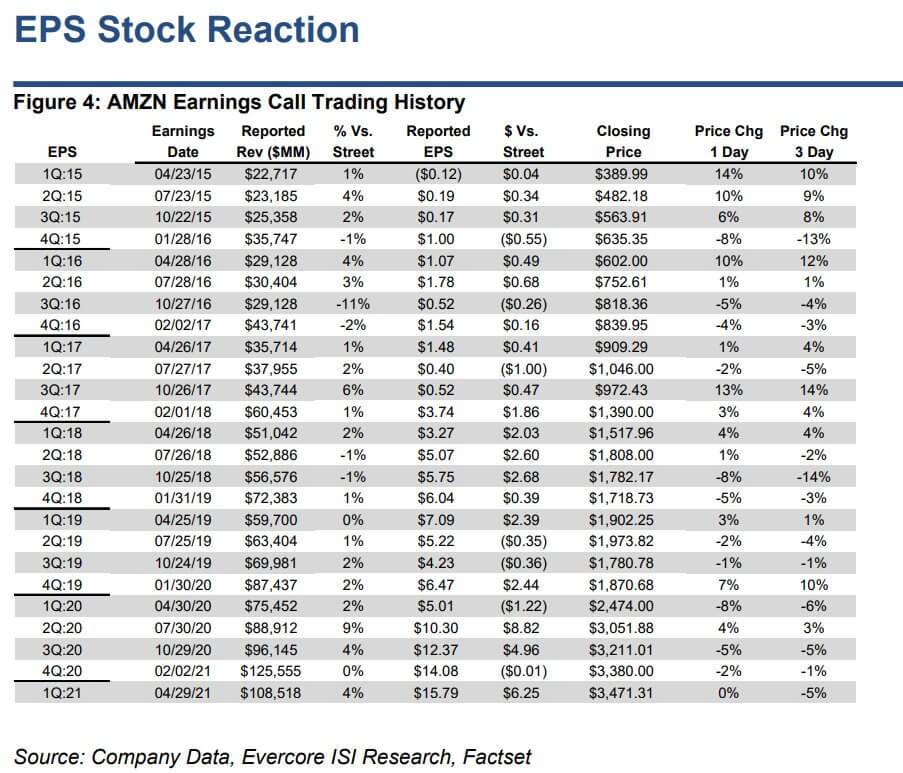

Upon the announcement of their Q2 2021 financial results, Amazon share price fell by about 7%.

I guess many of us were not expecting this degree of fall from an important component of the S&P 500 but actually, this degree of fall is not uncommon for Amazon.

This tweet shows the historical price change for some of Amazon’s historical earnings announcements compiled by Evercore ISI.

There were periods where Amazon’s financial results disappointed analysts and that resulted in a -8% fall.

But is this price fall an opportunity to accumulate more or is there some concern?

The Market is Pricing in a Lower Future Valuation

Amazon’s historical result was great.

For such a giant company, they were able to grow their revenue by 27% year on year.

Net income grew from 5.5 billion to 7.7 billion years on year.

But the intrinsic value of the stock is not what Amazon did in the past but what Amazon will do in the future.

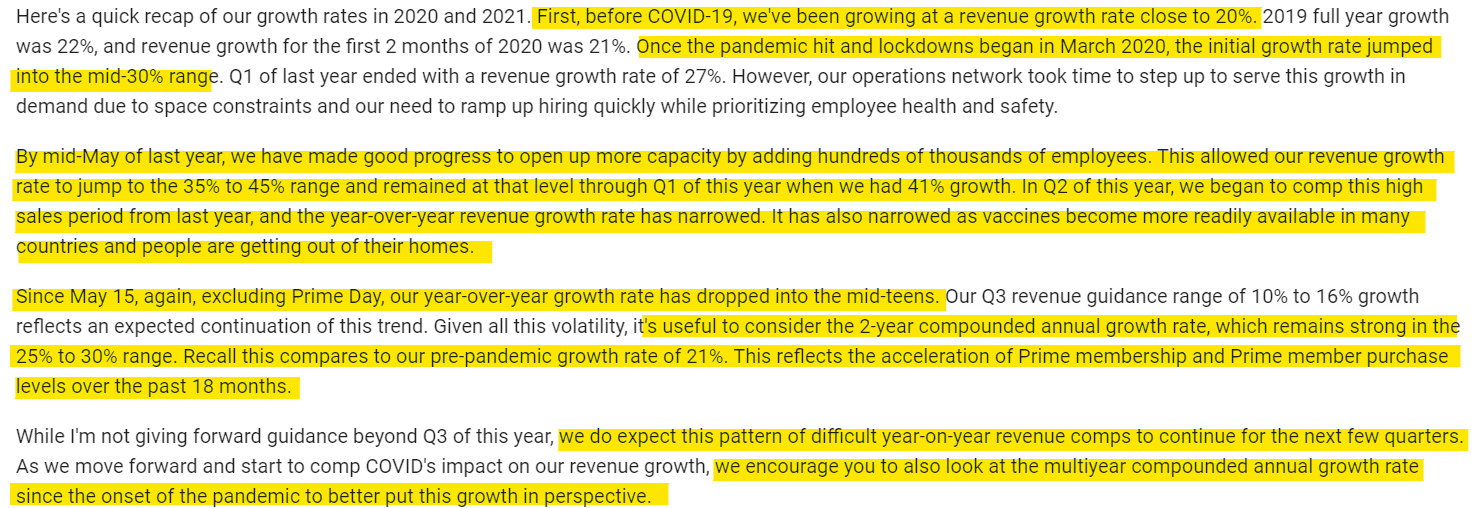

Amazon guided that in Q3 2021, they will generate between $106-$112 billion in revenue. This is much less than than the consensus estimate of $118 billion by analysts.

Operating income is going to be between $2.5 billion to $6 billion versus $6.2 billion in Q3 2020.

This means that Amazon’s revenue would grow between 10% -16% in the third quarter year on year and operating income to be rather stagnant.

The market is pricing Amazon as a growth stock, and when growth seems low, they wack the share price.

The recent earnings results make me realize that market participants expect these growth companies to not moderate the growth that they benefit from COVID.

It is very likely most of these companies are going to face tough quarterly comparisons with last year. COVID have pulled forward years of growth for these companies in a few quarters.

Market participants are behaving irrationally here and that might be our opportunity.

Guidance Creates Uncertainty in Amazon’s Valuation

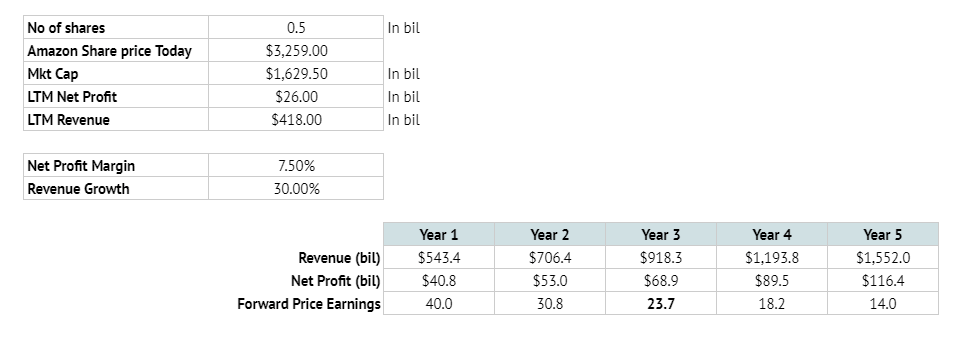

In my last article on Amazon, I explained that some fund managers anticipate that if we value Amazon based on forward earnings, we could get Amazon at a forward price-earnings of near 20 times by 2025.

Amazon current trades at a price even higher than the price when I wrote that article.

If you look at my base case, we were anticipating a net profit margin of at least 7.5% and revenue growth of 30%.

Amazon’s Q3 guidance creates uncertainty about whether the business can grow revenue at 30%. As of now, I think there is even uncertainty whether growth can push past 20%.

I would not say Amazon is expensive here, but that there is less margin of safety. The margin of safety for investors like myself is a high degree of confidence that Amazon can grow at 30% for 3 years at the same margin to reach a state of a mature company.

If Amazon behaves less like a mature company but a company that could still grow, that “growth spread” is our alpha.

It might take longer for Amazon to cut their PE if we purchase it today.

Then again, Amazon’s PE has never been cheap! It is just that moving forward, I got a feeling that there is going to be a shift such that Amazon is more focus on free cash flow than topline.

It gives me the vibe when Tim Cook took over Apple where there is a slight focus shift.

There are definitely some areas for us to remain optimistic about.

AWS and Advertising is Growing Well

I got a feeling that watching revenue might not always be the best thing going forward.

We have to see how well Amazon does in a few segments that are starting to become the cash flow driver for them. That would be:

- Amazon AWS

- Advertising

More and more, I feel that Amazon’s moat is setting up a crazy logistic system that can never be replicated by others. Eventually, the data they know from their own sales on Amazon and through their logistics network feeds into their advertising.

There are also two segments that are pretty important:

- Prime

- Third-party relationship retailing (3P) as oppose to first-party relationships (1P)

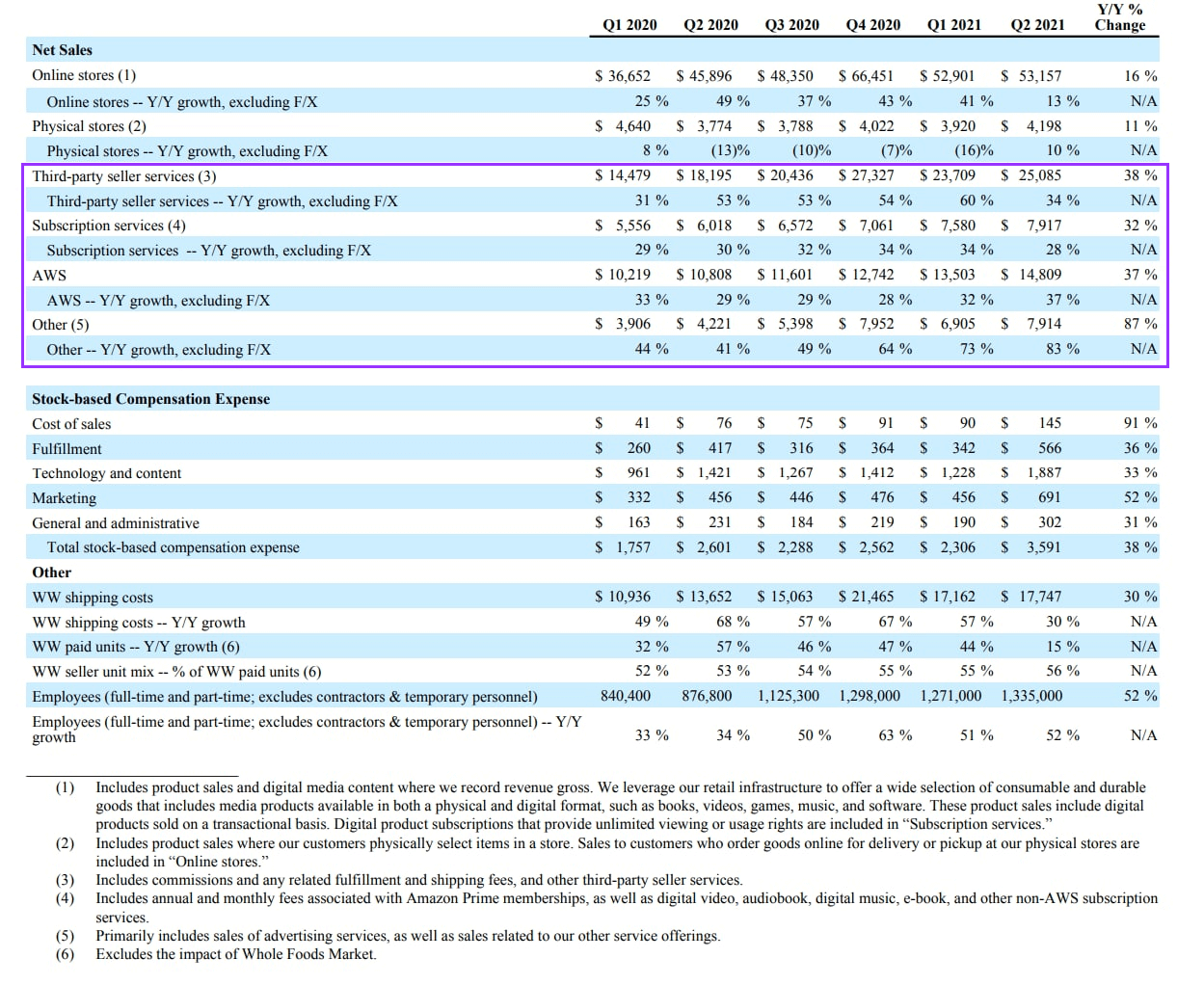

Mostly Borrowed Ideas have a great tabulation that shows the growth of these 4 segments.

The following table show a break down of the revenue growth of the various segment pretty well as well:

AWS’s growth got restored to 37% compared to 29% last year and it looks even looks good compared to 32% Q1 2021 growth.

Others, which represent the advertising is accelerating its growth and likely, this is a high margin segment.

This means that underneath the hood, the higher-margin segments are growing at a satisfactory high pace. 50% of the moderated growth comes from the lower margin online and physical stores.

The advertising engine is starting to become very important.

Intuitively, we think of Amazon ads on their website but advertising can appear in other areas now. They are putting ads on the boxes they deliver to people, ads on Amazon Prime Streaming TV and Twitch.

Sometimes, we have to just give them time and observe if Andy Jassy and the gang continue to do what Jeff Bezos do.

If you want to trade these stocks I mentioned, you can open an account with Interactive Brokers. Interactive Brokers is the leading low-cost and efficient broker I use and trust to invest & trade my holdings in Singapore, the United States, London Stock Exchange and Hong Kong Stock Exchange. They allow you to trade stocks, ETFs, options, futures, forex, bonds and funds worldwide from a single integrated account.

You can read more about my thoughts about Interactive Brokers in this Interactive Brokers Deep Dive Series, starting with how to create & fund your Interactive Brokers account easily.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

- The LionGlobal APAC Financials Dividend Plus ETF Won’t Give Singapore Investors 5% Dividend Yield Always. Further personal thoughts (with some data). - April 13, 2024