After the large DFA article last week, I do not really feel like writing a lot of stuff. There is probably a lot of other stuff I need to catch up upon then to do one humongous article every week.

So this week one is a little breather. It is some numbers that I ran some time ago.

I think I decide to bring it out.

There is emerging trend of experts teaching folks to build wealth with the aid of leverage. Leverage means, using other people’s money, in a lot case the banks money, to aid you in building your asset base.

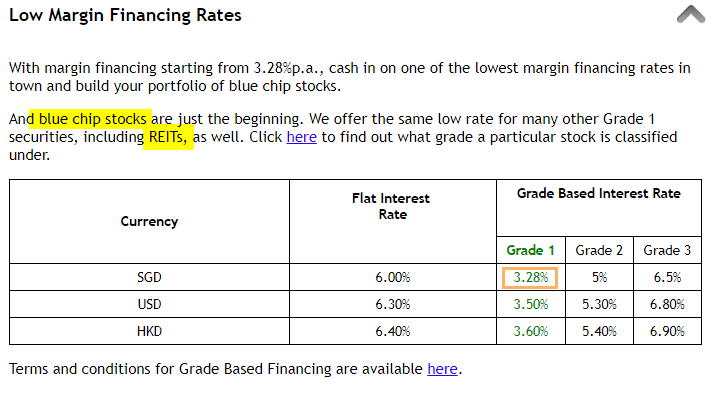

You have folks like Kim Eng who is able to give to loan you currently a 3.28% interest rate loan on your shares. This enables you to buy shares more than you can afford to and speculate on them. When you earn as you sell off the shares, you earn a lot more. Conversely, if you lose as you sell off the shares, you lose a lot more.

Now, the idea for a lot of people is not to do leverage irresponsibly. We all want to do the sensible thing, but to make use of what is available to us so that we can accelerate our wealth building.

So basically, rather conservative wealth builders wish to use leverage to step up and build their wealth. It makes me wonder how conservative we are.

Here is the Setup

We are going to invest in good blue chip stocks and Real Estate Investment Trusts (REITs).

And we are going to choose to invest in 1, or more of these, to form a portfolio that gives us a 7.5% per year compounded rate of return (hypothetically). If you want to take a look at whether its achievable, you can take a reference on the dividend yield that you can get on my Dividend Stock Tracker. Those are dividend yields, and do not show the future compounded growth rate. The growth rate can be +2 to 5% or -2 to 5%, depending on which you choose. Not all stocks are appreciating over time.

Let’s say we make use of Kim Eng’s margin financing which enables us to invest in selected stocks and REITs at a rate of 3.28% (this rate used to be 2.88%. When the global interest rate moved up, it also gets shifted up. This gives you an idea that these rates do not stay stagnant).

According to the strategy, we want to use leverage to build up our financial assets.

However, we do not want leverage to kill us. So at some point, we will pay back the debt.

The strategy is touted to be able to let you build up your asset base. So it is suitable for those folks in the initial years of wealth building.

Every year you contribute $2,000/mth or $24,000/yr from your disposable income to this leverage portfolio. That is $24,000/yr of your own money.

On top of this, through Kim Eng’s financing, they lend you $24,000 more to purchase more assets in your leverage portfolio.

There is an interest cost on this $24,000. As you build up your leverage/debt/liabilities/margin, your interest cost increases.

At some point, instead of using that $24,000/year to buy more stocks in this leverage portfolio, you use this $24,000/yr to pay down the leverage.

So the idea is

- Use your own capital + leverage to build up assets

- Use your own capital to deleverage on debt/liabilities/margin

What you will end up with at the end is an unleveraged portfolio, or one that is entirely your own equity.

The total capital you put into the portfolio in both leverage and unleverage is the same.

Building Wealth for 15 Years without Leverage

I think 15 years is a good time frame.

If you are in a good job and you can put away $2,000/mth at 26 years old, 15 years will take you to 41 years old. A relatively young age.

We first take a look at the numbers without using leverage.

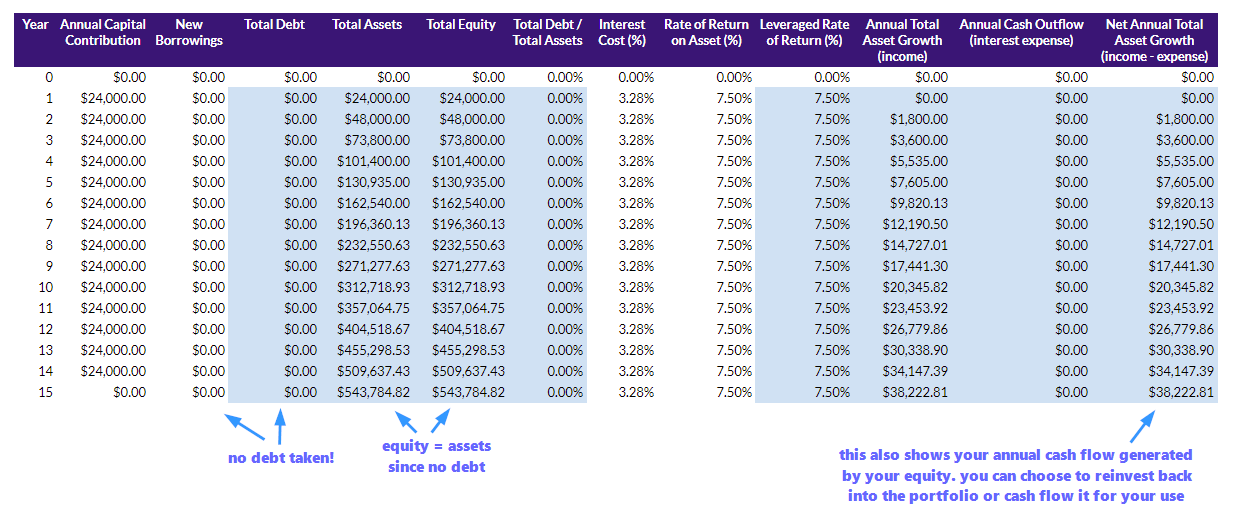

** Click to see larger table **

The table above shows the asset, debt and equity change over 15 years. It also shows us the net annual total asset growth over the 15 years.

We have probably contributed $24,000 a year for 14 years. Our assets grow from $0 to $543,784 in year 15.

Any return we have, we reinvest into the portfolio. So for example you can see the net annual total asset growth to be $1,800.

We can cash flow this and spend this in our daily expenses. But we do not do that, we reinvest back into the portfolio to grow it.

Since there is no debt, total assets – $0 debt = total equity. So Assets = Equity.

Also since there is no debt, there is no cash outflow as interest expense.

15 years and you can build up without leverage and get $3,185/mth or $38,222/year is pretty good!

Of course this is hypothetical that you earn such a consistent 7.5% on your total assets. In reality, your returns goes up and down. If you see a fund that gives you 7.5%, 7.5%, 7.5%, 7.5%… run from it. Most likely it is a scam.

Building Wealth for 15 Years with Leverage then Deleveraging in the 7th Year

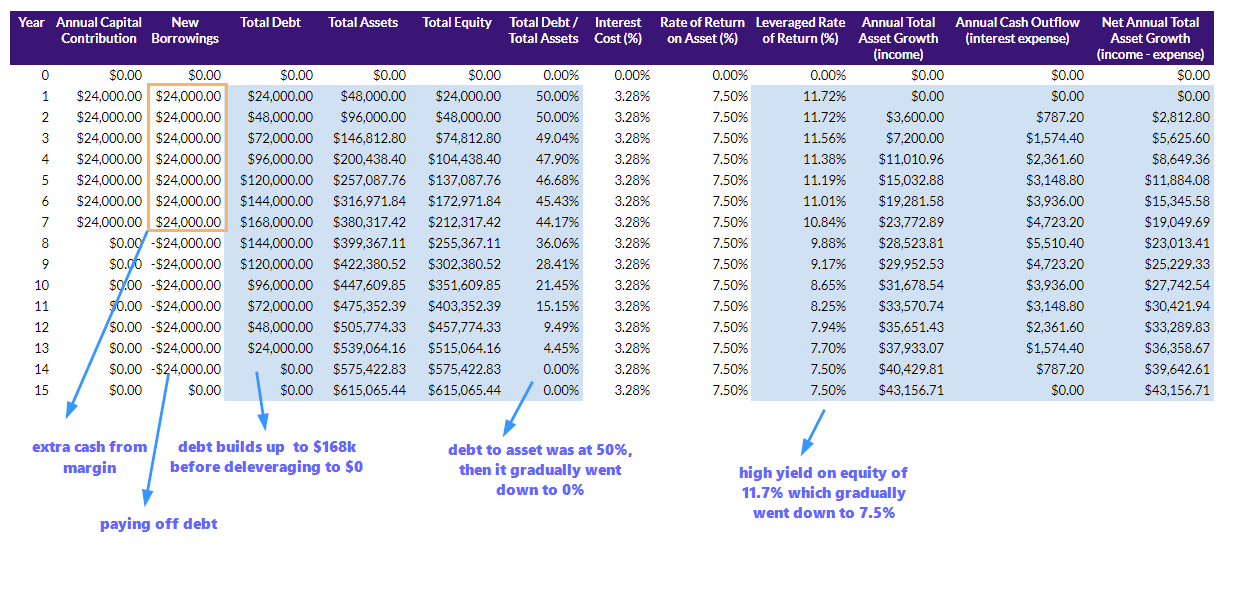

Now let us juice up the portfolio by taking on 100% more assets using margin.

Then at the 8th year, we start using our $24,000/yr to pay off the margin. At the end, we should have zero debt at the end.

** Click to see Larger Table **

I have tried to put some explanation on the data so hope that helps. We spend 7 years using leverage to build up an asset from $0 to $380k. Then the asset grow on its own with the net annual total asset growth to $615k in the 15th year.

From year 8, we use our $24,000/yr to pay down the debt.

The total equity at the end is $615k. This compares to $543k without leverage. (13.2% more)

The potential annual cash flow you could generate at the end with leverage is $43,156. This compares to $38,222 without leverage. (12.9% more)

So using this strategy, we reached our objectives 2 year in advance. Not sure about you, but that does not look like something real big.

Unless I really hate my job.

Now let us compare the total equity growth side by side.

Somewhere after the 6th year the equity of the leverage portfolio starts deviating from the unleverage one.

The chart above shows the cash flow or the net annual asset growth increase over time. Notice the great boost of building up more assets for the first 7 years giving the leverage portfolio a $19k/yr cash flow versus $12k if its unleveraged.

The chart above shows the cash flow or the net annual asset growth increase over time. Notice the great boost of building up more assets for the first 7 years giving the leverage portfolio a $19k/yr cash flow versus $12k if its unleveraged.

Then as no more assets are added, the pace of the growth slowed down. The unleveraged portfolio maintain its pace and eventually came close to catching up with the leverage portfolio.

Both your capital outlay is the same at $336,000.

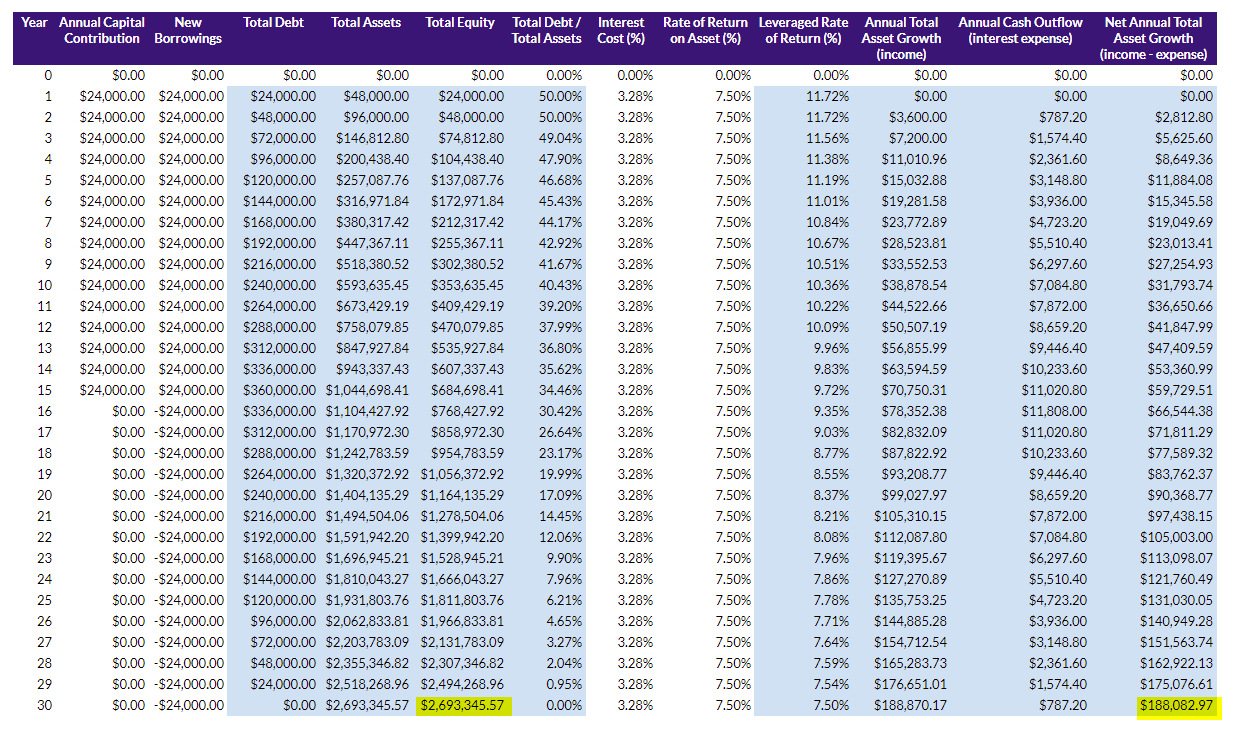

Building Wealth for 30 Years

I suspect that if we do it over a longer period, the leverage portfolio will show its quality.

So instead of 15 years, let us do it for 30 years. Instead of paying off at year 7 we start paying off at year 16.

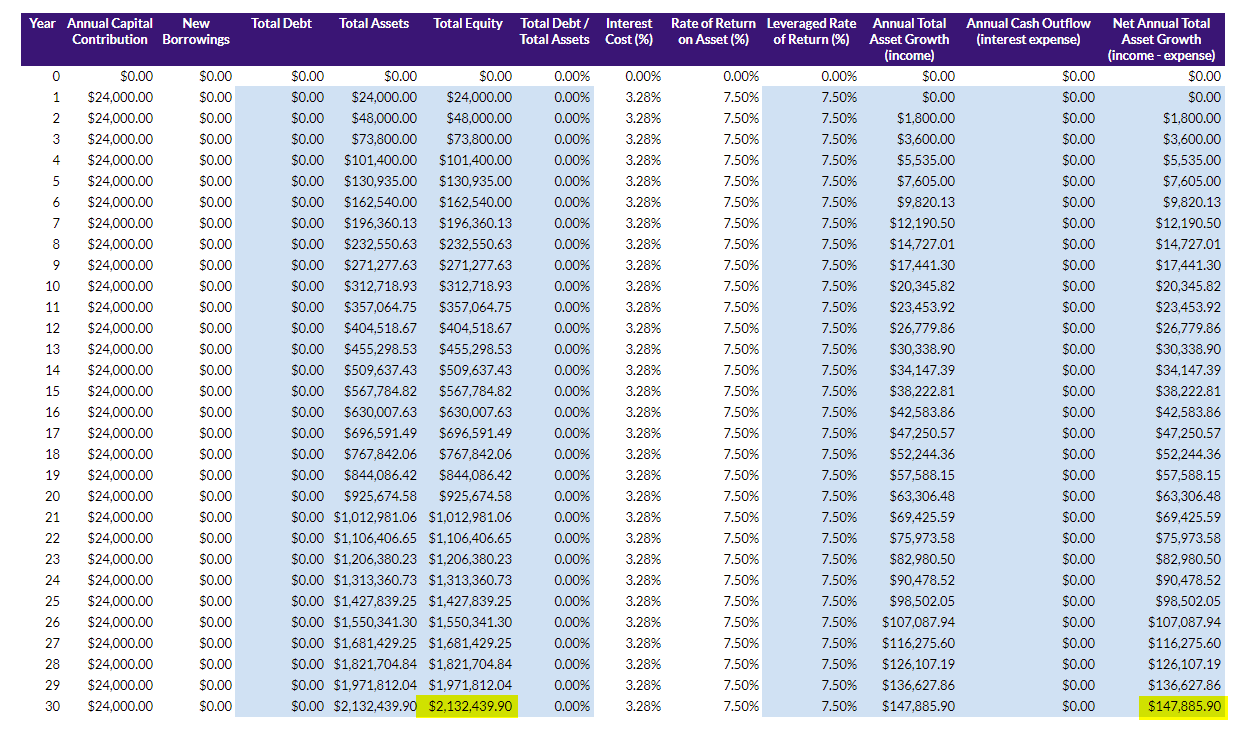

The following is the result of the 30-year unleveraged portfolio:

** 30 year unleveraged portfolio. Click to see larger image **

And the following is the result of 30-year leveraged portfolio:

** Leveraged Portfolio. Click to see larger image **

The leveraged portfolio builds $561,000 more than the unleveraged portfolio (26% more).

The leveraged portfolio eventually gives $40,000 more in annual cash flow. (27% more).

So we can see that as the duration increase, the leverage factor allows you to build more wealth and provide more cash flow (26% more versus 13% more when the duration is 15 years)

How Sequence of Returns affect the 15 Year Leverage Strategy

As I have said, your returns do not go 7.5%, 7.5%, 7.5%, 7.5%, 7.5%…….

In reality they go up and down if we are talking about total return. So this 7.5% for REITs can be the yield, but we can always look at it as a total return.

This means that you invest in a portfolio of REIT that gives you an average of 5.5% yield and a 2% compounded growth for a total return of 7.5% per year.

Now lets add a bit of sequence of return volatility into the picture.

I explained more about how a negative sequence of return can affect your retirement.

Basically, your returns over 15 year, 30 year can be of different sequence, and they affect your portfolio based on your objectives.

In the table above, I created 2 set of sequence. The first set is one where we have more negative returns first, follow by positive. The second one is more positive then negative.

If you look at the end result, both provide a 15 year compounded average rate of return of 7.5%.

The first sequence is bad for retiree. It is why I went through so much writing on retirement. To hedge this risk. However, this negative first follow by positive sequence is good for the wealth accumulator!

You get to accumulate more units when you are young. When you have more units, then when the bull market come later on, your wealth will grow.

For the leverage portfolio, I would expect this sequence to be favorable.

The second sequence, is good for the retiree but bad for the wealth accumulators.

So you can see the irony: If you have accumulate well and ready for retirement, you might be in the worst position as the negative sequence is coming. On the flip side, if you have struggle to accumulate for retirement due to poor returns, but you manage to get the amount you need, your retirement might be much smoother!

The assumption here is that market move in cycles.

How the Sequence of Returns affect an Unleveraged Portfolio

So first, lets see whether the fact is really a fact:

- The total equity build up at the end of 15 years for a uniformed 7.5%/yr return: $543,784

- The total equity build up for negative first then positive sequence: $759,390

- The total equity build up for a positive first then negative sequence: $487,547

So what I said previously checks out. If you are accumulating, it is better to have more negative years and then positive years.

How the Sequence of Returns affect a Leverage Portfolio

Now let us take a look when we applied leverage to it.

- The total equity build up at the end of 15 years for a uniformed 7.5%/yr return: $615,065

- The total equity build up for negative first then positive sequence: $913,906

- The total equity build up for a positive first then negative sequence: $601,602

Seems the dangers of leverage did not kill the portfolio. The negative first then positive sequence built $300,000 more wealth. Compared to the unleveraged portfolio which is $210,000 more only.

The positive then negative sequence was weaker but not by much.

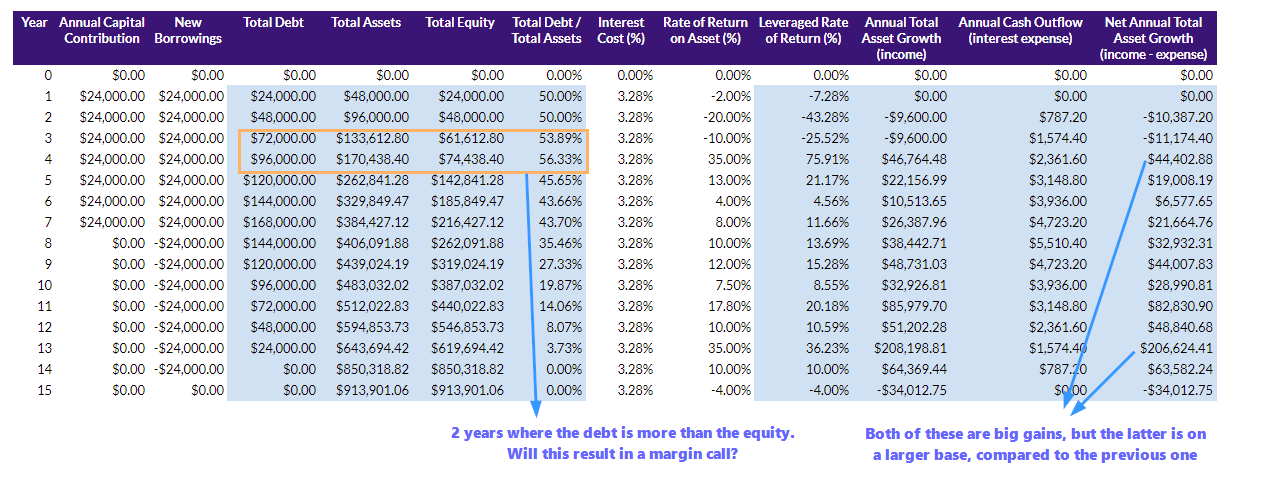

Now let us take a look at the portfolio debt to asset to see whether, at any point the portfolio is in danger.

First let us examine the negative first then positive sequence:

** Negative than Positive Returns. Click to see larger table **

I think this debt pay off thing might be working out. However, notice that when the -20% and -10% came in the debt to asset went above 50%. The debt is more than the equity.

Now I wonder whether if some of the stocks went down more on an individual basis, it will result in a margin call event. In those events, either you top up the equity to restore back to a maintenance margin ratio, or the broker force sell your assets.

Selling off at a low price. That might set your wealth building back for some time.

I think whether this becomes a grave event or not depends on the amount of capital contribution.

In those two years, although the net annual total asset growth was -10k and -11k respectively, the capital contribution and new investments dwarf that amount.

Your asset base have not gotten large enough.

It will take a few years for the new capital contribution to make up for those losses.

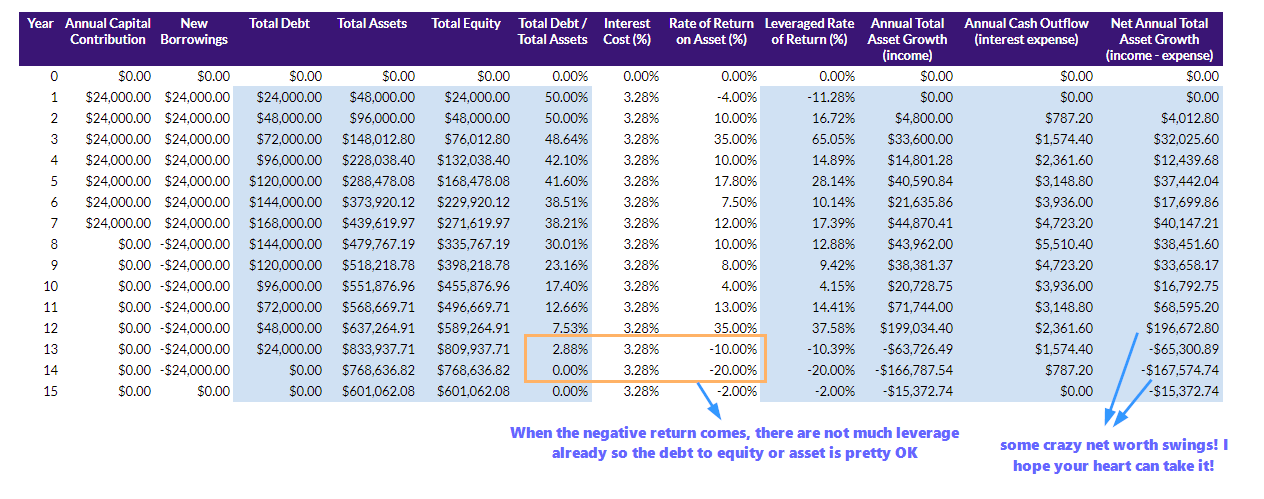

Let us examine the positive first then negative sequence:

** Positive than Negative Returns. Click to see larger table **

Leverage in this sequence did not kill because by the time the -10% and -20% returns come in, the amount of debt left is only $24,000 compared to an asset size of $833,937.

You just faced the prospect of -$230,000 reduction in your equity base.

Depressing yes, but it does not kill you.

If you think about it, this deleveraging is pretty similar to how you move more of your portfolio to bonds as you approach retirement (read How Traditional Portfolio Allocation Strategies Can Alleviate Large Market Plunge Fears).

Instead of moving to bonds, in the case of leverage portfolio, the debt is being reduced so that as you approach the twilight of your wealth accumulation, your credit risk is reduced.

Notice also that since this is an all equity portfolio, and as you approach retirement for example, a -10% and -20% return would shave a large part of your portfolio.

This investor took care of the credit default risk, but didn’t take care of the portfolio and retirement risk.

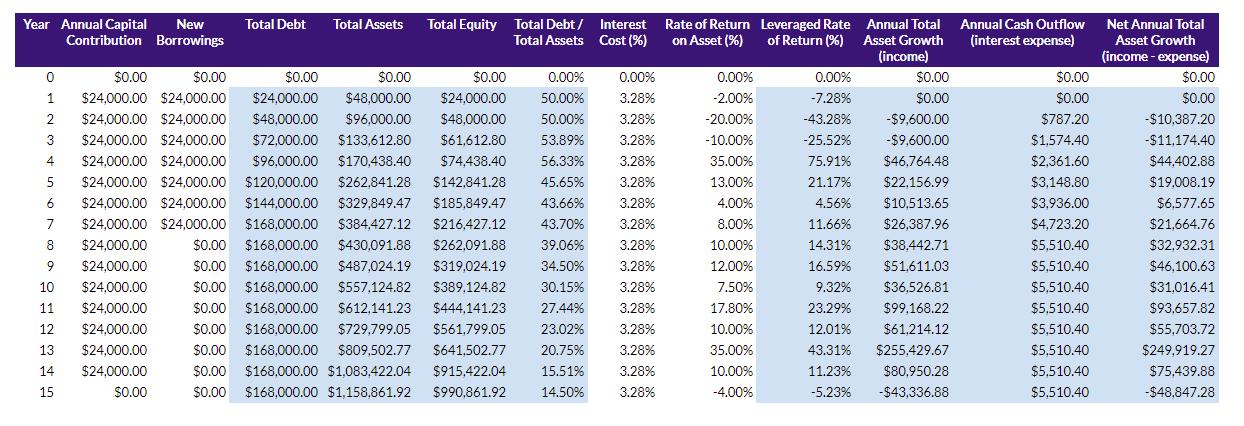

What if we didn’t Deleverage, but also don’t Leverage too Much?

Now since I went down this rabbit hole (and fxxk I wasn’t suppose to write so much!), why not build on the last sequence of return experiment and see if we do not deleverage?

The first table shows the positive to negative sequence. Notice that from year 8 to 14, the investor did not deleverage the portfolio. She adds to the assets instead.

The first table shows the positive to negative sequence. Notice that from year 8 to 14, the investor did not deleverage the portfolio. She adds to the assets instead.

Observe that the total debt to asset gets a nice bounce from 17.51% to 22.39% from 14 to 15th year. That is a huge increase.

However, because this happened at the end of the wealth accumulation stage, and that the assets have accumulated far more than the debt, that even with the huge increase, it is still manageable.

For the negative to positive sequence, once you get past the tough year 3 to 4, the portfolio naturally deleverage from 50% to 14.5%.

This is probably what naturally happen to some REITs:

- They took on debt, but they never deleverage

- They just refinance the debt over time

- The assets appreciate in value over time

- The debt remains the same value, if the rental income can cover the interest payment, and the banks are willing to let them refinance

Let us compare the return if we deleverage versus if we do not:

- deleverage versus don’t (positive to negative sequence): $601,602 vs $582,414

- deleverage versus don’t (negative to positive sequence): $913,901 vs $990,861

Not so much difference. Just for one you are free from debt one you are not.

Summary

This article turned out longer than expected. I cannot write anymore.

Should you leverage up? Is there an advantage to doing this? Are the trainers trying to sell you a pipe dream?

Here are some of my conclusions:

- If you do not understand what I have written here, it means that you should not leverage. That does not mean that if you understand, you should always leverage

- The guys came up with a strategy, and you should understand that different parts of the strategy try to make this a success. Don’t go implementing this just because you understand part of it and do not understand other part of it.

- Leverage does speed up your accumulation of wealth assets, but the level of speed up depends on a few factors, notably how long you are letting the assets compound, the rate of return of the assets

- For those who are thinking of gaining early financial independence, the advantage might not amount to much. Certainly much less than anticipated

- Whether it is a positive to negative sequence, or a negative to positive sequence, leverage mathematically enhance the returns

- Notice that what made this strategy work was the consistent capital injection into the portfolio. The capital injection is so much when the portfolio is small such that even if there is a margin call event, the capital injection saves it. If you do it in lump sum, your mileage may vary. If you lose your job during a margin call event (when times are bad, these 2 events come together!), you can be really fxxked

- You could choose to be sensible and let the portfolio naturally deleverage by not taking on too much debt and letting the assets appreciate

- While negative to positive sequence is the most conducive to wealth accumulation, depending on your leverage, and the individual stock risk, you might face some nasty margin call

- Interest rate do not stay stagnant. Your rate of return is also uncertain. By leveraging you are taking on more complexity. The advantage might not be too much and you end up walking on a tight rope. Hope you don’t end up being strangled by the rope

- We are doing the experiment on a portfolio level. However, there are some stocks that will get impaired pretty badly. So much so that they do not come back. Their business or structure have been drastically altered in a negative way that they just do not come back. Active stock investing is a whole different ball game all together

- There are alternatives to this: Get better in your stock investing! You might not need to bother with things like this. I always find that leveraging up are people attempting to invest with something conservative, but putting on more risk on something conservative. It depends on which poison you prefer.

- Again, this strategy is based on a consistent capital injection. If it is a large lump sum investing, your mileage may vary!

Let me know if some of my numbers seemed weird. I do make mistakes here and there. I realize in this research, some numbers lead me to believe that an unleveraged portfolio generates greater equity than a leverage one. Which mathematically do not make sense. So I am rather lucky to find my own error.

Do Like Me on Facebook. I share some tidbits that is not on the blog post there often.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Thinknotleft

Thursday 11th of June 2020

Hi

Was thinking about leveraged REIT strategy and I saw your article.

If do not pay down the leverage, the strategy looks like picking nickels in front of steamroller and one may not be aware when the steamroller will move (e.g. when stock crisis hit)

If pay down the leverage, it seems not worth the trouble to leverage.

For young person in middle class hh, if he wants to leverage, it could be safer to borrow from his parents at X% and return the sum some years later. He will not run into margin call during market downturn.

Kyith

Thursday 11th of June 2020

Hi Thinknotleft, I think this crisis shows that a tail event can occur not out of the question. However, I was supposed to read this book called lifestyle investing which explains the rational of leveraging early and then deleveraging. The idea behind is that at the start, you have a long time horizon but no capital. so leveraging would allow you to have a larger portfolio. You are making use of the time diversification aspect of investing to spread out your risk. when you are young, you can top up the margin calls with salary because the sum is still small.

Dylan Smith

Thursday 7th of May 2020

Hi Kyith,

Wanted to reply you but seems that the previous comment wasn't published. Didn't realise that some banks can remove stocks from margin accounts. How much lead time do they typically give before doing such stuff, and where can I read up more about applying safe leverage to my portfolio? Will you recommend applying it to pure growth stocks? Cheers!

Kyith

Saturday 9th of May 2020

Hi Dylan Smith, they remove it on the fly. So you have no reaction time. I think for growth stocks, the volatility tends to be higher. So while they do go up over time, in the short term we do not know what will happen. In this recent period you have seen some tech stocks go up and down 50%, and these are not small companies.

Dylan

Wednesday 6th of May 2020

Hi there, your article is super informative! Would be lovely if you could have a follow-up article on whether the current environment is a good time to apply leverage since interest rates are at all-time low, and it seems that REITs have stabilised too.

Will be good if there is a checklist we can follow to know when to leverage and when to de-leverage.

Kyith

Thursday 7th of May 2020

Hi Dylan,

I think I would have to revisit if that leverage factor actually kills the portfolio in what we have witnessed. A lot of the listed equities went to a 50% fall. That would necessitate a top-up. A lot of these are math, but the other aspect is whether you could find a lender that lends you at a good rate, and maintains it. A few firms removed certain stocks from marginable accounts. This is the equivalent of a margin call event.

My take is that if you are young, and you are building up your wealth, and that you have a bond-like job, you can do something like this. If you are older, don't mess with this too much. When you are young your income can top up and replenish your capital. When you are older you cannot do that well.

Adnan

Saturday 23rd of November 2019

Great article and really informative. Thanks for taking the time to explain in such clear detail.

Just wondering how it would differ if instead of a continuous investment over the years, an initial lump sum was used instead.

😊

Kyith

Saturday 23rd of November 2019

Hi Adnan, good question. There will also be a question of whether we deleverage at all or let it appreciate. I will see if i have the time to carry that testing out.

Sinkie

Monday 22nd of April 2019

A lot of nuances need to be applied. For example, it doesn't need to be an all or nothing --- even for the trainers, I suspect half or more of their overall portfolio is not leveraged. And even for the leveraged portion, it is likely not 1-for-1 leverage but something more of $0.50 margin for every $1 of own equity. With a 100% leverage, even bluest of blue chip REITs & bank stocks will face margin calls during recessions. More volatile counters will also have lower leverage applied, or not used for leverage at all.

Since many people focus on using leverage to juice yields, they naturally apply (or want to apply) leverage on REITs. You need to pay back the margin interest regularly, and dividends are much more dependable over the short term than counting on capital gains to offset the interest payments. However for REITs will need to focus on gearing, not just yield (just like normal stocks) --- and will need to be prepared to take up rights issues for both own equity as well as margined portion. Like you said, usually bad stuff all happens together --- fast & steep price declines, large rights issues, need to do large cash injections, job instability, anxiety over adequacy of emergency funds etc. To top it off, your bank may decide to move your counters to lower grade with higher financing cost.

The economic cycle also plays a part in how aggressive a leverage you want to employ. Starting near the beginning of a low-interest part of the cycle gives you not just cheap financing, but also a long runway to build up capital gains as additional buffers for your margined portion. During later stages of the cycle, likely will want to reduce leverage --- but that's when stock prices really on rocket fuel & temptation is there to push the boundaries.

Kh

Saturday 7th of December 2019

Hi sinkie,someone with the same nick left similar comments on the DW website for the early retirement course, so I am assuming it’s the same person here. What is your take on that masterclass and the limitations of the 10 year back test window for testing the strategy performance?