Manchester United released their first half earning report and key take away is that the club is continuing to bleed.

If you guys are interested in a thorough analysis you should follow this guy call Andersred. He does a great job reviewing not just Manchester United football clubs results but other clubs like Arsenal, Liverpool and Everton at times.

Here are the key take aways from Manchester United’s 2nd Quarter results:

- Revenue rose 8-10% for the quarter and first half of the year. Do note that this is the first half of the year so Champions League earning, which make up 1/3 of their revenue, is going to be zero. Look to second half of the year to be greatly impacted

- Expenses (not inclusive of player sales) rose 14% or more. This means that year on year their EBITDA (ex player sales) is actually worse. We do not understand why the wage bill is growing so much despite cutting players

- EBIT fell 6% for the quarter and rose 10% for the first half of the year. This is still pretty okay

- Interest on debt actually fell 10% for the quarter and year! This is actually a good thing

- Know what is not a good thing? EBIT is 44 mil for the first half of the year, Interest expense is 20 mil! That is almost half of their operating cash flow brought in

- Cash Holding fell drastically due to interest servicing, bond buy backs. Cash is 50 mil, debt is 438 mil. I dunno about you but does the interest on debt look freaking high to you?

- The worse thing is that cash holding is not used in capital investments (aka players, coaching stuff and facilities) but on bond buy backs, debt servicing

- And if you think debt is going down, quarter on quarter it is actually going up

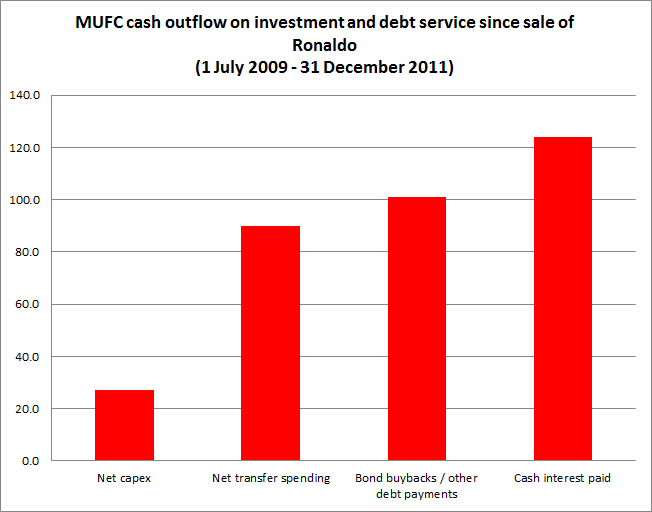

This bar chart from Andersred sums it up best

It compares very well with other leverage buyouts, large amount of cash is replaced by debts and the cash flow services the debt.

The company becomes a zombie. Typically you would expect buyouts to improve operations, which they did show in Media revenues. But overall this is to the detriment of the company.

The bond buybacks are at an even higher cost then when the bonds are issued. The majority of cash flow is spent on interest payment.

The Glazers talk about IPO in Singapore. And they say they want to wait for the right time. To be honest it will be a sucker deal for the investors because it will not be cheap and it will not be value.

But MUFC needs this more than anything else. Replacing that 438 mil debt could change this club to a cash flow generating machine.

My question is: Isn’t there a way to refinance the interest at a lower cost?

I run a free Singapore Dividend Stock Tracker . It contains Singapore’s top dividend stocks both blue chip and high yield stock that are great for high yield investing. Do follow my Dividend Stock Tracker which is updated nightly here.

If you like Investment Moats, do support us by Liking us or +1us below!

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Shan Rui

Wednesday 22nd of February 2012

By issuing a 500m IPO in Singapore, they can clear their debt. If i am already an investor in it, I won't mind diluting my equity just to clear the debt away since it represent an extra 20m in profit each year from interest expense + a better balance sheet

Drizzt

Wednesday 22nd of February 2012

Hi Shan Rui, as a fan of course that would be the best move. I know i am not buying it cheap. its the worst kind of investment monetary wise. But this isn't just any investment. Its probably a matter of life and death.