This post is a review of my expense for the year of 2018.

I started off with only $6,000 in my bank account and I am probably one of the bloggers that wasn’t such a well performing employee, or the one that had a great side line.

So a lot of it has to come from watching what I spend.

However, when I started doing this 5 years ago in 2014, it is more of whether I can keep this going and show something I am comfortable in showing.

This post will show:

- links to past annual expenses review

- what I used in the past, and now to track all these stuff

- some review of the expenses

- illustrating some expenses that are not permanent

- the annual expense and relation to your retirement or financial independence goals

My Past Annual Expenses Review

Since 2014, I been doing this annual expenses review.

In each article, you can find out what I think about my expenses during those years, and how they evolved over time:

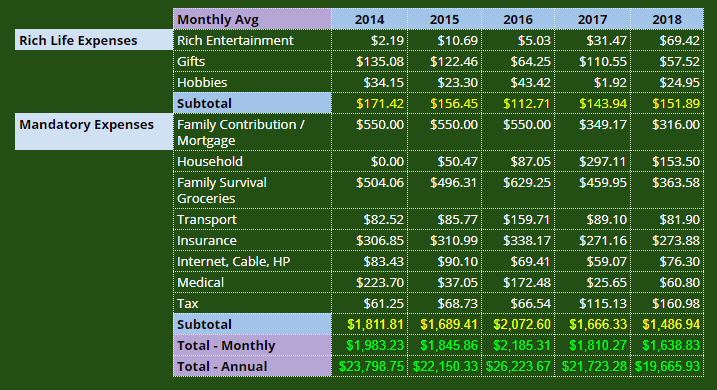

- 2014: $23,798/yr – A review of my past year’s expenses

- 2015: $22,150/yr – How our family’s $22,150 annual expenses means for our financial security and financial independence

- 2016: $26,238/yr – My Annual Expense Report – $26,238/yr and its link to Financial Security and Independence

- 2017: $21,723/yr – Annual Expense Report 2017 – $21,723

What Software I used to Track my Expenses

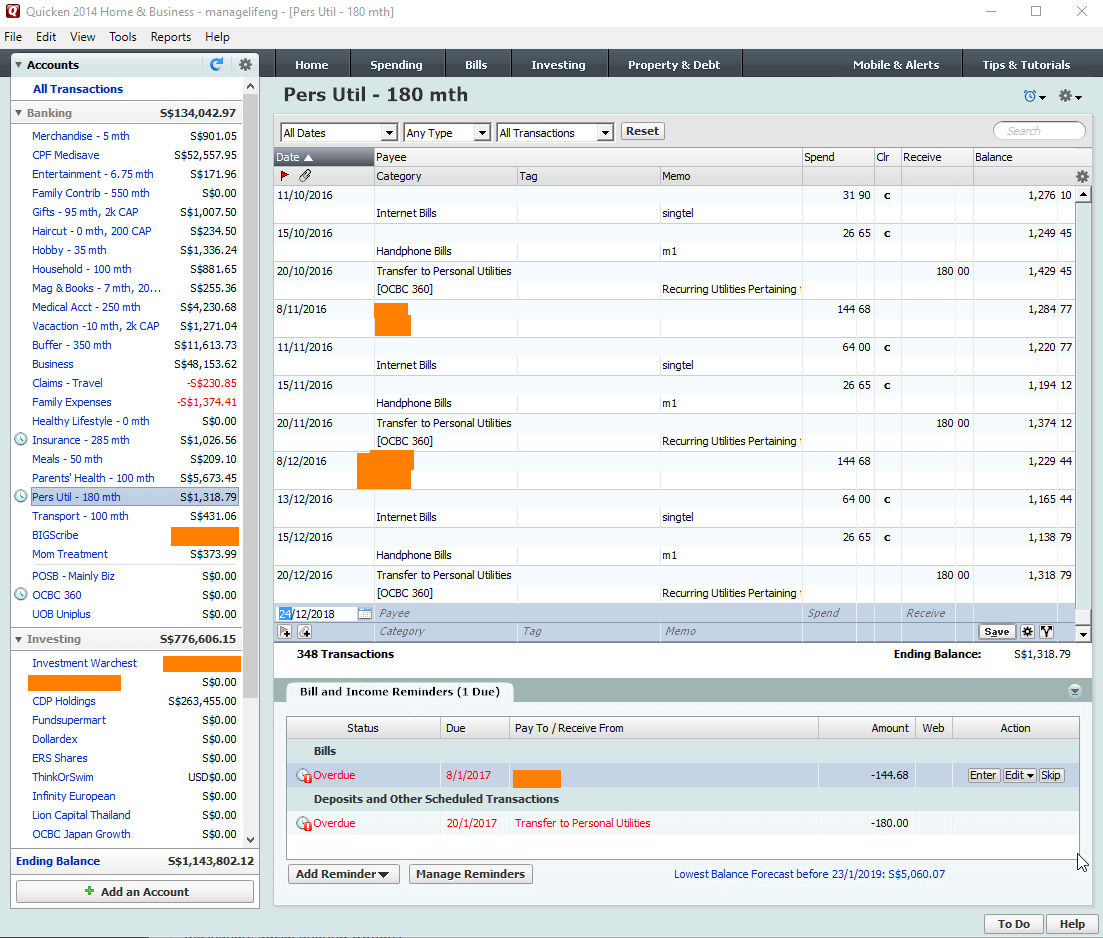

From Jan 2005 to Oct 2016 (11 years 10 months), I have been tracking my expenses on Quicken. I only input the expenses in Windows, when I get home. For a long time, smartphone does not exist.

click to view larger image

Quicken is very old school but the great thing is that it is very flexible to adapt to envelope budgeting. It is a paid software and after some time, I just got sick of paying for it. Actually, the cost of it perhaps is less than the subscription services nowadays!

One thing that a lot of people may not noticed, that is rather helpful, is the reports that could generate. I went back to my old Quicken and pulled this report of spending by category from 2005 to perhaps 2016.

Since reviewing is an important aspect of a personal finance application like this, this makes Quicken worth the money you pay for it.

You can also see the crazy $31,000 I spent on medical in the past!

Quicken is pretty good if you like:

- Create multiple accounts

- Tracks your investment portfolio

- Schedule Transactions

- Can be modified to do Envelope Budgeting

- Numerous very useful reports

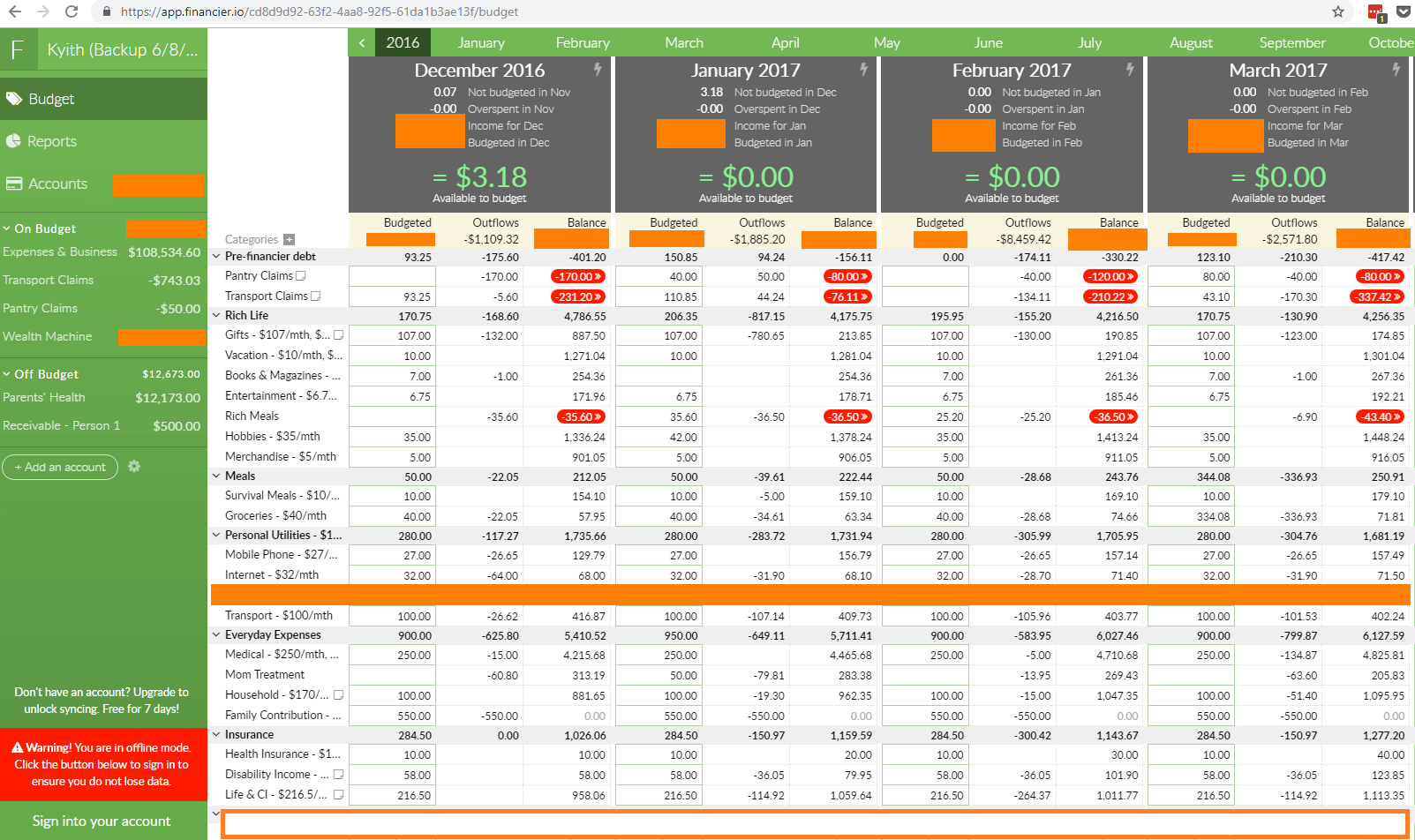

From Nov 2016 to May 2017 (7 months), I decide to support a online/offline Envelope Budgeting Web App called Financier.io. Alas, it was not to be. The project went unsupported, but it was pretty functional after it stopped.

If you would like a sophisticated, yet free web app, that is offline, that does Envelope budgeting, you can try Financier.io. Your data would only be clear if you empty the cache of your browser.

You can backup the data, and you can restore the data to continue your work. The backup is robust, as I have restored it on different computers a lot of times (for reference purpose).

Here is a summary of what I like about Financier:

- Does YNAB (you need a budget) level Envelope budgeting

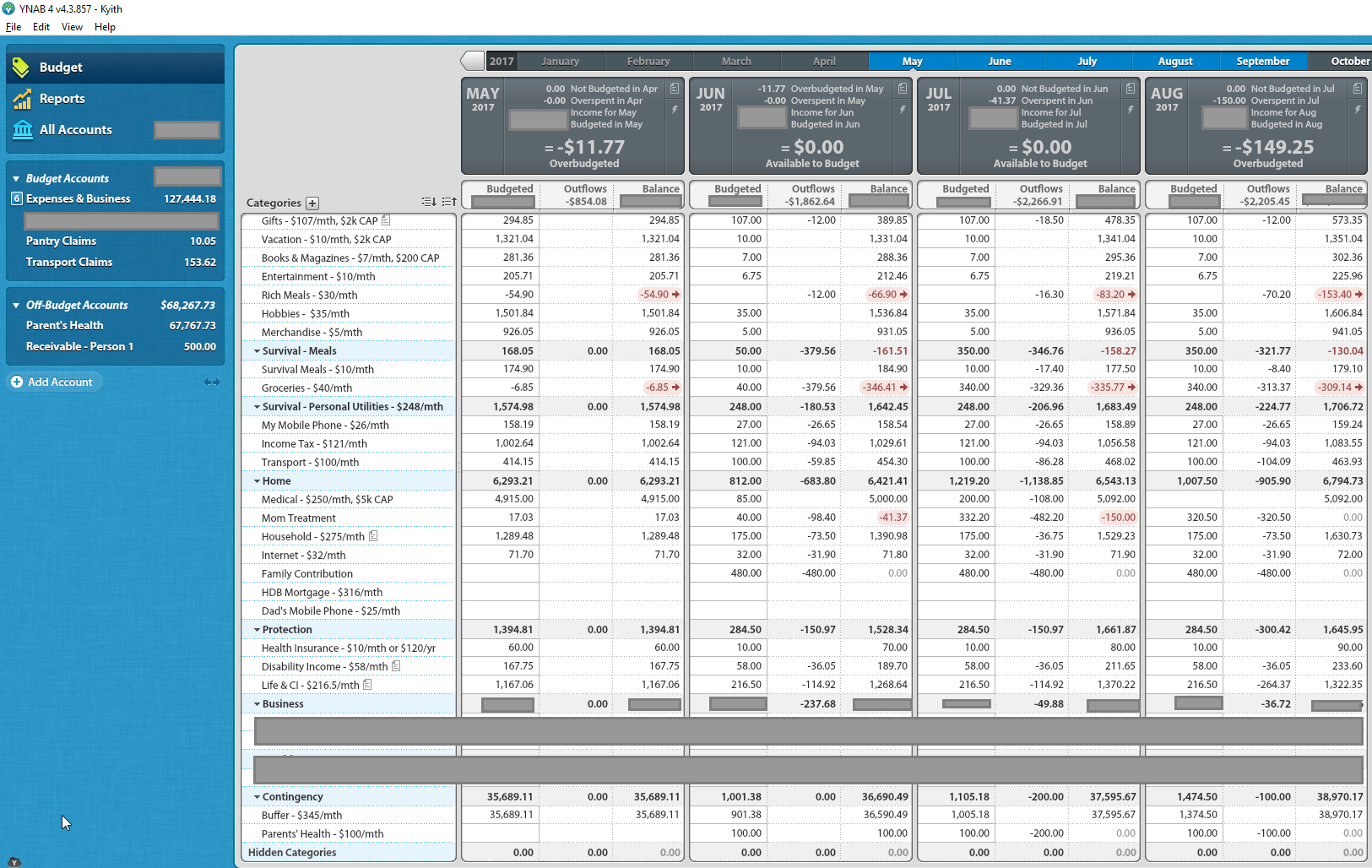

From May 2017 to Today (1 year 7 months), I have been using the old classic version of You Need a Budget (YNAB 4). I bought it off Steam for . Shortly after that, they decide to make this a subscription based service (US$6.99/mth).

If you do envelope budgeting, there is not a lot of things that would beat YNAB.

Click to view larger image

You can see how similar Financier.io is to this. Which is why if you do not know if YNAB will work for you, and you are stretched for cash, you know which one to go for.

Click to view larger image

Again, to compile this report into a spreadsheet, it really help to have good reporting. This is something that Financier.io struggled with because one person just cannot add so much functionality.

It is still usable now for me. For new users, you cannot get it.

Here is a summary of what I like about YNAB4:

- Sophisticated Envelope Budgeting

- Schedule Transactions

- Numerous very useful reports

- Android and iPhone companion app for data entry

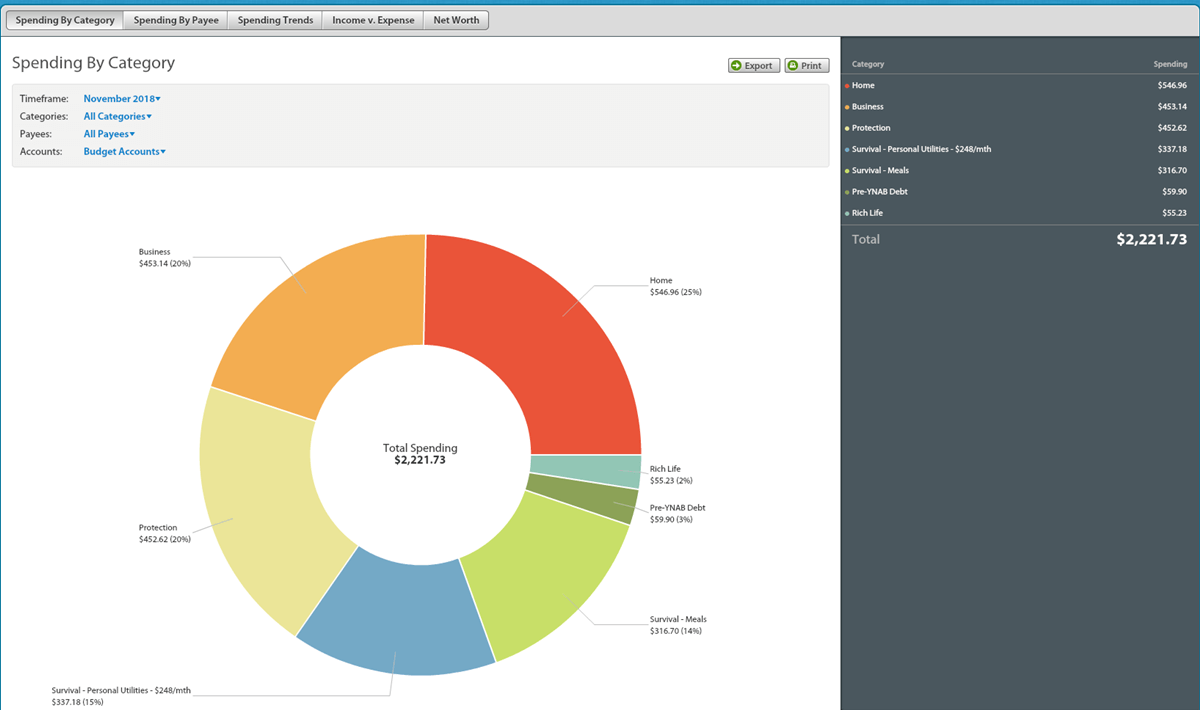

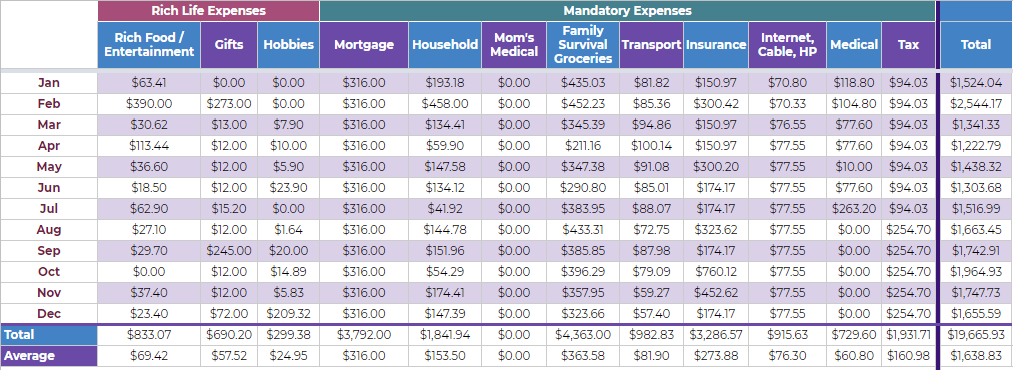

My Review of My 2018 Annual Expenses

Click to view larger table

In the table above, I have tabulated my monthly expenses break down. Some categories do fluctuate month to month, particularly when there is one off items.

The annual expense is $19,665/yr. That comes up to about $1,638/mth.

Last year it was $21,723/yr and $1,810/mth respectively.

For those who have read my article on what an annual survival expense means, you can see I have 2 master categories:

- Rich Life Expenses. These are expenses that make life interesting and not dull to live on. It is also a category to be reduced when life gets a bit tougher or you have some other financial goals that you are prioritizing

- Mandatory Expenses. This is mainly the survival expenses. These are the expenses that you cannot run away from. If you don’t spend, the household does not function in a minimal manner.

In the table above, I tabulated the average monthly spending for roughly each category. There are 2 master categories, rich life expenses and mandatory expenses. You can remove the rich life expenses, when the going gets tough, but not the mandatory expenses.

Of course, I have to relabeled some of the categories since I have re-categorized some of them since 2014.

So here are some thoughts on my expenses.

Top 5 Expenses

If you are trying to optimize your expenses, you will do best by focusing on the “larger rocks”.

Take care of the larger expenses, and you will find the greater cash flow.

My top 5 expenses are:

- Family Survival Groceries: 22.5%

- Mortgage: 19.3%

- Insurance: 16.7%

- Tax: 9.84%

- Household: 9.0%

Top 5 expenses is 77.3% of total expenses.

It is a good thing that #2, #3 and #4 are expenses that are not always permanent in the long run, and can be cut away (to be discussed later)

I do see #4 to be higher next year.

Top 5 Increase in Expenses

These are the expenses that increase by the most:

- Hobbies: +1200%

- Medical: +137%

- Rich Entertainment: +118%

- Tax: +39%

- Internet, Cable, HP: +29%

Those look like big increases, but you realize only tax is among the top 5 expenses. The rest are much smaller so an increase in expenses is not such a big impact.

The tax increased because I earned more. The internet, cable and HP is more because I factored in my Dad’s cell phone bill. Medical will fall next year most likely.

I didn’t spend a lot for hobbies and rich entertainment. They made up 5.7% of my total expenses. So the increase has been less of an impact.

Mandatory Expenses to Rich Life Expenses Ratio

We evaluate mandatory versus rich life expenses to have a sensing if that is what we want.

If you are trying to be frugal to prioritize saving, having higher rich life expenses versus mandatory expenses is probably not what you want. If you are retired and enjoying life is a requirement, then having a lower percentage of rich life expenses might mean you are short changing yourself.

- Mandatory Expenses: 90.70%

- Rich Life Expenses: 9.24%

My expenses is still a profile of bare minimum expenses with very little enjoyment.

Another significance of such a loop sided ratio is that, if the going gets tough, I do not have much to cut down really, so that I controlled my expenses. If you have more rich life expenses, then you might have more leeway.

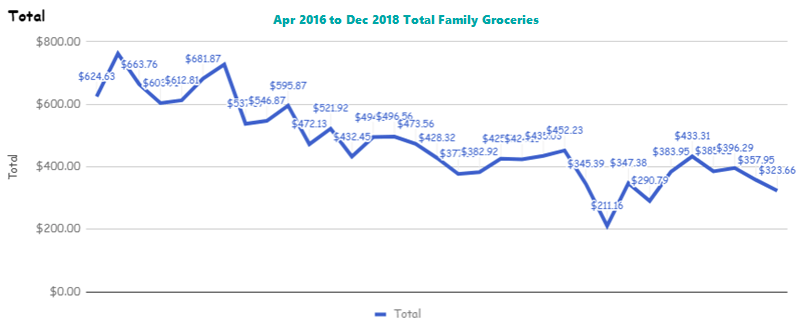

Family Expenses Month by Month over Time

The top expenses is the groceries, food bill for the family, so I do record this small subset of my expenses to see how they change over time. This is typically my family’s food cost.

Currently, this is the food cost for 2 person.

My dad does majority of the grocery buying, with the rest done by myself for designated items like sweet potatoes. Thus to make it simple I would ask him to ensure that for all his purchase with receipts keep the receipts in a container. I will tabulate them at the end of the month.

For those without receipts, tell me and we record them in a note book. I will tally them at the end of the month as well.

End of the month, I will just add up:

- my own groceries spending and survival expenses (if there is any) from YNAB

- Dad’s spending without receipt

- Dad’s groceries with receipt

The this would be our family expenses.

The spending went down since 2016, where it was more for 3.5 person to 2 person. This came up to an average of $363 per month.

This year, I did not record down the line items of what makes up this amount of spending. I think there is no need. I don’t think it will make much of a difference.

You realize there is a tilt downwards, and I think that, if you focus on refining the process of what keeps you satiated and satisfied, your costs will be rationalized.

The Recurring Expenses that will Go Away

There are some expenses that I am paying for now, that will be reduced in the future.

What this means is that the annual expense could go down even further.

There are 2 kinds of expenses that will go away:

- Fixed Tenure Expenses

- Expenses that are tied to employment

Fixed Tenure Expenses

Fixed tenure expenses have a particular duration. If you pay them off, you will not need to pay for them again.

I do have 2 of these.

The first one is my parent’s mortgage. I have been paying for it since I started work, with cash (instead of the usual CPF).

We should probably have almost 4 years more of payment and about $14,000 left.

Of course, I could choose to pay it off in one shot, but I see little advantage in doing that. I have paid up most of the mortgage interest, such that the majority of the payment now goes towards principal repayment.

However, it might motivate me to save up $11,000 next year so that I can match this liability.

The second fixed tenure expense is my Tokio Marine $50,000 20 year limited whole life.

I got this policy in Nov 2006, so I would have almost 9 years of premium left to pay. Once that is done, I would have owned this policy outright.

In total, that will be $10,260 worth of premiums left.

I have ask whether I could pay this premium in full, and whether there are any advantages in doing that. The answer is that I couldn’t do that.

I am still on the fence about the role of this policy. Perhaps I need to review the way that I look at this policy. The surrender value in Jun 2017 for this policy is $9167.55, so I would probably lose $2,500 or 2 years of premium payment by surrendering this policy.

9 years is a long time, but an annual premium of $1150 is not going to make much of a difference at this current point.

I could possibly replace this with a decreasing term life insurance policy.

Paying off these fixed tenure expenses to me is accelerating the asset versus liability matching.

In total, I could reduce my annual expenses by $4,932/yr.

Expenses that are Tied to Employment

Then there are the expenses that only exist due to work.

There are 2 that fits this as well.

The first one is Income Tax.

You pay income tax when there is work. If I do not work, I save on income tax. If I work part time, my income tax is reduced.

So the saving here could be $3,000 to $4,500/yr. (trying to project)

The second one is less transport cost. If you do not work, you reduce the average 40 monthly trips per month.

The savings is not a lot probably $360/yr.

How the Annual Expenses is Related to Financial Security, Financial Independence and Retirement

A common running theme of Investment Moats is on the topic of financial independence, and I was often asked how do you compute the wealth that you need to accumulate to achieve financial independence.

So the answer is a lot of the starting ground, is to know

- what is your ideal lifestyle in financial independence

- how much you need to spend to meet this lifestyle

And the starting place is from your current expenses (which is why reports to yourself like this is rather important). To find out how different your future lifestyle is, you got to know its difference from your current.

There are a few different schemes of financial independence:

- semi retirement

- coasting or barista financial independence

- just wanting some form of financial security to relief your financial anxiety by providing a cash flow that covers your annual survival expense

- be financial independent with the dream of eventually retiring

There are more different schemes, and different rungs of the ladder in your pursue of wealth, and you can use this ladder of wealth here as a guide and keep you motivated.

And for each of us we wish to live very different lifestyles. And for some of us we are very risk adverse and want to ensure we don’t have to work again, while others are more carefree in that, if things do not work out, they can see themselves going back to work easily.

So with that in mind, you need a sum of money.

This sum of money is put in a portfolio of financial assets and it will grow over time.

You would withdraw or spend a percentage of this sum of money annually. The more you withdraw, the greater stress you put on your portfolio of financial assets. The less you withdraw, the less stress you put on it, but you have less to spend.

So you are always trying to find where is the Goldilocks point.

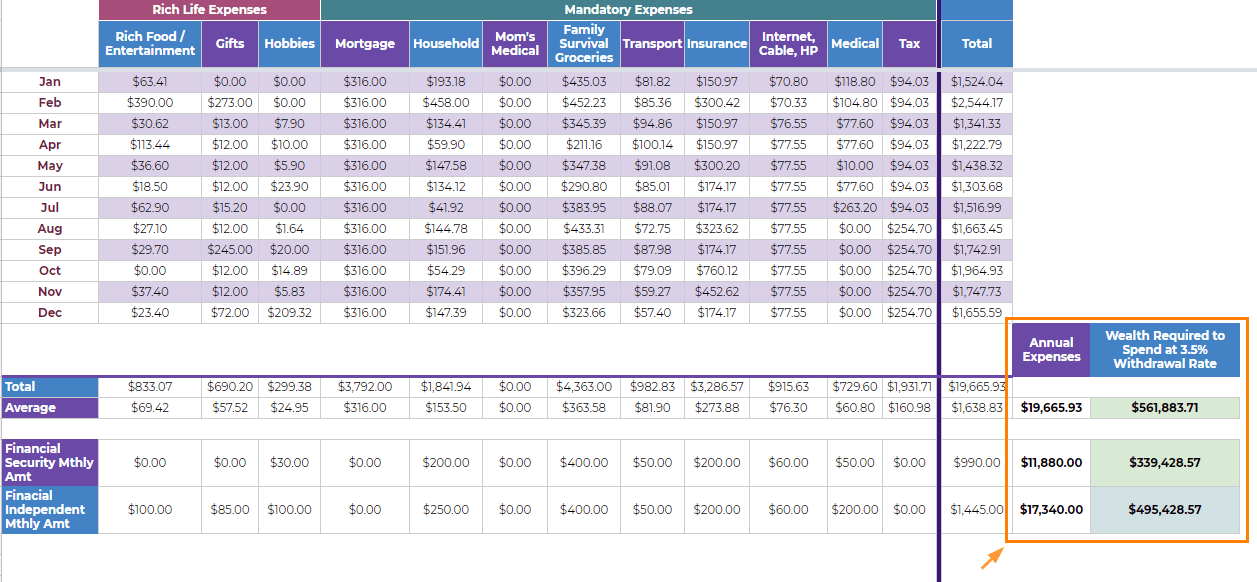

Click to view larger table

So here is the table where I show what makes up my annual expense. I always aimed to be financially secured, but not really financially independent, since I see myself as working. I wanted to ensure that I put myself in a good financial position that is all.

So I worked out, based on my current expenses, how would my spending for each category change, if I were to be financially secured or independent.

For example, the rich life spending budget would be larger in financially independent, I would gift more, spend more on hobbies.

For both financially secured and independent, I do see the mortgage being paid off, less insurance expenses, and tax expenses.

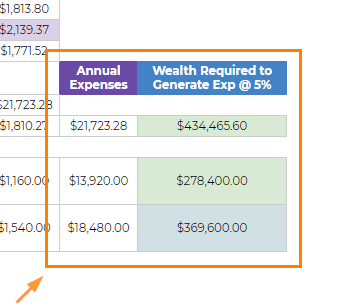

So the annual expense to be financial security is $11,880/yr and financial independent would be $17,340/yr. And I think these numbers will change as life changes (which is why people would say its difficult to project how much you will be spending. But you got to start somewhere isn’t it?)

With this, you can calculate how much wealth you require to achieve this.

After that, you can compare that to your current liquid net worth to see how close you are to these financial goals.

So I compute an initial year spending rate of 3.5% of my wealth. This means I take out $X for the first year, then for second year, I increase $X by the inflation, and third year, I increase the second year amount by inflation.

Why 3.5%? I think 3.5% is more conservative than the often touted 4%, but its still not absolutely safe (compared to 2.5% to 3%). If you check out my planning for retirement section, I go into this in a deeper manner. Please comment below if you wish for more explanation on this.

So I would need $11,880 / 0.035 = $339,428 to be financially secured, based on a baseline annual survival expense.

I would nee $17,340/0.035 = $495,428 to be financially independent.

I also compute based on my current 2018 expenses and the sum required is $561,883.

The more you need annually, the larger amount of wealth you need. The more risk adverse you are (which means instead of withdrawing 3.5% of the first year, you withdraw 2.5% to 3% of the first year), the larger amount of wealth you need.

This is the math that you cannot run away from.

I am not going to say outright whether I have attained any of these financial independence life schemes, but if you are smart, you would have picked up enough Easter Eggs to know how close I am from this.

Shifting from a Conservative Dividend Yield formula to a Withdrawal Rate formula

Regular readers of the blog would realize that these sum, is higher than that of the 2017 figure, despite the spending going down.

So here is 2017’s figures for the same section:

The main difference is that, this year I used a 3.5% withdrawal rate.

The past few years, I based it upon a system of spending a “conservative” dividend cash flow, that is equivalent of a 5% dividend yield.

The idea is that we can find many dividend stocks to invest in, with some higher yields that is more risky and lower yields that has more quality. We could form a portfolio that realistically provides a dividend yield of 5%.

As long as the portfolio grows an additional 2% per year on average, for a 7% total return, this stock wealth machine should work relatively well.

Over time, with deeper research, I find this concept to be filled with flawed.

I would not go too deep into this but here are the summary points:

- it makes retirees reached for high yield stocks, so that they can meet their goals, and may put more than needed risks to their retirement

- the idea is that just spend on dividend income, and don’t touch the principal, and the principal can appreciate back to its original cost, thus a dividend equity portfolio can combat against sequence of return risk. Your result would really vary, because there are stocks, whose business can get impaired in certain poor markets such that your capital cannot recover. This strategy does not work in all situations. You need to be a competent dividend investor that actively manage your portfolio to do that. And competent dividend investor do sell and lose their capital (but redeploy this capital to areas that provide the best risk adjusted returns going forward)

- dividend income fluctuates. This would mean your annual expenses fluctuate as well. If every $1 of your retirement expenses is mandatory, then you will face some lifestyle problem. You cannot frugal your way out of this. If your annual expenses contains expenses that are non mandatory, then you can frugal your way out of this

- not every readers invest in a portfolio of stocks. Basing the communication on withdrawal rates is more universal.

I think moving onward, it is better to see your returns as total returns ( capital growth + dividend income that is reinvested) and seeing how much you spend from your wealth machine on a consistent basis.

Does that mean that my previous estimation on a 5% conservative dividend yield is flawed?

I think we have to viewed it in context.

An annual expense update like this is very personal, and if you are aiming for financial security like myself, then this would still work for you.

The demands on your wealth machine for financial security is very different from a full blown retirement:

- you are probably not looking to spend that cash flow to perpetuity, or 50 to 60 years. For most they probably are looking at a 1 year, 2 year, to 4 years relief, then they will go back to earning, to build up the wealth machine again

- what is similar is likely all the expenses is mandatory (since its required for basic survival)

- if the dividend income fluctuates, there are plans to take a lower paying job, just to meet that basic survival

And given this permutation, if you form a dividend stock portfolio that yields a 5% dividend yield, it would fit this need.

Let us revisit the summary points before:

- Don’t reach for high yielding stocks. In this article I written about how you can shift your dividend portfolio to be more conservative, do evaluate the stocks that form your portfolio to be based on either more matured business that is still growing, business that are growing but paying a decent dividend, or at most matured business whose businesses are intact. Always evaluate the quality of the business, versus the price you pay for it. You could still get an average portfolio dividend yield of 5%

- If you form your portfolio with REITs that yield 7% when their valuations are attractive (and not when their prices do not provide high margin of safety), but spend only 5% of it, it gives you room to maneuver when the dividend per unit gets reduced

- If the dividend income is not adequate, systematic sell some units to make up for it. This works only if you would replenish your portfolio next time from your work income. This will enable you to provide a consistent cash flow

- When the business behind the stock looks like it will be impaired, or that it would not do so well in a cyclical downturn that you can foresee, re-balance the stock to one which will survive better, or into cash. In this way, you eliminate sunk cost fallacy, and always set up your portfolio with stocks that give you good risk adjusted returns going forward

To do this, you got to be relatively competent in managing a dividend portfolio, which over time I realize, can be rather challenging.

I think if there is one critique, it is that for financial security, it should be based on:

- survival expenses that are very well optimized to make sure those are really the bare essentials (no cable TV, no providing for parents or in-law parent, no Ang Bao)

- based on a very conservative withdrawal rate from your wealth machine

- income cannot be volatile or fluctuating

So given the above, a more sensible withdrawal rate should be a 3% initial withdrawal rate.

If your annual survival expense is kept to $12,000/yr, you would need $12,000/0.03 = $400,000.

We will know that if the line items for survival stay the same, if we have $400,000:

- we have a perpetual wealth machine

- tested with historical data

- that provide us with consistent inflation adjusted cash flow

- to provide for our annual survival expense

That 5% dividend yield formula works but you would have to make a lot of adjustments, and that requires a certain level of competency. To have absolute security, you might want to keep it simple, have less adjustments.

You would need a larger sum of money though.

Next Year Spending Will Be More

It looks like there will be some spending coming next year:

- home painting

- higher taxes

- ancestral tablet

Summary

I think for a lot of the topics that we discussed on money, you cannot run away from the expenses discussion.

And in the second half of this article, I shown just how much your longer term financial goals, depend so much on your short term annual spending.

If you have tallied up your annual expenses, you might have some stories to share. You might also have some queries on this post.

Do discuss below.

This is the last article for year 2018. I will see everyone in 2019!

Do Like Me on Facebook. I share some tidbits that is not on the blog post there often.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Alex

Sunday 30th of December 2018

Hi Kyith,

Thanks for your constant contributions, they are very insightful. I have just a question. When you compute a financially independent amount, I noticed that you do not factor in CPF payouts when you arrive at the eligible age. Is there a reason for that?

Kyith

Sunday 30th of December 2018

Hi Alex, I take it that I do not need to depend on the CPF policy. I think it makes sense for more people considering they tend to use their CPF to pay for housing. They would have to build their wealth without the CPF. if i add in my CPF.... i think the withdrawal rate is even lower.

Isaac

Sunday 30th of December 2018

Hi Kyith,

I want to encourage you and thank you for all the articles you have written in the past. We have learned alot from you.

It seems that your personal expenses is very low. In fact, your spending could be at the bottom 10% percentile of the local population which is amazing! I'm even stuggling at your average monthly spending. I usually spend close to 2k per month which my colleagues already feel i am very frugal.

May i give u some suggestions?

1. Continue to think a life of abundance! The earth provides. I can see that you already hit a floor of expenses. It's easier to increase income on your side hustle.

2. You are very young at late 30s. I project at least you can scurried another 20 years of your earned income to your portfolio. If you are invest well, you can hit 7 figures by your late 50s most likely.

3. Since you hit 7 figures, you will have more than enough for your monthly expenses even at 3% withdrawal rate.

Wishing you well into 2019! Stay healthy and eat excellently so you can save on medical fees!

God bless and continue the good work!

Kyith

Sunday 30th of December 2018

Hi Isaac, thanks for the encouragement. Those are good advice. What would your side hustle be?

All the best for your 2019 as well!