Yesterday, I watched two videos.

One of the videos is on this YouTuber named Rishi, who made a few videos calling out scams. One of the person/company he called out decide to serve him a lawyer letter. So now he has a Go Fund Me campaign to fund his court case because he wishes to fight this case.

The second video was put up by IQuadrant who has been in the news a fair bit. They are in the news because a few people, including Rishi, tried to expose their “scams”.

In this video, the two co-founders explain in detail, with a lot of numbers, primarily how the little to no money down plan is not as dangerous as it looks.

The second video made me reflect upon something Morgan Housel wrote in his book The Psychology of Money.

I would comment on the Rishi video at the end. So let me talked about this IQuadrant thing in brief.

I think like a lot of things this year, Morgan describes it perfectly that a lot of these things would have good outcomes. But these things need a lot of things going right for it.

Financial ruin occurs when your plan, which is suppose to go right, didn’t go right and you have not build in the other what-if scenarios.

To be fair to Shawn from that IQuadrant video, he did build in some margin of safety in his example. The margin of safety is 24 months of vacancy, which amounts to 6 months of vacancy per year.

I think if you ask around with people in the know and ask them how they would build in reasonable assumption, this is fairly conservative. But the devils is in the detail.

There still has to be much things going right for this investor so that there would not be a risk of ruin.

The Story of Rick Guerin

Morgan cites what happened to Rick Guerin to help us contrast the concept of growing wealth and keeping wealth can be two different things.

They require us to have different attributes.

Here is from the book:

You’ve likely heard of the investing duo of Warren Buffett and Charlie Munger. But 40 years ago there was a third member of the group, Rick Guerin.

Warren, Charlie, and Rick made investments together and interviewed business managers together. Then Rick kind of disappeared, at least relative to Buffett and Munger’s success. Investor Mohnish Pabrai once asked Buffett what happened to Rick.

Mohnish recalled:

[Warren said] “Charlie and I always knew that we would become incredibly wealthy. We were not in a hurry to get wealthy; we knew it would happen. Rick was just as smart as us, but he was in a hurry.”

What happened was that in the 1973-1974 downturn, Rick was levered with margin loans.

And the stock market went down almost 70% in those two years, so he got margin calls. He sold his Berkshire stock to Warren- Warren actually said “I bought Rick’s Berkshire stock” – at under $40 apiece. Rick was forced to sell because he was levered.

Charlie, Warren, and Rick were equally skilled at getting wealthy. But Warren and Charlie had the added skill of staying wealthy.

Which, over time, is the skill that matters most.

Nassim Taleb put it this way: “Having an ‘edge’ and surviving are two different things: the first requires the second. You need to avoid ruin. At all costs.“

– Psychology of Money

Morgan summarized money success into a single word: Survival.

In one of the chapters, he showed us evidence that what propels our wealth are tail events. The majority of the companies failed or in my latest article, have a lifespan that is shorter than what you believe.

Not “growth” or “brains” or “insight”. The ability to stick around for a long time, without wiping out or being forced to give up, is what makes the biggest difference. This should be the cornerstone of your strategy, whether it’s in investing or your career or a business you own.

There are two reasons why a survival mentality is so key with money.

One is obvious: few gains are so great that they’re worth wiping yourself out over.

The other is the counterintuitive math of compounding. Compounding only works if you can give asset years and years to grow. It’s like planting oak trees: A year of growth will never show much progress, 10 years can make a meaningful difference, and 50 years can create something absolutely extraordinary.

– Psychology of Money

Morgan explains that applying the survival mindset to the real world comes down to appreciating three things. I will list out the one that is applicable to this case study.

Most Important Part of the Plan

Planning is important, but the most important part of every plan is to plan on the plan not going according to plan.

What’s the saying?

You plan, God laughs.

Financial and investment planning are critical because they let you know whether your current actions are within the realm of reasonable.

But few plans of any kind survive their first encounter with the real world. If you’re projecting your income, savings rate, and market returns over the next 20 years, think about all the big stuff that’s happened in the last 20 years that no one could have foreseen:

- September 11th

- A housing boom and bust that cause nearly 10 million Americans to lose their homes

- A financial crisis that caused almost nine million to lose their jobs

- A record-breaking stock-market rally that ensued

- A coronavirus that shakes the world as I write

A plan is only useful if it can survive reality.

And a future filled with unknowns is everyone’s reality.

A good plan doesn’t pretend this weren’t true; it embraces it and emphasizes room fo error.

The more you need specific elements of a plan to be true, the more fragile your financial life becomes.

If there’s enough room for error in your savings rate that you can say, “It’d be great if the market returns 8% a year over the next 30 years, but if it only does 4% a year I’ll still be OK,” the more valuable your plan becomes.

Many bets fail not because they were wrong, but because they were mostly right in a situation that required thigns to be exactly right. Room for error – often called margin of safety – is one of the most underappreciated forces in finance.

It comes in many forms:

- A frugal budget

- Flexible thinking

- A loose timeline

Anything that lets you live happily with a range of outcomes.

It’s different from being conservative.

Conservative is avoiding a certain level of risk. The margin of safety is raising the odds of success at a given level of risk by increasing your chances of survival.

Its magic is that the higher your margin of safety, the smaller your edge needs to be to have a favorable outcome.

Lawsuit Threats

The ironic thing also is that IQuadrant threathen another prominant person on Facebook who spoke out about their practices.

This is in the same way how Rishi got himself tangled up in this.

I have mixed feelings about this whole episode. Let me try and explain.

Imagine if you do everything proper and your business partner decide to create an elaborate scheme to get you off the company. Your now ex-business partner goes even further by doing all sorts of things so that you won’t have access to a single existing client. He then do a lot of things to drag your name through the mud so that you won’t have any new business.

You want a judicial system where you can fight it out and clear your name.

The issue is that there are some who have more resources than the others, and decide to use these means to get you to retract what you said or to get you to back off.

They know that for most people, they do not have the know-how or the resources to fight something lengthy.

This is not the first time that I am seeing this. For those of us in the industry, you would know what I am talking about. Most of the time, these folks with resources win.

And you know what hurts… it is that they continue with the business. The issue is that in the specturm of value delivery, they deliver on the very low end. For some, its not even value. It is outright scam.

In a Way, You want What They Give

I have developed this perspective: Some of the highest form of marketing is be able to know what you really want, appeals to you deep down inside, and deliver a message that speaks to you.

In a way, a lot of these internet marketing scams prey on those who do not have much options.

It also preys on those who are looking for passive income. (You do not see a lot of marketing materials telling you that you can have residual income or passive cash flow. There is a certain familiarity with that term)

While scams prey on those desperate folks, some of these courses prey on you because you have a lack of investment options, and you do not wish to do a lot of work, and a lack of sophistication.

But it is not always negative. We all have a starting point where we lack sophistication.

Two days ago, I had lunch with a friend who want to thank me for troubleshooting her stock portfolio tracker on and off. She came a long way from not knowing so much of personal finance and investing to somewhere where her friends turned to her for bits and pieces of advice.

While there are many free content, she shared that the difficulty during her less sophisticated phase was that investing is not written in a very procedural way.

Bascially, when you are learning, you need something more step by step.

I get very ticked off when I keep hearing people say information is free all around, why do you need to attend courses that are so expensive? You should just join this chat and learn from the people with more experience there.

Many experience folks forget how they started all this. They probably forget the knocks that they suffered along the way. There should be something procedural in their way of learning and for a lot of things, it is fundamental that we learn in a procedural way.

In November, the company send us to a 2-day ettiquete and learning course. If you ask me, for this kind of thing, it is even worse. There is less uncertainty and less impactful that we would need to invest money for this sort of thing.

For whatever that you need to learn there is a search cost. There is also tuition fees paid for making mistakes. If you do not wish to incur such a cost you would need to pay up.

There is a Spectrum of Value In Whatever Lessons You Pay For

In that spectrum, some are very useful but they are priced cheaply. Some are not very useful, but are not cheap.

There are some stuff that are priced very expensive and just do not work. They do not work because fundamentally, what they are asking you to do is not fundamentally workable over the long term.

This is what I would term close to being a scam.

The unfortunate thing is that, since you are not very sophisticated, you would not be the best person to evaluate that.

Even if you ask me, I would need to roughly know your level of sophistication and what the course provide, to know if going for a particular investing course is the right fit. I think is a total mismatch.

Often, there is a mismatch in expectation because the marketing was too good and the value provided is not up to the marketing.

So people feel cheated.

I think we got a lot of value out of our grooming course. There is a lot of nuances provided that are valuable.

Nuances in a particular subject are very very tough to learn and very valuable. How do you know that you have a problem? What is the problem? How do you articulate your problem clearly to yourself? If you cannot articulate the problem, how do you know what to search for? How do you know who to find to get this problem address?

Our more experience staff (which includes the advisers) are no slouch when it comes to grooming and looking very presentable in front of clients and prospects. Even then, there were enough questions in case studies that made us wonder if we really know how to dress well or not.

But at the end of the day, all our mileage will be different. Going for a grooming course like this is more of a primer to speed us our journey. We still have to build good habits to apply it in our daily lives.

The most fxxk thing I keep hearing people throw at these investing stuff is how good it works.

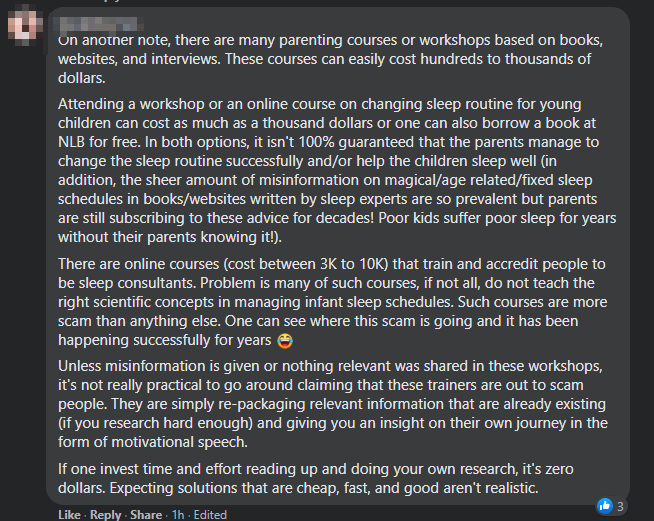

I came across this commenter who was sharing with us the amount of money paid to change people’s sleep routines:

The amount that they cited is probably around some investing courses.

Here is the rub:

- This space is most likely not regulated

- Some of the people know what they are talking about

- Some are downright scams

- Even if you attend, it might not work for you as well. The issue with addressing sleep-related issues dare I say, is more challenging than investing. We would roughly know more about how market works than why you cannot sleep well

- Addressing this problem is much needed

I do not have a good solution for this. Some call for authorities to do more. But at the same time, if there is heavy regulations, positive and better investing ideas might not bobbled to the surface.

There are Potential Consequences

Lastly, if you made a decision to call out someone, always know that there are some consequences coming your way.

And you should prepare for these consequences.

Companies pay for indemnity insurance because there are always potential legal liability.

If the potential magnitude of the damage is big, then like financial risk management, you avoid it. If not, prepare the money!

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- New 6-Month Singapore T-Bill Yield in Late-April 2024 to Drop to 3.70% (for the Singaporean Savers) - April 18, 2024

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

lim

Sunday 15th of November 2020

Like you mentioned in your article, while there is plenty of stuff on the internet your friend benefited from having face to face advice about her portfolio.

I'm very grateful that I have a network of friends that I can always talk to and ask 'is this legit?' :) For example, while I do not need a sleep consultant, I do know doctors and psychiatrists who I can check with to see if a 'sleep consultant' is legit (i don't know, but at least I have someone I trust with some expertise I can ask). Similarly, I have a friend working for ARA I can also ask him is so and so property investment course worth attending (I think you would be able to guess his answer). At the same time, I can try to be helpful in case they have queries which relate to my area of expertise.

Manferd Hoe

Sunday 15th of November 2020

Nice article. I am sure by now IQuadrant and those ecommerce gurus do aware that they have been… well… have been receiving a strong response to their advertisement.

But by explaining how they do their investments, how their investment is safe. They are treating the problem, which is the public already has a negative perception of them, with the correct ‘medicine’, which is an explanation. If they wish to help the public, I sincerely believe that they should put up more education videos or articles and educate the public instead. By sharing good and useful content is more powerful than irritating youtube advertisements when I want to watch Uncle Roger videos. (Haiya~ Advertisement again!) The public will have a certain guide on what to do. And if they want to learn more, well… the public will know who to look for mentorship. My mentor who taught me how to invest in shares did charge me a fee for the training. But he does give a risk-free ‘time frame’, as the training was 4 days, after the first 2 days if I felt it isn’t suitable for me, I can ask for a refund. No question asked refund. This shows that he cares more about teaching investment education than profiting. In another way, he is also aware that investing in shares isn’t for everyone and shouldn’t be ‘punish’ for taking the leap. It also shows that trainer whatever he is sharing has confidence it works, he does not require the training fee to earn a profit. Well, as a trainee, I respect the effort he made to make me learn, he does deserve the fee. Rishi has my sympathy as he does want to help the public and entertain his viewers along the way. Although I am grateful for how he research and help me find out more about how some advertisements are false. But in certain areas, I believe he can have more improvement. However, like you said, “Lastly, if you made a decision to call out someone, always know that there are some consequences coming your way. And you should prepare for these consequences.” I hope both parties come to a respectful and harmonious agreement and maybe a collaboration. No one is perfect, we all can learn from each other. We also can leverage each other and explain their viewpoints and answer their questions. This can be more helpful in terms of their reputation and clarify any misunderstanding or grievance.

Kyith

Sunday 15th of November 2020

Hi Manferd, thanks for sharing. I would wonder what is considered an outright scam. if I got an ounce of value from it but it's too little versus I paid for it, would that be a scam? I would think there are many courses out there with barely able to make it quality, enough to pass off not as a scam, but were overcharged. This may leave a poor taste in our mouth but usually, people will not complain about them but would just grumble about them.

The issue with a lot of stuff is because there is a lack of transparency. Interestingly, a profession which is pretty opaque has no issue of people calling it a scam: a professional service called legal services.