Back during my army days, we would meet all sorts of different characters.

I guess that is the same for you as well. It is good exposure for a sheltered JC kid to mix with people on the “other side of the track” to learn from their experience. Our team, for some reason, happened to have 2 batches of NS boys who were from JC background.

And one member who did not complete Poly.

And he is one colourful character.

Colourful things but many things best not shared on Investment Moats. The cleanest, most tattoo-less Ah Beng. Probably teaches better tuition than myself. Various entertaining past love stories.

At times he can be rather reflective about things and one topic that often came up… is the contrast between folks in his world and… JC boys.

There were not a lot of conflicts. We were able to see past that educational background and see each other as individuals because whichever background that you came from, you can find weird people, smart people, people you do not wish to be around, and cool people you want to be around.

There was one day where the topic drifted to another one of us. We both acknowledge that this guy stands out because he does not venture to do some of the things we would do due to a set of idealism that he has.

I respected him for being able to be disciplined to stay that way (other than some of the times we made him break it!) most of the time.

My Ah Beng mate reflected and say that is probably a very tiring way to live. When you have so many principles, you get dictated by them.

I think as folks whose whole career is based on studying, that comment on idealism did not hit that hard until I draw some similarities between this and the way you run my own stuff.

These kinds of principles, idealism eliminates a lot of things you could do and places handcuffs on you. The reward is that you probably felt more livable about it.

Principles and idealism became a boss with a set of tasks that you should do or not do.

They are a kind of obligation in life.

The thing about obligations is that we do not notice the effects of one obligation on our lives. Collectively, they can have an effect on our time and our finances.

And we often do not see this linked there.

I was reading an article and the writer brought up that

“We are gatherers of obligations, but if we want to ensure financial stability, we must purposefully eliminate obligations as the end of our careers near.”

As the link between obligations and money is weak, we often did not realize how much it impacts the wealth we need for retirement and our ability to accumulate for it.

So this post serves to deconstruct this topic of obligations and money.

The Obligations in Our Lives

Obligations to put it simply, are things or projects that you need to do. These things and projects can be recurring and they could be any one time only things.

The thing about obligations is that they could be the result of people giving you that responsibility. They could also be the return favours that you need to do because someone did something for you last time. They can also be the responsibility given to you because you are a human being, growing up in the ethnic background, with a certain culture.

They could be something you are perfectly fine to take on, or that you take on begrudgingly.

Now here are some obligations and you tell me if you have taken on them.

You are obligated to:

- Find a partner

- Propose with a Diamond Wedding Ring

- Hunt for a Wedding Shoot, Select and Do the Shoot

- Do a Wedding Banquet

- Get Married

- Have 2 children (because having one will eventually make the child lonely)

- Provide for your children. Give them the best to your abilities

- Work in a way that is not in conflict with your principles, philosophies, idealism

- Live a life that is not in conflict with your principles, philosophies, idealism

- Buy something for your other half on Valentine’s Day and Birthday

- Give the Market Rate Ang Bao during Your Friends Wedding

- If you are the Boss, you give more to be respectable

- Join in the social activities at work to build cohesion

- When someone foots the bill for all at social settings or at work, you will have to do the same

- Create team-building event for your team to increase cohesion

- Get a car

- Get an insurance savings plan for your children for their future education needs

- Attend to your users after working hours

- If your children cannot keep up, help them or get them tuition

- Upgrade to a private condo after living in HDB for some time and your combined annual salary goes up

- Improve your wardrobe. Clothes cannot be the same every month

- Provide for your parents

- Provide for your in-laws

- Provide for your grandparents

- Provide for your nephew/niece, godson/daughter

- Provide for your kid with Autism or Down’s syndrome

- Provide for a large part of your family, because you are doing very well in life

- to regularly donate to your church/temple/mosque

- Support your bosses wife’s MLM health product business because he helped you

- Take on additional work because a friend helped you in the past

- Take on additional work because your colleague helped you in the past

- When people allow you to guest post on their site, you have incurred intangible business debt

- Help to Pay for your Children’s University Tuition Fees

- Help to Pay for your Children’s home down payment

- To have a retirement plan and contribute towards it

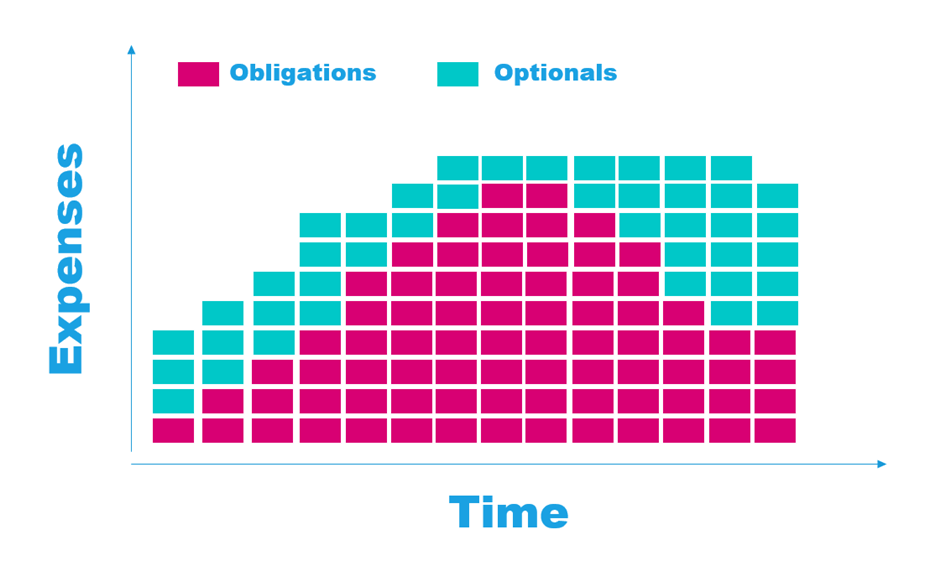

The level of your obligations have an impact on your financial independence

Obligation has an impact on your financial independence goal. The amount you need to accumulate is very much linked to your annual expense when you need it in financial independence.

If your expense is $3000/mth or $36,000/yr and you sought to spend 4% of your wealth in the initial year, you will need $36,000/0.04 = $900,000. Your subsequent year’s annual expense will increase by inflation.

There is a constant debate whether it is “safe” to withdraw 4% of your initial wealth (that is why it is called the safe withdrawal rate or 4% Rule).

My take is that the 4% withdrawal rate is deemed safe based on the body of work based on historical data we have in the USA.

In actual implementation, we often recommend forming a safe income floor + a more volatile higher return portfolio strategy. The safe income floor provides the cash flow for your essential expenses. The volatile higher return portfolio takes care of the non-essential expenses. If the portfolio performs well, harvest more for the non-essentials. If it’s the opposite, constrained your spending.

So we can look at the 4% initial withdrawal rate as a combination of the more safe 2.8% initial withdrawal rate + a variable 1.2% initial withdrawal rate.

So if your annual income is $36,000/yr, your essential expenses will be satisfied by $25,200 and non-essential expenses will be satisfied by $10,800.

For subsequent years, your $25,200/yr meant for essential expenses will rise by the rate of inflation, but should still be conservative.

For subsequent years, how much you spend on the $10,800/yr will depend on the market returns and your requirement. It can be very rules-based (check out some of the variable withdrawal strategies).

This plan, balances between conservative and flexible. You ensure that you address the security of your most basic needs and sensibly spend more if you do well, spend less when you do not.

For this plan to work, you got to be able to split your expenses to:

- Essential recurring expenses (also known as Survival or Subsistence Expenses)

- Essential non-recurring expenses

- Non-Essential recurring expenses

- Non-Essential non-recurring expenses

Obligations, are things that you MUST do.

Generally speaking, that means that they are essential to you. So they can be recurring and non-recurring.

So going back to our $36,000/yr example, if your life is filled with a lot of obligations pilling up, that means your essential expenses is a lot.

It might be so much that $36,000/yr is not enough at all, due to so many obligations.

If all your expenses are essential, then that 4% might not be very safe, based on some poor historical sequence such as the 30 year period starting in 1968 to 1998.

Most of you are risk-averse.

What this means is that you would want your plan to be rock solid and cover your bases.

So if all your $36,000/yr are essential expenses, then to be safe you would need to accumulate $36,000/0.028 = $1.285,714 instead of $900,000. This is 43% more than $900,000.

Here are some areas of obligations and money for you to think about.

How your obligations and your money & time is linked together

Whenever you set your mind to take responsibility for an obligation, do remember that inevitably, there is money linked to it.

If you look to provide for your niece education, that is a worthwhile goal.

It does not hide the fact that money will flow out of your pocket on a recurring basis for this.

If you hold a high principled life and rejected a lot of money making ways due to your obligations to your principles, recognized that monetary wise, you might be leaving a huge lump sum (an aggregate of discounted cash flow that you could have made in your job, side job, or business)

Taking on obligations need not always be about money. It involves a lot of time in certain situations.

And time and money in a lot of situations can be traded.

Knowing this link between money & time and obligations is an awareness problem.

And most of us are not aware of this if we do not explicitly talk about it.

Many could not say no to almost all their obligations to others

Some of you tend to be more altruistic and chivalrous, and take on obligations, despite your poor financial situation. Basically, you took on more than you can chew upon.

For some it’s even worse, they cannot say no. They find it very difficult to reject people.

So they ended up taking on a lot of obligations.

And since obligations sap a lot of time, and money, they end up in a tough financial situation.

The worst thing is that they do not feel good about taking on these obligations. So they end up rather drained by these obligations. If you see a purpose why you took on those obligations, you might be motivated by that challenge. When that is not your purpose, then that is a tough situation to be in.

Some past obligations slowly stop become your obligations… but we all stop being aware of them.

A lot of us planned our retirement with our financial planners at the start when we buy our unit trust.

And we never revisited this conversation again. What you think you need might have changed over time.

We also failed to see that the 25-year-old, which the original plan was based upon, is totally different from the 45-year-old as a person.

The 45-year-old sees a different life priority compared to the 25-year-old. The 25-year-old could never see his life priorities 20 years later.

When you are near retirement, you might not be so obligated about some of your obligations in the past:

- To have a car

- To provide for your kids

- Support your bosses wife’s MLM health product business because he helped you

- Join in the social activities at work to build cohesion

- Provide for your in-laws

- Provide for your grandparents

What this means is that the amount that you need for essential expenses might be very different from what you think.

It should also be said that you might lose some obligations, you might gain some obligations as well.

Be deliberate to go through and make your obligations optional instead.

I guess the opposite of obligations are things and projects that you do not always need to do. Make them optional.

The more that you can make them optional, the more you can structure a plan that is conservative and flexible at the same time.

For example, the following can be pushed to optional:

- Help to Pay for your Children’s University Tuition Fees

- Help to Pay for your Children’s home down payment

- Provide for a large part of your family, because you are doing very well in life

- to regularly donate to your church/temple/mosque

- Support your bosses wife’s MLM health product business because he helped you

- Take on additional work because a friend helped you in the past

- Take on additional work because your colleague helped you in the past

- When people allow you to guest post on their site, you have incurred intangible business debt

- Upgrade to a private condo after living in HDB for some time and your combined annual salary goes up

- Improve your wardrobe. Clothes cannot be the same every month

- Give the Market Rate Ang Bao during Your Friends Wedding

- If you are the Boss, you give more to be respectable

- Join in the social activities at work to build cohesion

- When someone foots the bill for all at social settings or at work, you will have to do the same

- Create a team-building event for your team to increase cohesion

- Get a car

- Get an insurance savings plan for your children for their future education needs

- Attend to your users after working hours

- Find a partner

- Propose with a Diamond Wedding Ring

- Hunt for a Wedding Shoot, Select and Do the Shoot

- Do a Wedding Banquet

- Get Married

- Have 2 children (because having one will eventually make the child lonely)

When you move more to options you can essentially form an annual expense of Essentials and Non-Essentials.

With that at least you can estimate the amount you need to accumulate to cover the essentials based on a safer initial withdrawal rate. Because the essential amount is smaller, you need to accumulate less.

But obligations can be a big source of motivation.

I had this conversation yesterday with some of my co-workers on why Singaporeans work and why Singaporeans play games.

They seem to think that gaming is to fill a void and that work can never be meaningful.

I asked: “Then why do people work long hours? How can you say they do not like work?”

So their response was that work is poor, but it is better to use work to fill the “empty void” than not working and have that empty void.

I was astounded by this, and perhaps why we have people in the office functioning like zombies.

Obligations, while it forces you to do something that might be out of your comfort zone, can be used as a positive motivator. If it is a philosophy that you feel strongly about being committed to, then it becomes the driver to push you through challenging times.

Research has shown that there are folks that didn’t respond to retirement very well because there is a 180 degrees change in their life.

They were engaged in something that, they might not know its purposeful, to a situation where there is no purpose at all. That loss of purpose affects them as a virus would.

Without obligations -> Nothing on the line -> Very little dependence on you -> People do not need you -> You feel less significant of your position in society -> You questioned your existence -> You will have a large void to fill up.

Curate your Obligations during Accumulation and Financial Independence

I think we often do not discuss our responsibilities as a subject for wealth accumulation and financial independence.

If we frame our time and money in terms of responsibilities and obligations, it will allow us to right sized it.

A recent article by New York Times explained that the best way to figure out your expense is not to talk about what you had spent in the last few years.

It is more to talk about what you would do in a typical day and then figure out the amount of wealth that we need to support that.

And that is probably the right way to think about your obligations and responsibility. Go through what you have now and what becomes more optional. Also, go through what new responsibilities that you would want to add in now that you do not have a job anymore.

Then we would be able to work out how much you have now, versus how much you need to spend and assess if your plan is still safe.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

steveark

Thursday 26th of August 2021

OK, as a US guy what do JC, poly and NS mean? As far as obligations, a lot of what you listed looked cultural or regional. We never had to take care of our three grown kids, they are financially successful and off the bank of mom and dad. They get to make their own down payment on houses and never had any student loans, they got free college based on their test scores. We never had to take care of parents, they were debt free with lots of assets they handed down to us when they died, both mine and my wife's. But they were only middle class at best, not rich people. They just avoided debt and ended up with money and land by the end of their lives. Our wedding might have cost $200, no diamond ring and a church venue that cost us maybe $25 paid to the preacher. Our kids followed suit, the two that are married eloped and were married without guests for almost no cost, the most recent was a Covid Zoom wedding. We bought one house for about one years pay and are still in it 42 years later. I was the boss and felt no pressure to have better stuff than the people who worked for me, in fact they had bigger houses and nicer cars. What did I care, I had more than enough. That stuff doesn't make you happy, relationships make you happy. And I had good kids and a wonderful wife and great friends. The obligations I have now in retirement are ones I chose, non-paid work for nonprofits that help others achieve success. Its work that makes me happy because I'm making a difference in the lives of others, usually people less fortunate than me.

Kyith

Saturday 28th of August 2021

Hi Steve, not sure if you are currently residing in Singapore. JC stands for junior college and poly stands for polytechnic. these are probably equivalent to your high school in the US. NS stands for national service. As male Singaporeans, it is mandatory that we have to serve 2 years in the army.

Rainbow Coin

Monday 25th of March 2019

Perhaps at some point in time, we would "outgrow" the obligations or wake up to the fact that certain obligations don't matter anymore (eg. when favour has been duly returned, realized that the other party is trying to take advantage of us etc).

However, it might not be easy for us to just let go of our obligations, despite that many of these obligations do not spark joy and can be (financial) burdens. Because we often need to consider the intricacy of issues associated with these obligations such as "face", status and relationships. When we weigh wealth against the intangibles, things often cannot be very clear cut.

Kyith

Saturday 30th of March 2019

It is not so clear cut. However, I would contend to say it is the lack of awareness that obligations deals with money, and by merely collecting less, our lives are better off. Thanks for visiting Rainbow Coin.