Adampak is a label converter with a large client base in electronics,pharmaceutical, petroleum and other industries. I recently took notice of this little company due to the recent gloom for hard disk parts manufacturers from the Thailand flood problems. Many of them were beaten down so I thought why not do a study and the most appealing looks to be Adampak

- At $0.025 payout that translates to a 9% yield

- Average DPU since listed (2005) have been $0.02 translating to a 6.9% yield

- Business is net cash with very strong free cash flow

- How I would describe them is that they are an extension of 3M. Using 3M’s products to customize and serve a wide industry of customers by value adding to their products.

- Their advantage lies in the delicate balance their products sits in their users end product. It is not a large portion of the cost to produce the end product such that the customers would often think about switching. Rather the customer looks at other intangible aspect such as the quality of delivery and reliability and the additional cost should they switch over.

- The opportunities is that whichever industry 3M’s and their suppliers products are used, they can potentially edge in.

- This business they way I see requires a lot of business relationship building and competent sales team.

- Once established, you will need a strong operations to deliver and meet the requirements.

- The threat is that they are not the only ones doing this and that another competitor can readily replace what they do. To increase their sales by tapping other businesses, the relationships may have been established and the same reasons that stops people from taking away their business might stop them from edging in as well.

- They are pretty spread out in terms of profit contribution from various industry, but by their own engineering, hard disks manufacturers Seagate and Western Digital drives 50% of their net profit and the recent Thailand flooding goes to show that this is an opportunity as well as a threat.

(Click to view larger image)

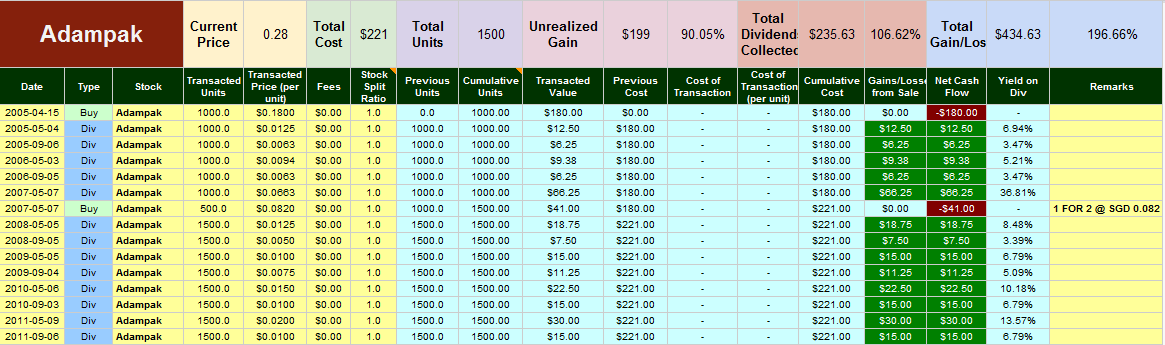

Here is the factsheet for Adampak since listing. I thought it looks pretty good. Went through the GFC but had you been a holder and you have participate in the rights issue your total gain is still pretty good.

How I see the hard disk industry shaping up

Now since hard disk drives a large portion of profits, a lot of folks are talking about how solid state drives (SSD) will replace magnetic hard disks (HDD), which are the hard disks that you guys have been using all these while. Does this spell a big substitute threat to Adampak?

For the less tech savvy folks SSD have a lot of advantages over HDD but have some flaws as well

- SSD have significantly faster reading and writing speed than HDD. You can get Windows 7 boot up in 8 seconds on SSD.

- Consume less electricity

- More tolerant to ambient temperature

- More tolerant to vibration and shock

- Their one fatal flaw is “write endurance”, which means that there is only a finite write cycle for each block.

Judging by the pros over cons why hasn’t SSD taken over HDD? One thing is the cost per byte is much much higher. But in the last 3 years they have narrowed significantly

- The average price of SSD has fallen from $40 / GB in 2007 to $2.42 in 2011.

- The average price of HDD has fallen from $56.03 / GB in 1998 to $0.075 in 2011.

- For SSDs in 2011, the lowest price per GB we have in our data set is $1.50.

- For HDDs in 2011, the lowest price per GB we have in our data set is $0.053.

- In 2007, SSD memory cost 120 times as much as HDD memory. In 2011, that has dropped to 32.

- If a 3 TB HDD would cost as much per GB as the average SSD today, it would cost around $7,260. Right now, the cheapest 3 TB drive on NewEgg.com is $230.

- The current average price per GB for SSD is about the same as it was for HDD in 2002.

Given another 2 years and I am sure it will reach a viable price. Still the way I see it, you need SSD controllers to improve significantly to lengthen the write endurance.

Ultrabooks, Macbook Air, Tablets driving SSD

Now the market for hard disks tends to be segregated to enterprise servers and consumers. I believe the use of SSD as server accelerators Is starting to see a lot of viability. However for enterprise servers the need for large storage due to the movement to cloud computing will mean that there is always a sustain demand for HDD.

However the shift in consumer electronics should see a drift towards flash storage and flash SSD. The Macbook Air in 2011 have been very popular. So popular that all the PC vendors are copying them and producing Ultrabooks.

The trend is clear. Consumers want thin, light and portable laptops. The demand for desktops should see a drop off as the move to App Lifestyle and Cloud Computing reduces the business case for desktop pc for a lot of people.

Adampak likely still very relevant

In such a scenario, what Adampak provides in my opinion can still be brought over to SSD.

SSD will still need adhesive labels similar to that of HDD, which is provided by Adampak. However, Die cut adhesives used as damping could be render obsolete due to the nature of SSD not requiring much vibration protection.

The problem for Adampak is to edge in to this new pie. This is where their sales guys need to do the job well. The SSD players likely will have their own suppliers.

The one thing that would work for Adampak is an industry consolidation. Everyone knows Western Digital and Seagate are late into the game. The likely thing that these 2 will do is buy up the smaller players for technology. But they cannot buy up Intel which is big on this.

Conclusion

I do see that Adampak having an important role to play in an industry that will continue to be around. Whether its HDD or SSD the important thing is that the management can tie up strategic customers not just in the hard disk industry but in pharmaceuticals.

Any one currently invested can enlighten me what you guys think of the industry.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Drizzt

Sunday 15th of January 2012

haha i am flattered. i will try to look into some in this new year hopefully don't disappoint people.

Viz Branz and Boardroom and OKP have read them once in a while but not Nam Lee.

Boardroom for one provides a lot of stability with the business they are dealing in. OKP has a smashing balance sheet and business, but you have to wonder is it because due to a construction bull run.

will look into Nam Lee

G

Sunday 15th of January 2012

I am not really good at picking companies.

So I tend to rely on well-intentioned bloggers (like your goodself) and forummers who are willing to do the heavy lifting and are kind enough to share.

Some of the ones on my watchlist (not vested) are Viz Branz, Boardroom, OKP, Nam Lee.

Drizzt

Saturday 14th of January 2012

think it will be worse. what else is on your radar G?

G

Saturday 14th of January 2012

Yeah.. thank goodness for insurance, else losses would have been more significant. 2011 wasn't the best year for semicon industry and Thailand. Lets hope 2012 would be better!

Drizzt

Saturday 14th of January 2012

i share that sentiments G, but i think thats what they are trying to do. latest update is that they are leasing another factory to take over the one with the flood problem. this will burn some cash.