Last year around the same time, in early June, Azalea Capital issued their Astrea IV bond.

What was significant was that this was the first bond that Azalea Capital open a specific tranche that retail investors are able to purchase with smaller denomination. The reception for Azalea IV was very good.

And so now, 1 year later, Azalea Capital decide to release the Astrea V.

Currently, the Astrea V bond is in the order book building stage. It is kind of crazy this time round. As of now, I heard it is greater than US$4.3 billion! This means the demand for this bonds is a lot.

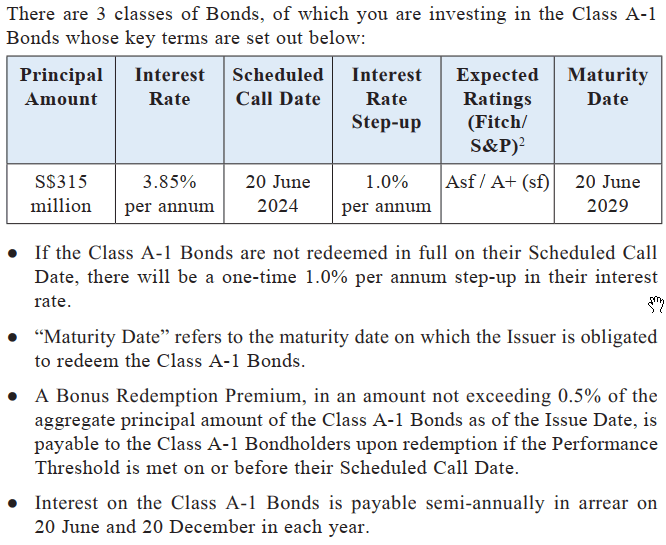

The final interest yield is as follows:

- Class A-1 Bonds (available to retail investors): 3.85%

- Class A-2 Bonds: 4.50%

- Class B Bonds: 5.75%

I think it is likely that if you bid for it, you are not going to get a lot. You would have to buy from the open market when it starts listing on the stock exchange.

If you are a retail investor, and are interested in this, only the Class A-1 is available. You can subscribe in denomination of $1,000, with a minimum subscription of $2,000. I think this is very affordable to the public.

This structured bond, follows the same tradition as the Astrea IV. And there is not a lot of things new about this bond.

If there are some things different it is that the yield would likely be slightly more compressed and the underlying PE funds are different.

I still have that feeling that government is trying to create an environment that we can build wealth with different kind of financial instrument.

A few bond issues by government linked company, or blue chips company is happening:

- Astrea IV Bond

- Temasek 2023 Bond

- SIA Bond

So this adds to bonds issued by relatively well known institutions.

I think I will not wish to repeat a lot of things, and you would gain some benefits from reading my old article on Azalea IV which yields 4.35% to 6.75%, depending on which tranche you subscribed to.

If you want more in-depth easier to understand stuff, you do not find it in investment moats, It is better to turn to the experts at Seedly.

Here are some things to bear in mind about the Azalea V, if I wish to emphasize:

- The issuer Astrea Capital V, belongs to Astrea Asset Management, which is a wholly owned company under Temasek Holdings

- Only the Class A is rated, the rest are not. In terms of the ratings they are largely the same

- There are a few safety mechanism build in place to ensure Class A-1 bonds have a greater chance of being redeemed

- Credit Facility to smoothed the payout of the interest payment

- Reserves Account are proactively build from losses, divestment. These work towards funding the reserves account so that enough safe money to call back the bonds on the 5th year

- If the net asset value of the underlying funds fall, the reserves are also used to deleverage

- That said, Astrea V is a structured bond but it is not a traditional bond.

- The underlying PE funds is likely leverage, and also so are the underlying companies within the PE funds.

- The very fact that the interest rate for a rated bond is higher than the Temasek 2023 bond and SIA Bond should tell you that this is not a straight forward asset

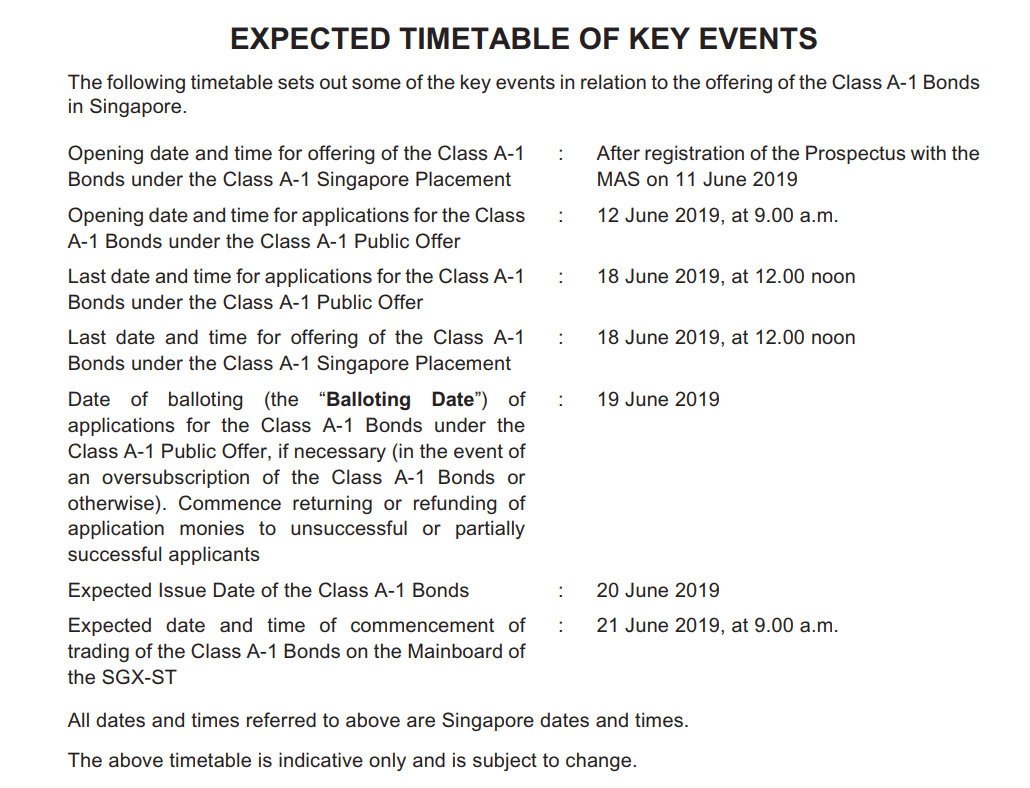

Time Table of Key Events

Here are the expected milestones for this structured bond issue:

The key milestones are that for the retail public, you can start applying on the 12th of Jun till 18th of Jun noon. That will give you 6 days to apply.

Some Risk Management Stuff in the Prospectus

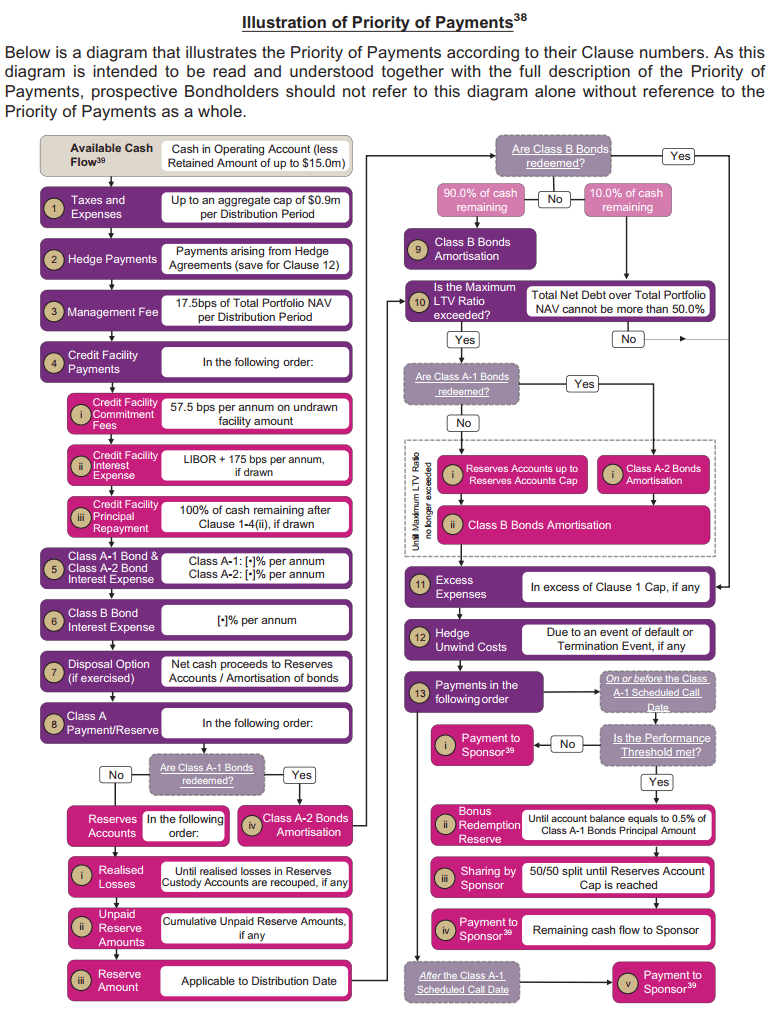

The above graphic is how the issuer wishes to illustrate to you the priority of the payments.

The underlying private equity funds from time to time, will make distributions or realized capital returns out of their funds. These will be the cash flows that are returned to you.

What the above tries to illustrate is how they prioritize every dollar.

It is pretty complicated and I am not going to admit I know all of it.

The folks at Seedly and Financial Horse are better at explaining these stuff to you. My general understanding is that some of the expenses such as taxes & expenses, hedge fund payments and management fees will be paid first.

Subsequently, the interest payments are made to the Class A-1 bond, Class A-2 bond and Class B bond.

The cash flow will then flow to the reserve account in managed portions so that they are worked towards getting ready to call the Class A-1 bond in 5 years time.

The Sponsors will get the excess money after all this.

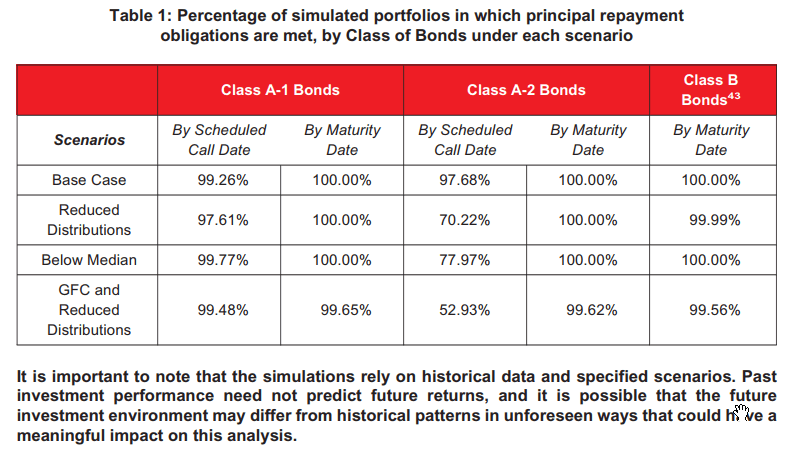

The issuer sought to alleviate your concern about whether all these mumbo jumbo cash flow will work out by going through some simulations as well as go through some historical scenarios.

If you look at the above table, observe that they computed the expected probability of success which includes their ability to call the bond in 5 years for the various different classes and the ability to fully redeem the bonds in 10 years.

That looks pretty locked in. Of course, we have no idea what are the variables that they use.

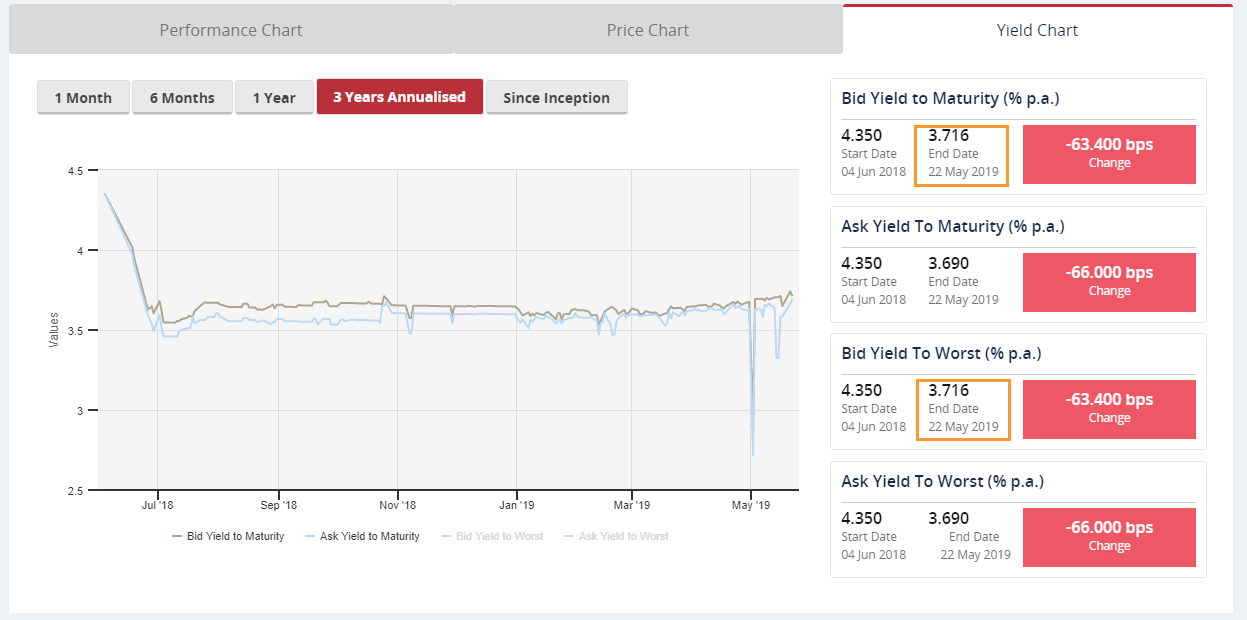

Reviewing the Astrea IV Performance

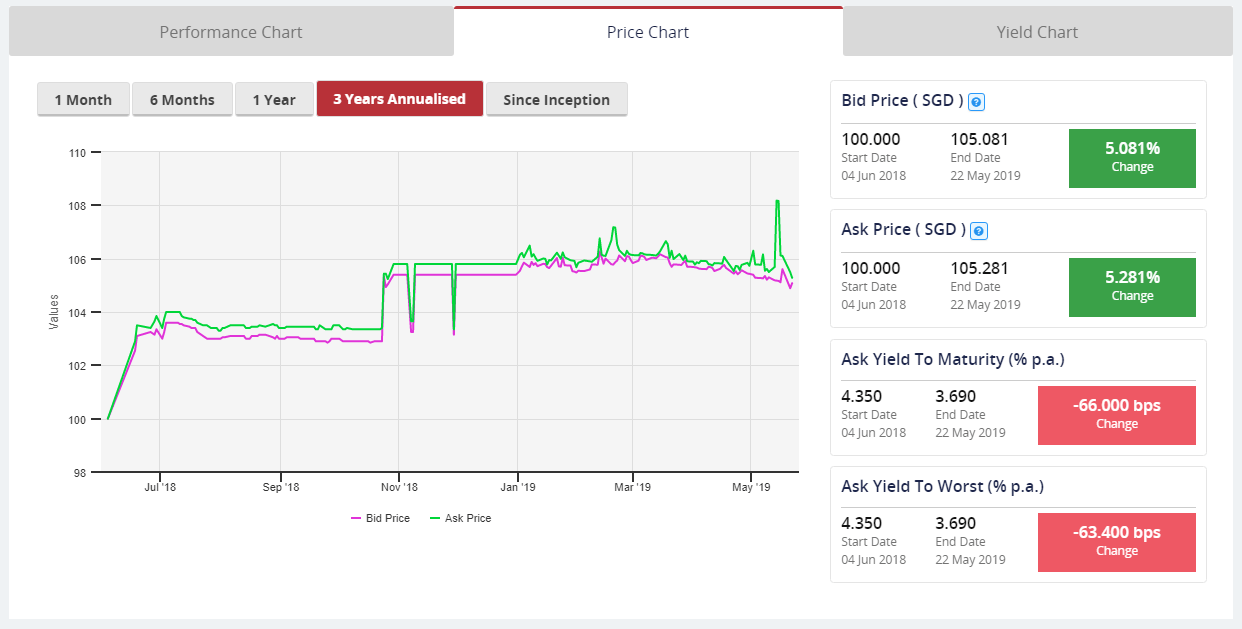

The Azalea IV appreciated in value from the start of trading.

For those who are not aware, you can purchase the Astrea IV, issued last year on the SGX. It is listed on the SGX exchange and you can purchase it on the market just like a stock. If you choose to purchase the Azalea V, it can be sold to the market as well.

You would have to pay the necessary trading commission levied by your broker.

The Astrea IV Class A-1 was issued at 4.35%. Since then, it has compressed to 3.716% since then. This means that if you bid for the Astrea IV Class A-1 bond through your brokerage the yield to maturity is 3.716%. I suppose the yield to worst should specify the yield to call date of 2023. The yield to worst is the same as the yield to maturity. Typically there is a difference there. Not sure how that worked out.

If we look at Astrea V’s Class A-1 yield, it is very close to the yield of Astrea IV Class A-1’s yield.

Somehow, the market is rather efficient there. If both structured bond’s risks are similar, and the duration are the same, then the yield should be pretty close to one another.

Notice the price appreciation at the initial few days. This shows you how popular the structured bond was during that period. Then it spiked again, likely due to the potential of interest payment 6 months later. I suppose another spike might be coming since the coupon payment would be soon.

Summary

I think this issue is not so different from the previous one. I wonder if the more that Astrea keeps issuing these bonds, and you keep seeing that there are no issues, whether you will be conditioned to think that these are normal bonds.

I strongly think that we would.

And soon, we might be owning a lot of structured bonds. You might start seeing people deploying $20,000, $50,000 into these bonds.

And then acceptance to alternatives to unit trusts, property, fixed deposits and stocks would develop.

I have friends who are more well schooled in these stuff and voice various misgivings about these bonds. They might be right. It is just like me saying some of these retirement strategies would not work the way you think, in certain scenarios. When you go deeper and know more, you start seeing the realities, and knowing those realities will hinder you from investing in this seemingly safe thing. In most times it is good.

But sometimes it can be bad.

We have to ask ourselves how probable those scenarios will happen and the relative impact to your capital.

My counter argument to that is that, the government might be enjoying this kind of PE returns in different ways, either through direct investing, or through bond or pseudo bond like investments for some time.

And there are some of us who complained why this is not available to the public.

Now it is available to most of us. And yet there are negative murmurs to this.

As I end of this post, I would leave you with a few of things:

- To get a higher than expected return, there needs to be some form of risk premium. This is in the form of taking market risk, where your money is subjected to volatility, potential capital impairment. Or in the case of bonds, you take on credit risk. If the yield is good, there are some potential risks. Your job is to assess and see if a bond/stock has asymmetric returns profile (high return low risk)

- And if all things are risky, that means that to protect yourself, or to assure yourself that things will not blow up, you got to look deeper into it with enough sophistication (or people with adequate sophistication)

- If you want true safe things, the yield or total return profile will reflect that. If the total return is attractive to you, there is some risk (go back to #1)

- Diversification solves a lot of problems. But there are some things that you should not rely on diversification. It is like the prevalent saying that you should eat a balance meal. I do not think you will add some rat poison to your daily meals just to eat a balance meal isn’t it?

For those that are interested, take note of the time table. You can apply the Astrea V at the ATM or through internet banking at the major banks.

Do Like Me on Facebook. I share some tidbits that is not on the blog post there often. You can also choose to subscribe to my content via email below.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- New 6-Month Singapore T-Bill Yield in Late-April 2024 to Drop to 3.70% (for the Singaporean Savers) - April 18, 2024

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

astrea

Saturday 15th of June 2019

keith, are you buying? =)

Kyith

Saturday 15th of June 2019

hi astrea, I have some other things to buy.

Don Chua

Friday 14th of June 2019

Hi there! I created a calculator for the Astrea V PE Bond and thought it might be useful for ohers as well so I uploaded it on github. It is available at: https://github.com/chuadon/Astrea-V-ROI-Calculator

There's a telegram bot version of the calculator here as well, for my folks on telegram! https://t.me/astreav_calculator_bot

Kyith

Saturday 15th of June 2019

hi Don, thanks for sharing. What does the calculator do?

Philip Lim

Wednesday 12th of June 2019

This is a good buy, if you are allocated.But like the previous one, there's liquidity issue. Ok, if you hold to maturity.

E

Wednesday 12th of June 2019

Hi Keith,

May I know how the yield is computed for Astrea IV: 1. When initial price at 1.00, the yield is 4.35%; 2. But when its price at 1.07, its yield compressed to become 3.72%? I thought is 4.35/1.07=4.07%

Chan

Wednesday 12th of June 2019

May I know if the interest pay out every 6 months ? Thx

Kyith

Wednesday 12th of June 2019

Hi Chan, yes the interest is paid out every half yearly