I think last year Nov 2018, I wrote a post introducing everyone to MoneyOwl.

If you are financial savvy, take control of your finances, you would have an idea how much insurance coverage you are looking for. You can then survey the different prices for the same type of insurance coverage and see which one offers the most competitive prices, and which one suit your needs,

Then you can purchase the insurance protection, and not afraid of advisers hounding you to purchase some higher value added policies.

And there are the readers who knows that you should get protection, are not sure what are your needs, but would want someone dependable and conflict free to speak to, MoneyOwl is also the right solution.

So that is the protection solution.

In March this year, MoneyOwl rolled out a Digital Will Writing service. This will service is useful for you, if the way you would like to will your assets is not too complicated.

What is missing is the investment service and this is what I am here to update everyone.

Implementing Wealth Management the Right Way

MoneyOwl is a joint venture between Providend and NTUC Enterprises. NTUC Enterprise is the holding entity for the Labour Movement’s social enterprises which collectively serve more than 2 million customers.

As a subsidiary of NTUC Enterprise, MoneyOwl’s social mission is to help working families make the best possible financial decisions, so that all Singaporeans can achieve greater financial security, better retirement adequacy and be empowered to live fulfilling lives. NTUC decided to collaborate with Singapore’s first fee-only financial adviser and well-known in the industry for its deep expertise in comprehensive financial planning and for championing ethical advice.

We do get the feeling that the government sense that the current wealth management space is “a little uneven”, and wish to take the lead and shape the direction of the industry by participating directly in it.

As a financial commentator for probably 14 years in this space, I like what I am seeing here.

If I have an acquaintance that needs help to grow her money, evaluate her financial protection, there is always the lingering thing at the back of my mind asking yourself: “Is this the right adviser to help my friend? Will things turned out in ways I didn’t anticipate?”

Having them around solves a fair bit of these issues.

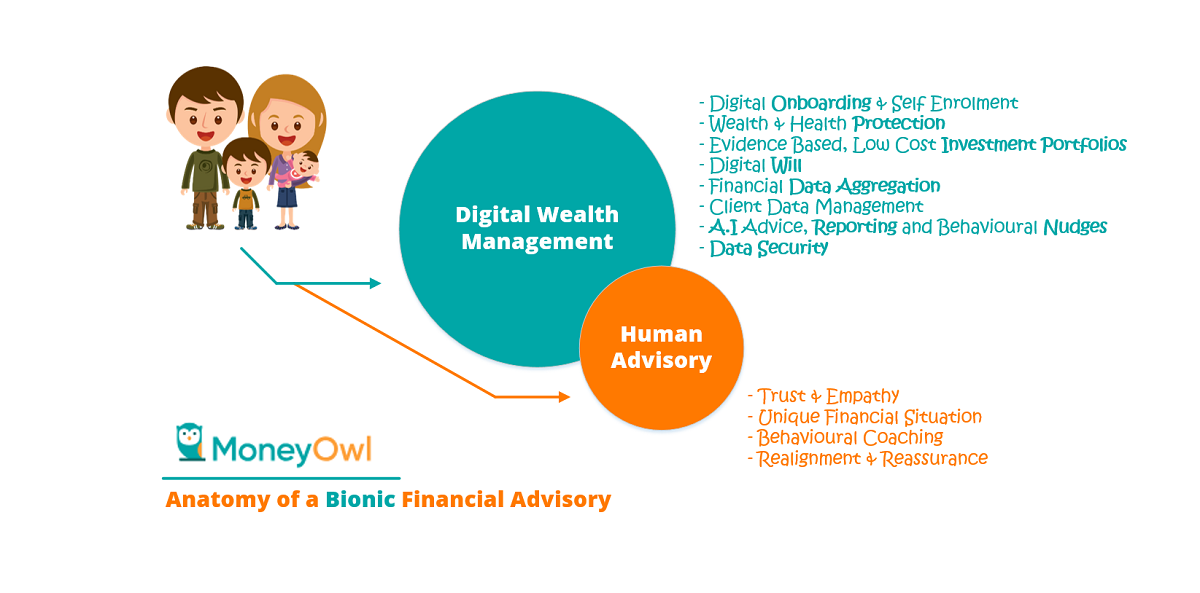

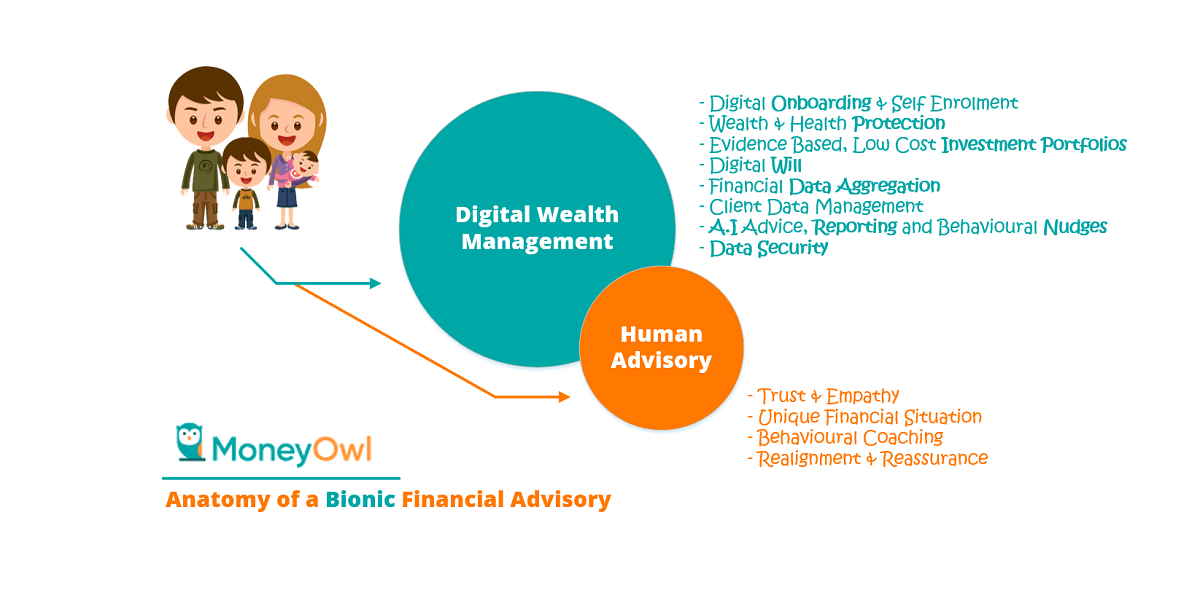

MoneyOwl provides the following service:

- Protection Robo. Guides you to pick the right insurance protection to hedge your life risk

- Self-checkout Insurance Protection. If you know the protection that you need, you can purchase it from MoneyOwl and not be up-sell on other protection

- Digital Will Robo. Allows you to create your own will, so that you can have a peace of mind how your assets would be passed down

- Investment Robo. Provides 5 different low cost portfolios, which allows you to build wealth through buy and hold

- Comprehensive Financial Planning. More to come later

Leveraging on technology, and automating work flows that used to be crumble-some seemed to be the way to go but MoneyOwl is actually more than that.

They prefer to be known as Bionic, which means a combination of technology and human touch.

I do agree that to a certain extend, not everything can be automated. There are aspect of wealth management that can be automated and others that require hand holding.

Perhaps I will go through some examples to let you have an idea why I think MoneyOwl’s service will provide invaluable to you.

MoneyOwl’s Investment Robo

This article is to let you guys know more about MoneyOwl’s Investment Offering.

After they have first provide you with a fundamentally sound way to hedge the risks in your life, the next objective is to answer the question: How do I accumulate my wealth in a fundamentally sound way?

This ties in with the third question they already attempt to help you address, which is: How do I ensure that when I passed on, the wealth is distributed in a way that I want.

Everyone has a philosophy how to build wealth and MoneyOwl is no different:

- Focus on asset allocation – do not take country, sector or firm-specific risks

- Go for market-based return – it is hard to consistently beat the markets through active management

- Keep costs low – the difference compounds big time, over time

- Stay invested for the long term – time in market, not time the market!

I actually think this is the “default” way we should build our wealth, if we do not have the time to mess around with more active approach to wealth building (even if you mess around, it does no mean that your results would be better. Sometimes it will be worst off.)

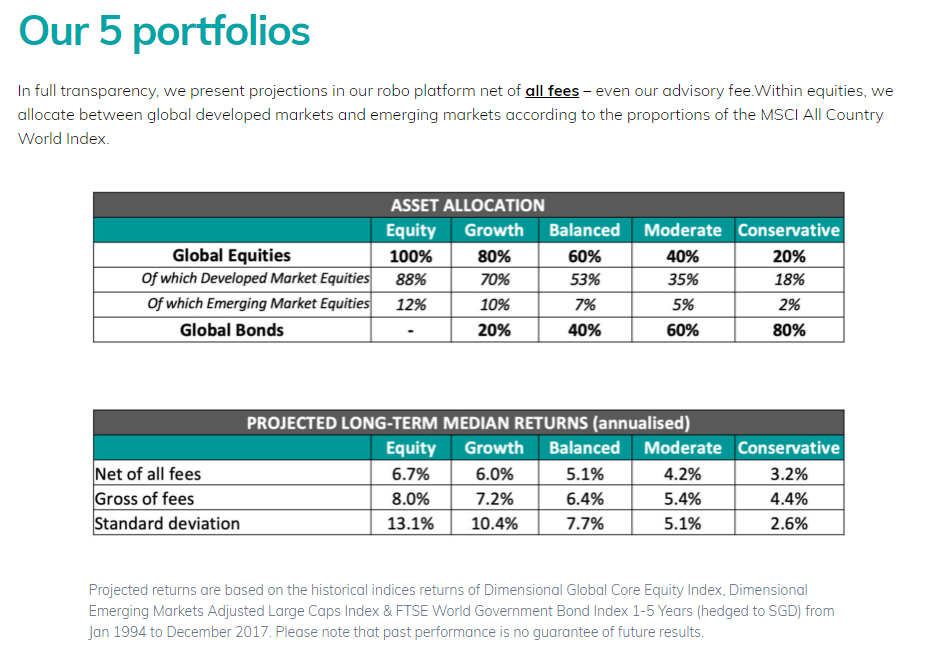

MoneyOwl will provide wealth builders in Singapore 5 different portfolios to invest. These portfolios differs based on their allocation between equity (stocks) / bonds.

These are the 5 portfolios:

The 5 portfolios ranges from conservative to equity, with equity being the most aggressive. The aggressive portfolio have a higher equity allocation while, the more conservative portfolio have a higher bond allocation.

The 5 portfolios ranges from conservative to equity, with equity being the most aggressive. The aggressive portfolio have a higher equity allocation while, the more conservative portfolio have a higher bond allocation.

MoneyOwl took their time to evaluate the investment products out there, and they decided to work with Dimensional Fund Advisors (DFA) from USA to structure these 5 portfolios with 3 low cost, evidence based funds:

- Dimensional Global Core Equity Fund (Developed Market Equities in the table)

- Inception in 2017 Jul

- Currency: SGD

- Benchmark: MSCI World Index (net Div, SGD)

- Total Assets: S$4.5 bil

- ISIN: IE00BF20L879

- Dividends: Accumulating

- Expense Ratio: 0.35%

- Factsheet

- 7776 Global Stocks

- Dimensional Emerging Markets Large Cap Core Equity Fund (Emerging Markets Equities in the table)

- Inception in 2017 Jul

- Currency: SGD

- Benchmark: MSCI Emerging Markets Index (net div., SGD)

- Total Assets: S$706 mil

- ISIN: IE00BF20LB02

- Dividends: Accumulating

- Expense Ratio: 0.50%

- Factsheet

- 922 Emerging Market Stocks

- Dimensional Global Short Fixed Income Fund (Global Bonds)

- Inception in 2017 Jul

- Currency: SGD

- Benchmark: FTSE World Government Bond Index 1-5 Years (hedged to SGD)

- Total Assets: S$4 bil

- ISIN: IE00BF20L549

- Dividends: Accumulating

- Expense Ratio: 0.29%

- Factsheet

- 181 High Quality Bonds

- Yield to Maturity: 2.18%

- Average years to maturity: 3.67 years

MoneyOwl provided the annualized returns, based on the back tested results from 1994 to 2017. There are two returns provided, with fees and without fees. This is so that they are transparent about the fees you are being charged in different ways. (which a lot of financial institutions are not upfront about)

Why use Dimensional Funds?

Dimensional have been in the wealth management business in USA for the past 4 decades.

They are not a familiar name in Singapore, but I suspect there will be more discussions in the future. You can refer to this page to know more about Dimensional.

To put it simply, they are the Smart Beta funds before smart beta became a popular thing.

Here are some of the fund’s characteristics:

- They are not exchange traded funds (ETF), which are listed on stock exchanges whose prices are updated real time. Dimensional funds are unit trusts. Their prices are updated end of the day

- Unlike the unit trusts that you see distributed in Singapore, Dimensional funds are low cost. Their expense ratio ranges from 0.29% to 0.50% compared to the typical 1% to 3% expense ratio of unit trust

- Dimensional funds do not pay trailer fees to the distributors. Not many know that your typical unit trust have a high 1% to 3% expense ratio, but a large proportion of this is paid by the unit trust to the distributors like Fundsupermart, Dollardex, POEMs and the banks as a fee for distribution. So even though they charge 0 platform fee, they get paid from you indirectly. That is how they can survive

- Dimensional funds are passive funds but they are not indexed. Savvy investors would know that investing in low cost index funds/ETFs that follows broad based benchmark index like the MSCI All Country World Index is the way to go. Index funds are passive because instead of a human fund manager who selects what stocks or bonds to buy, hold and sell, a machine sought to mirror the index fund’s net asset value as close to the index as possible. For Dimensional funds, they are similar in that they have a machine at the back end to position their portfolio. However, they do not mirror an index. Rather, they systematically buy, sell and hold based on a few persistent and pervasive factors

- Building on to #4, Dimensional funds are factor based. They based their buy, sell and hold on factors that are not just persistent but pervasive. These factors are:

- Overall Market (Beta)

- Company Size (Small Cap over Large Cap)

- Relative Price (Low price to book over High price to book)

- Direct Profitability ( High profitability over low profitability)

- You can only buy Dimensional funds through DFA trained advisors. They believe that advisors play a very big role in delivering alpha

- Dimensional funds are taxed optimized and therefore reduces tax uncertainty. Unlike popular low cost index ETFs listed in other countries, these Dimensional funds are domiciled in Ireland, and are much efficient in dividend withholding tax and estate duty / inheritance / death tax for foreign financial asset holdings

The way I look at MoneyOwl’s investment portfolio is this way:

- You believe that certain factors are persistent and pervasive. These are backed by extensive research. They will eventually deliver good performance

- You believe in keeping your costs low. Dimensional funds have low expense ratios

- You wish to have adequate clarity and eliminate tax uncertainties from your wealth building

- You do not wish to spend your effort actively managing your investments. You prefer to focus your effort on your job, your family

- You know what I am saying, but maybe you don’t really know. You would prefer to have companions that have integrity to guide you along this path

- You wish you can setup a recurring payments instruction, and let your bank automatically funnel money to your investments without you triggering it. This will take you out of the loop and be less affected by market fluctuations

If this fits you, then MoneyOwl’s portfolio might be something you are looking for.

My Comprehensive Article on Dimensional Funds

A few weeks ago, I wrote an article introducing Singapore readers to Dimensional funds.

There is only this much that I can cover in this article, so I do hope that those are interested, you can read it. Warning: It is likely you cannot finish it in one sitting. Bookmark and read it over the week on your daily commute.

The article covers:

- The targeted market for a group of funds like this

- How do we build wealth, on a high level with DFA funds

- Introducing the Dimensional Funds

- Explaining Evidence Based Investing

- Examining DFA Results including rolling equity expected returns data

- Breaking down the Cost Stack and Comparisons

- Explaining the Adviser’s Alpha

- Breaking down Dividend Withholding Taxes and Death Taxes

- The Case to Invest in a Global Equity and Bond Portfolio

Should Singaporeans Invest in Dimensional Fund Advisors (DFA) Funds? My Comprehensive Take >>

The Total Fee Stack for MoneyOwl’s Investment Portfolio

When you invest in other investment products, there are great emphasis placed on performance returns.

Less on the cost.

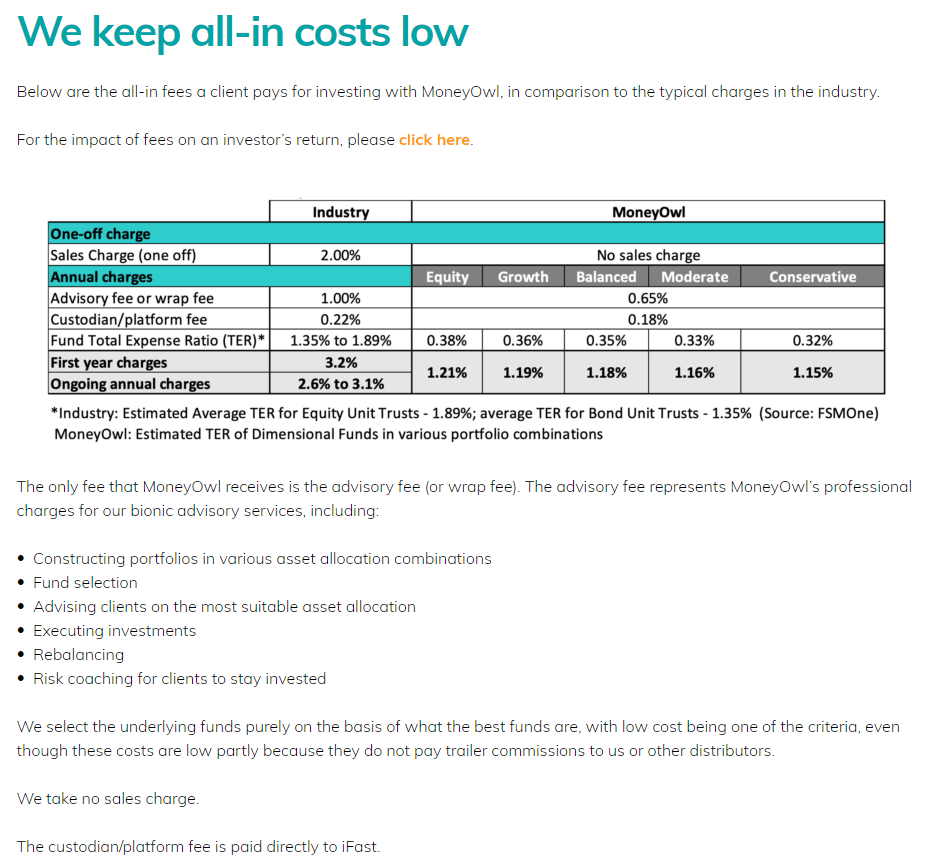

MoneyOwl would like to be transparent with the fees that they are charging.

That is why they provided a cost stack of their portfolio’s versus the industry:

We observe that the total costs for the 5 portfolio range from 1.15% to 1.21%. This compares against the recurring fee of 2.6% to 3.1% that MoneyOwl estimates.

We observe that the total costs for the 5 portfolio range from 1.15% to 1.21%. This compares against the recurring fee of 2.6% to 3.1% that MoneyOwl estimates.

Cost is a big issue because your returns are uncertain, but your cost, rain or shine, make money or not, you have to pay it. And it is worse that you pay a big chunk of it.

If you would like to see how MoneyOwl fare against the DIY ETF solutions and other Robo platforms like Stashaway, Autowealth, Smartly, you can read my comprehensive article, where I go into deeper comparisons.

The summary that I gather is:

- The total cost stack for the Robo platforms are roughly the same around 1.2% to 1.7% but mostly around the 1.2% range

- The DIY ETF solutions depends on which broker you use. With the right broker, the DIY ETF solution is the lowest cost

MoneyOwl charges a advisory fee or wrap fee of 0.65%/yr. As they are making use of iFast’s platform, you have to pay iFast a platform fee of 0.18%/yr.

Some readers in some Telegram chat have asked, how is the advisory fee, platform fee and expense ratio taken from me?

Let me address the expense ratio first.

Like your typical unit trust or ETF, the expense ratio are incur in the underlying Dimensional fund itself. It is transparent to you (which is why a lot of investors ignore it because they do not see it! They think it does not matter!). The returns that you see in the factsheet, annual report are net of the expenses. In fact, if you read the annual report of the Dimensional funds, you would see how much expense is incurred. It will give you a better understanding.

With regards to the advisory fee and iFast platform fee, they are deducted by selling the units in the best performing fund.

Advisory fee are deducted in April, July, Oct and January. The deductions are reflected in the statements for these months. Note that the months corresponding to each deduction are as follows:

- Deduction in April: Fees for Dec to Feb

- Deduction in July: Fees for Mar to May

- Deduction in October: Fees for Jun to Aug

- Deduction in January: Fees for Sep to Nov

For example, the fees for Mar to May are deducted in Jun and this is reflected in the quarterly statement given to the client in July.

The Investment Process

One of the great thing about MoneyOwl is that as a social enterprise, they want to make it easy for people of all income levels to start investing.

Thus the minimum investment amount for lump sum investment is $100 and the minimum amount for recurring investment is $50 per month.

This means the hurdle to give the platform to try is really, really low!

Like a lot of Robo platform, MoneyOwl will not let you choose which portfolio you would like to get invested.

Instead, they would recommend you a portfolio based on:

- How long is your investment horizon

- Your willingness to take risk

To invest with MoneyOwl, you would have to be at least 18 years old.

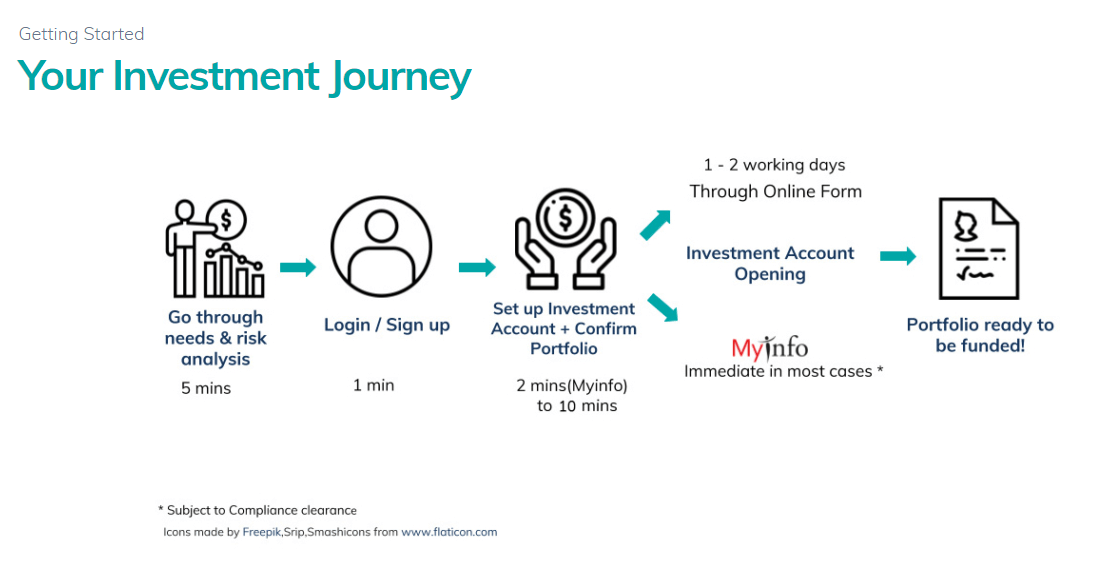

The following illustrate the investment process:

- You will first go through a needs analysis. The end result of the needs analysis is to identify which of the 5 portfolio is suitable for you to invest

- Then you will create an account, or login

- MoneyOwl will facilitate the account opening

- Then you can fund your portfolio with money to get invested

Now let us briefly go through the process.

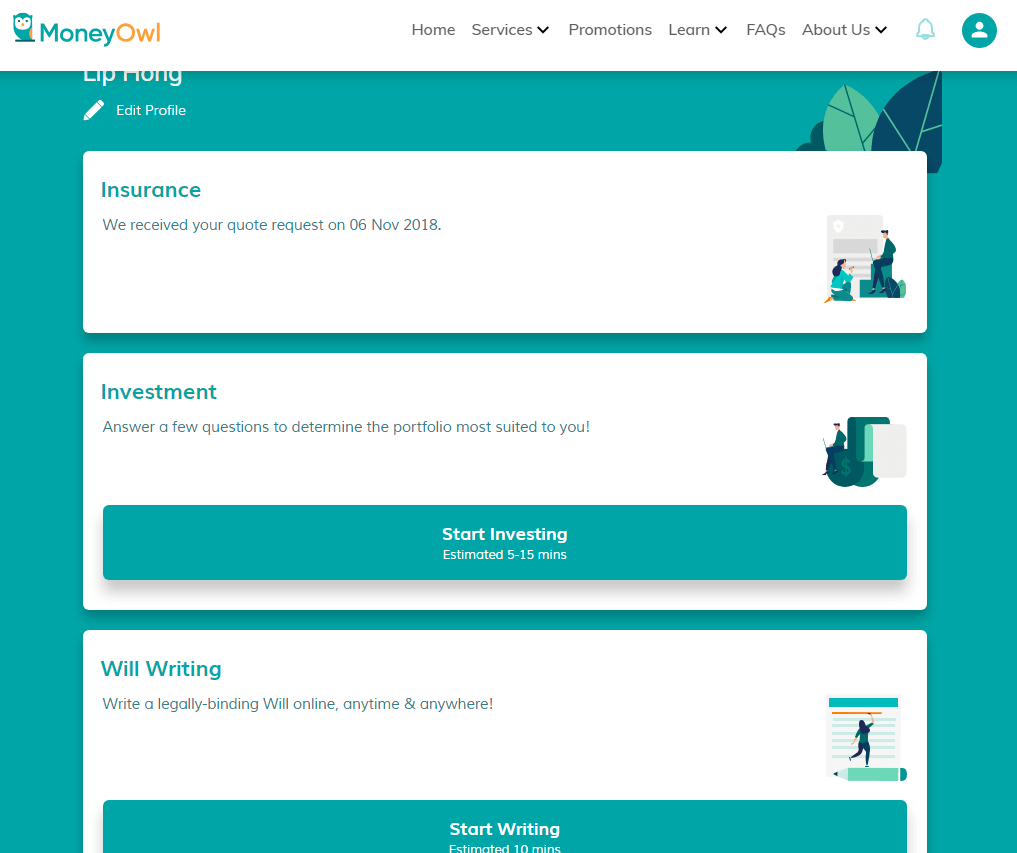

To get started investing, you can go through this link here >>

If you have an account like myself with MoneyOwl, you can click on Start Investing to go through the process.

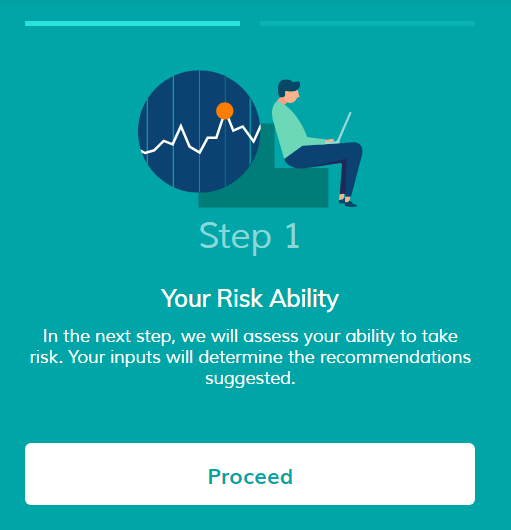

1. Needs and Risk Analysis

The first part of the needs analysis is to assess your risk ability.

If the tenure to which you need to use the money is very short, then it might not be wise to invest. In the screenshot above, you can see a selection of 1 year (genuine for me, if I were to retire next year), MoneyOwl do not even let me invest.

Which begs the question of, what if I wish to retire and spend down my money? I would still need equities. I will still need bonds.

I think right now, MoneyOwl caters more to wealth accumulation not retirement.

If I select an investment horizon of 5 years, MoneyOwl will let me continue.

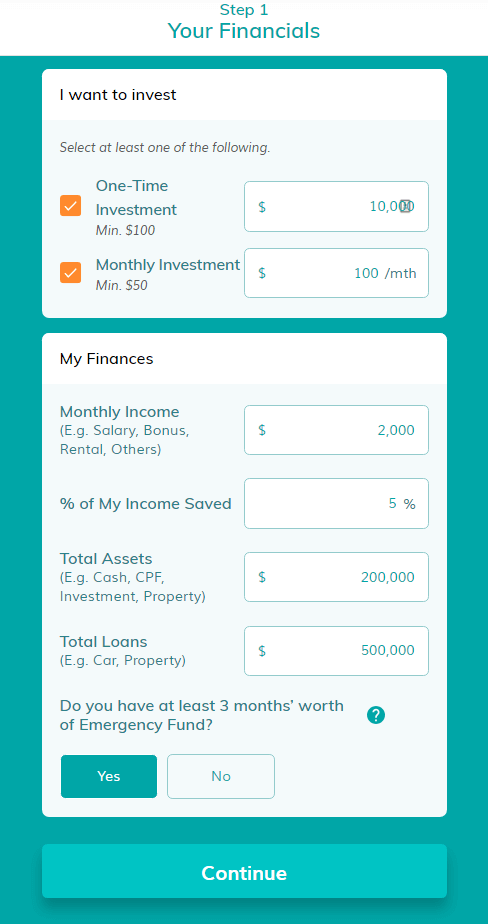

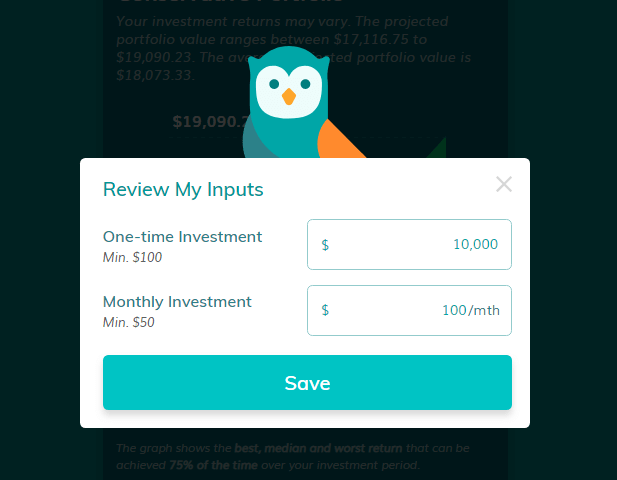

The next step is for me to specify how much I would like to invest in one lump sum and on a recurring basis.

The next step is for me to specify how much I would like to invest in one lump sum and on a recurring basis.

I realize that you have to invest a minimum lump sum of $100, even if you decide that you wish to invest on a recurring basis. You will also specify your finances such as your monthly income, your savings rate, the assets and liabilities you have.

I tried clicking that I do not have emergency fund. If I do not have emergency fund, I cannot invest as well. Which is the standard financial planning advice.

You should have at least 3 month’s worth of emergency fund before you invest.

If the percentage of income saved is less than the recurring amount that I wish to contribute, MoneyOwl will warned me as well.

The next step is to answer 4 questions to show my willingness to take risk. This is to let you, and MoneyOwl have a basic behavioral check to see where your risk tolerance is at. It looks like I am rather tolerant to some negative downside.

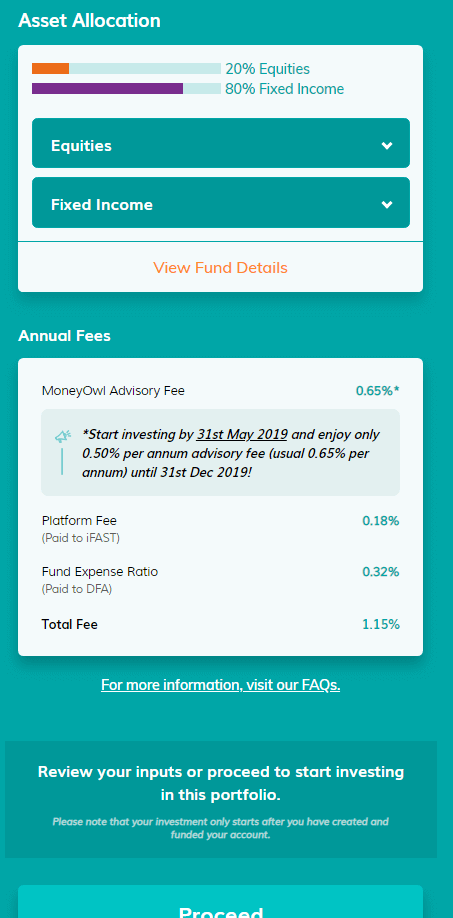

The result of the needs analysis is an output of the portfolio chosen for me. There are 2 parts. The first part shows me that, if I were to put in $10,000 and $100/mth, how much my money would grow to.

MoneyOwl will show you based on their historical results the amount you would accumulate. My capital put in will be $15,900 and in the worse case it would grow to $17,116 in 5 years.

The second part shows you the portfolio selected for yourself, the breakdown of the fees.

At this section, you can change your one time investment contribution and monthly investment amount and MoneyOwl will recalculate the wealth growth model for you.

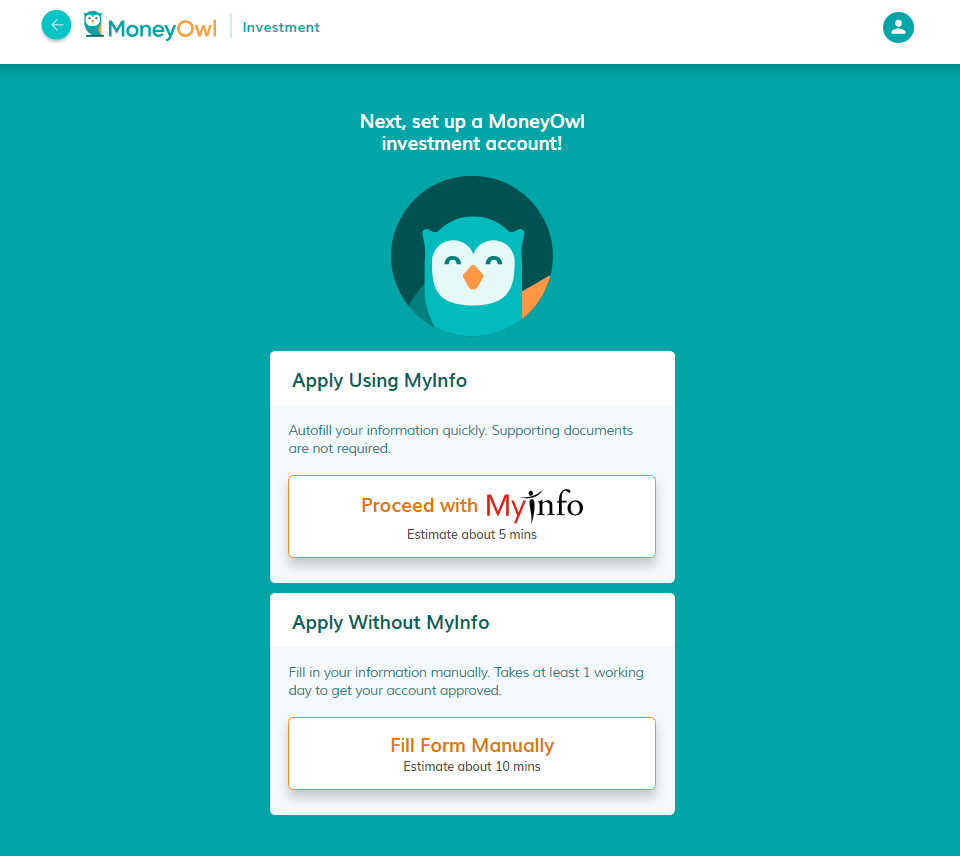

2. Opening your Investment Account

The next step is to open your investment account.

The next step is to open your investment account.

The filling up of information is done online. This makes it rather easy to open an account.

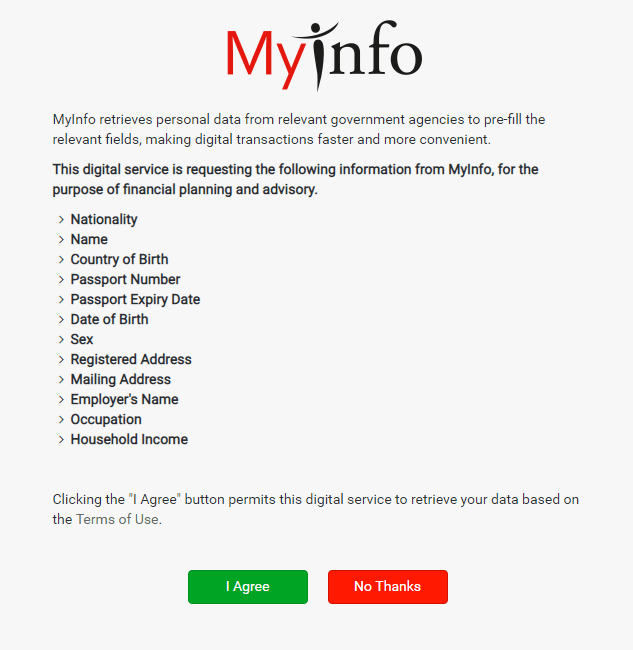

What is more, you can make the process smoother by choosing to authorize MoneyOwl to pull your read only info from MyInfo.

You will need a SingPass authentication.

Once you have authenticated, you will then authorize MoneyOwl to retrieve the information above.

If you do not wish to pull information from MyInfo, you can fill it up manually yourself.

Once you have finish this portion, your investment account is setup.

You are ready to fund the account.

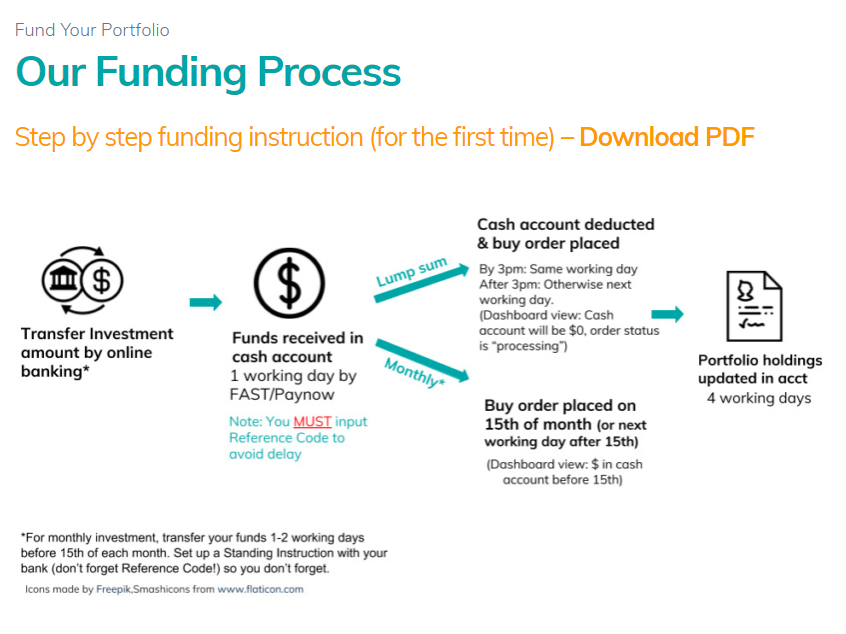

3. Funding Your Investment Account at MoneyOwl

The illustration above gives you a clear idea how the funding process will be. For those who have invest in unit trust, this is not to different.

You will fund the Investment account by:

- Transferring using Online Bank Transfer via FAST

- Transferring using PayNow

Both methods are pretty similar and it would be instantaneous for the money to be transferred from your bank account to your MoneyOwl’s account.

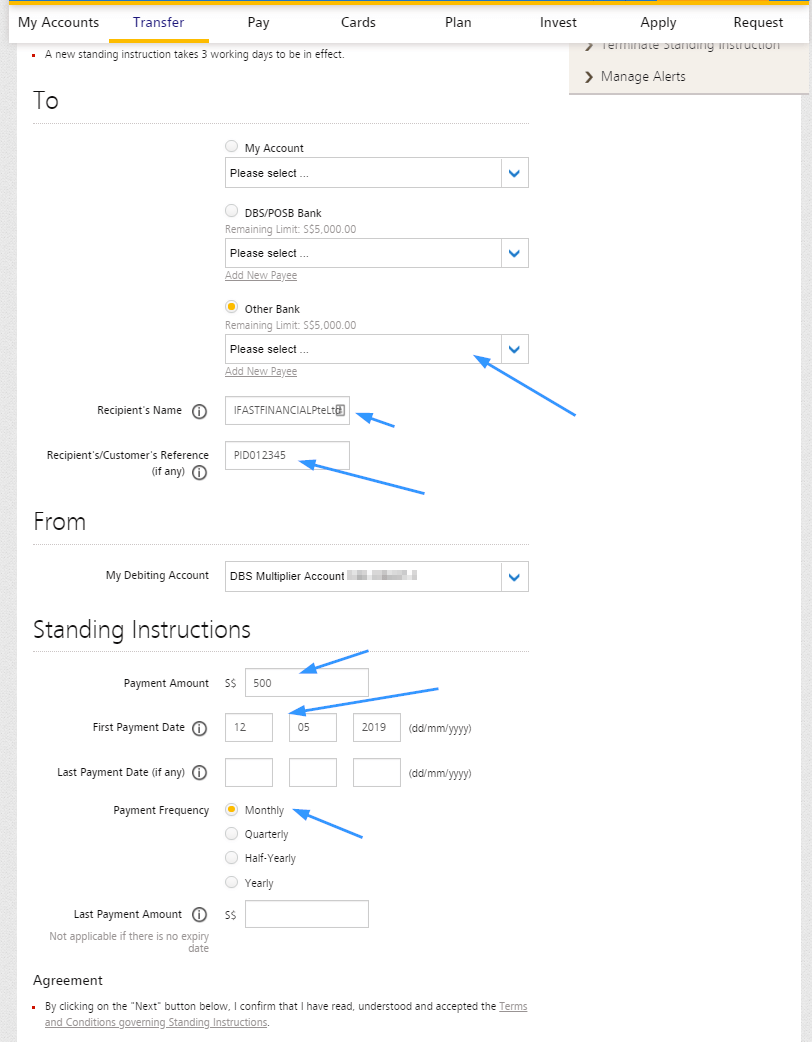

There are different set of standing instructions, and you can refer to a more detail instructions here >>

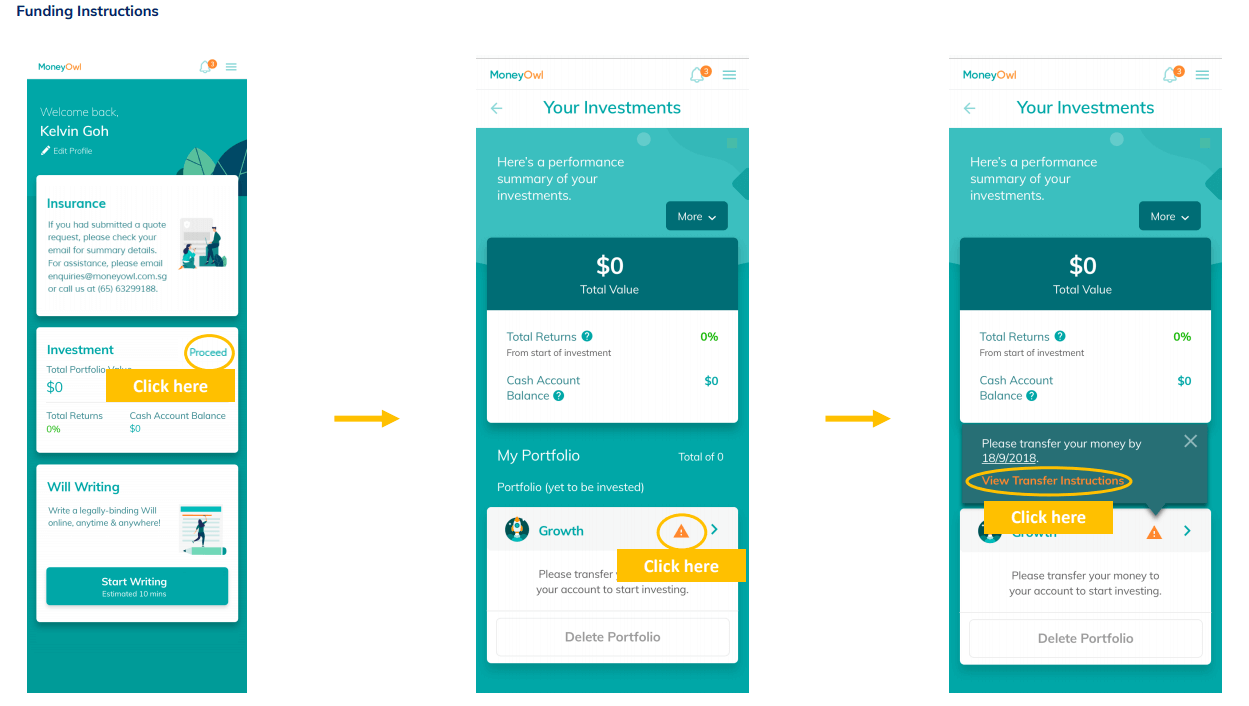

If you have not fund your account, if you go into your portfolio, you will see a orange triangle. Click on it, it will show you the funding instructions.

The funding instructions will contain iFAST Financial’s bank account for you to fund to.

Note: If you look at the instructions, it tells you how important it is to key in your Reference Code in the transactions.

You can then go to your bank or your PayNow app to pay. Remember to key in your personal Reference Code.

For recurring transactions, you can also go to your bank and set up a standing transaction like the screen shot above. Note that MoneyOwl will deduct the money on the 15th of the month, so it is advisable to transfer in a few days before the deadline.

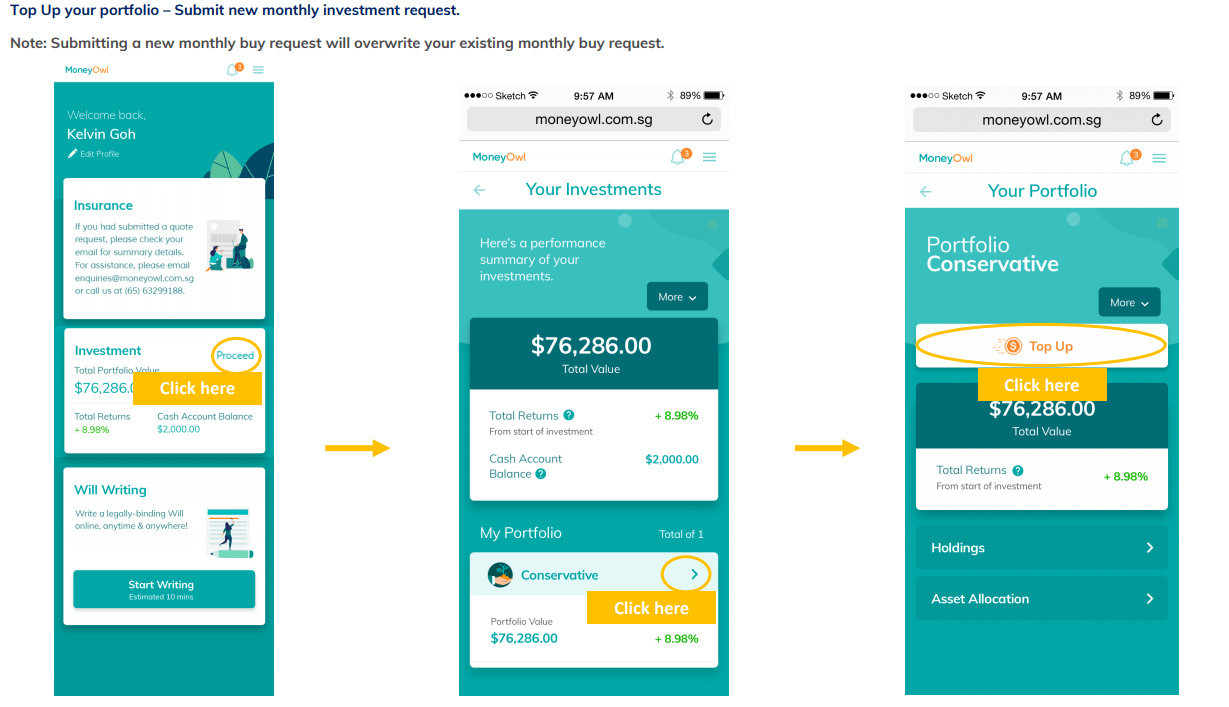

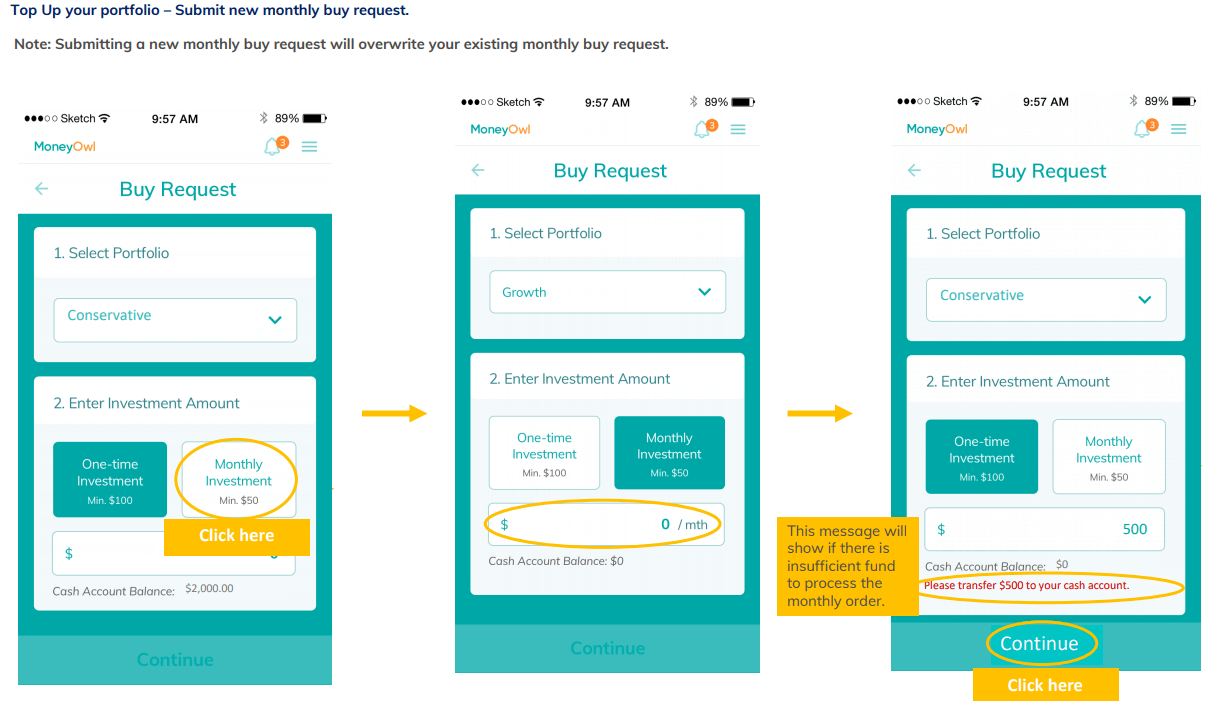

When you have a pay increment and would like to put away more, you can always change the amount you contribute. This is so that MoneyOwl can deduct a higher amount on a monthly basis.

MoneyOwl is Audited and Certified ISO/IEC 27000

It might be tough to trust money to a start up. It is also tough to trust that people will not break into the platform and steal your private information, your passwords and other data.

We have seen a lot of popular website fall prey to this.

Even established websites were caught storing certain of your passwords in clear.

MoneyOwl is ISO27001 certified. The ISO27001 certification is a mark of recognition that a company has met the international standard for establishing, implementing, maintaining and continually improving its information security systems and processes.

The Adviser’s Alpha – Improving your Sophistication So that You can Build Greater Wealth

I do observe that there are quite a bit of comments asking whether it makes sense to pay the 0.65% advisory wrap fee and the platform fee.

And I think that if you are wondering about this, it means that:

- You know that cost matters

- You prioritize cost over other investment conveniences

- You are likely more sophisticated and competent enough to educate yourself how to build wealth through passive investing over the long term

In this case, MoneyOwl might not be right for you.

One good test is whether you could finish my Dimensional article, understand the stuff and do not have much questions after that.

If you are able to overcome that and think it is a good refresher, then you are probably more suited to DIY your passive investing.

I think as a NTUC Enterprise, they will be glad that more of you guys are that sophisticated and build wealth soundly on your own.

Even so, I do feel that many of us do not know what we do not know.

I went over to Seedly, and tried to pick out some questions that you might have. You realize that you have a gap in understanding about an investment strategy that you thought it is rather simple.

I went over to Seedly, and tried to pick out some questions that you might have. You realize that you have a gap in understanding about an investment strategy that you thought it is rather simple.

What you were expecting is very different from what the strategy delivered.

And these doubts usually surface, in the face of some losses. 2018 is probably a good test and we see a few of these examples here.

You might know that you should invest for the long term, but the problem is the head may understand this during “peace” time but when the markets start tumbling, the heart may not follow what the head knows:

- If you DIY, you might not key in that buy order that you normally do on a monthly basis

- You might cancel your standing order to make more contributions to MoneyOwl

The above chart is the famous Dalbar study.

It shows the 20 year annualized returns of various kinds of asset class.

Notice the worst performer. It is the Average Investor.

Why did the average investor do so poorly? Dalbar cites a few reasons:

- Panic selling during market downturns.

- Exuberant buying at market highs

The strategy to invest passively is simple. The tough part of investing is to stay in the game and navigate the storm in your head when things get volatile.

What MoneyOwl sought to do is to get you to be more sophisticated about investing.

The first way is to give you access to a human adviser, when you need them.

With MoneyOwl, if you have doubts like these, you can have a human adviser, paid a salary, to

- clear your doubts

- frame things in a different way for you

- work with you together to see the best way going forward

The difference between an adviser and asking in an open forum, is that they are your adviser, know your situation and are able to go deeper into your specific situation. As a social media commenter, we do not know your specific situation and could only give our advice based on what we can gather and interpret.

An example of what these advisers can do for you is to confirm your risk appetite decisions.

While MoneyOwl have a good set of risk questions to ascertain that, your willingness to take risk is really a matter of the heart, influence by many factors that are complex enough that a robo might not fully empathize. Their advisers will be there to provide the judgement so that you can make the correct investment decisions that will help you stay invested when markets become volatile.

Secondly, MoneyOwl will seek to produce more educational materials, in different medium to attempt to get you sophisticated about passive, evidenced-based low cost investing:

- Written content

- Video content

- Easy to digest infographics

- Investment Symposium

The idea is to create a MoneyOwl University for Passive, Evidenced-Based Low Cost Investing.

MoneyOwl already have a team of financial literacy trainers providing education to investors.

If MoneyOwl do all the above well and together with you, the chances of you staying invested will be much higher when the markets start to become rough. But when the “shit really hits the fan”, besides doing more education through articles, videos, and events, you can be sure MoneyOwl’s advisers will be on hand to guide you through the storm. You always have access to them.

Summary

Ultimately, I think as a starter MoneyOwl have come up with a rather sound, comprehensive product for the masses.

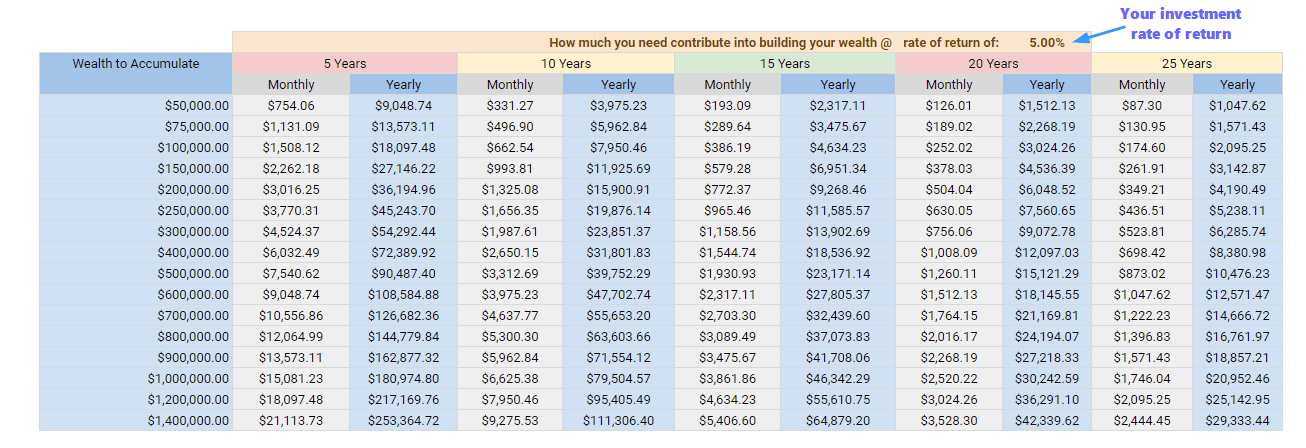

If there are some last minute take away from this it is to ask yourself: Why do you want to build wealth? What is your reason to accumulate?

The table above, provides you with an easy look up table to show you that if you need $X , how much monthly and annual capital you need to fund the wealth building.

MoneyOwl is not a magic bullet:

- You need to earn more so that you have more personal free cash flow to put into investing

- You need to consistently channel contribution on a monthly or annual basis to build wealth

MoneyOwl provides you with a sound solution if your philosophy is the same as them:

- Focus on asset allocation – do not take country, sector or firm-specific risks

- Go for market-based return – it is hard to consistently beat the markets through active management

- Keep costs low – the difference compounds big time, over time

- Stay invested for the long term – time in market, not time the market!

And this is the kind of investment you are looking for:

- You believe that certain factors are persistent and pervasive. These are backed by extensive research. They will eventually deliver good performance

- You believe in keeping your costs low. Dimensional funds have low expense ratios

- You wish to have adequate clarity and eliminate tax uncertainties from your wealth building

- You do not wish to spend your effort actively managing your investments. You prefer to focus your effort on your job, your family

- You know what I am saying, but maybe you don’t really know. You would prefer to have companions that have integrity to guide you along this path

- You wish you can setup a recurring payments instruction, and let your bank automatically funnel money to your investments without you triggering it. This will take you out of the loop and be less affected by market fluctuations

Check out MoneyOwl’s Investment solution here >>

Here are some further readings on their investment solutions:

- The Right Portfolios: Putting it together

- The Right Building Blocks: About Dimensional and Nobel prize-winning research

- The Right Way to Invest: Keys to a successful investing experience

- Why Unit Trusts and not ETF?

Exclusive: MoneyOwl Investment Symposium in 25th May 2019

If you would like to find out further how to build wealth with Dimensional portfolios, and have further questions regarding the way MoneyOwl structure their investment offering, MoneyOwl will be organizing a 3 hour session at One Marina on a Saturday at NTUC.

The speakers will be:

- Ms. Chuin Ting Weber, CEO & CIO, MoneyOwl

- Mr. Christopher Tan, Executive Director, MoneyOwl / CEO, Providend Ltd

- Dr. Chen Peng, CEO, Asia ex-Japan, Dimensional Fund Advisors

The event is FREE. Register here >>

This post is Sponsored by MoneyOwl. The views are Kyith’s.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- New 6-Month Singapore T-Bill Yield in Late-April 2024 to Drop to 3.70% (for the Singaporean Savers) - April 18, 2024

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

Tan

Saturday 4th of May 2019

Hello. What are your views when compared to lion global all season fund? I can further save on platform fee if i invest lion global fund using dollardex right?

Sinkie

Friday 3rd of May 2019

The ideal "put money where mouth is" comparison is for all Robo's to put out backtest performance of all their portfolios over the last 10, 20, 30, 40, 50 years, inclusive of all fees & expenses.

Since this is backtested, all pertinent information should be either available or can be constructed. Even S&P is able to re-construct the S&P500 index all the way back to the 1920s for analysis and comparison purposes, even though the actual S&P500 index only started in 1954.

Should not be a problem for Dimensional to re-create out-of-sample performance using their factor-based indexing (in fact they have already done so), or for Stashaway to use their Economic Regime Asset Allocation going back half a century.

Things like exchange rates, trading commissions etc over the last 50 years can be estimated to quite an accurate degree.

People want to see whether performance has been consistent through different economic conditions e.g. hyperinflation, deflation, global recessions, booms, wars etc. It may be that certain economic periods suit certain investment strategies better --- of course that becomes market timing liao. LOL!

Kyith

Saturday 4th of May 2019

Hi Sinkie. We cannot backtest so much because the data the most recent is only till 2000 for some. 17 years of data you can only conclude so much.

momo

Thursday 2nd of May 2019

Hi, thanks for the great article once again.

Me thinks fees need to be same as or better than Autowealth (0.50% + USD18) to be attractive.

Kyith

Thursday 2nd of May 2019

Hi momo, i think they have to show their factors.

Vladi

Thursday 2nd of May 2019

Why is there a custodian (as an investor will my name not appear in the unit holders registry)? How safe is iFast as custodian and what are the implications if iFast goes bankrupt? How are the assets segregated?

Kyith

Thursday 2nd of May 2019

Hi Valdi, all investors' money are protected and held in trusts' account under our custodian's iFAST Financial Pte Ltd - Client Trust, which are subjected to MAS Regulations. In the unlikely event that iFAST ceases operations, your investment holdings held under custody with iFAST will not be affected as they will either be returned to the investors or transferred to another agent of your choice. iFAST has the responsibility to ensure that all liabilities and obligations to all clients have been fully discharged or provided for, and that proper arrangements have been put in place.