You might have friends who keep complaining to you that it can be such a challenge saving money.

These are the friends who frustrate you the most because you know the solution to their problem is very simple and implementable, yet their habits and psychology is a huge impediment for them to successful saving.

I was introduced to this new digital account called Hugo.

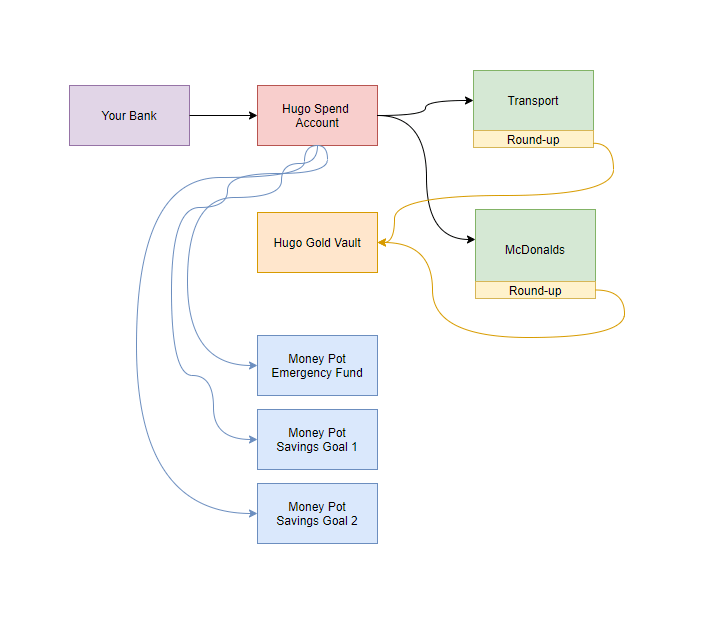

Hugo will systematically make you save by putting some money during many of your spending transactions into a gold vault.

Instead of just telling you about it, I decide to keep using Hugo for one month.

Here is my experience with Hugo.

My Experience with Hugo Wealthcare

One of the main goals of Hugo is to help us develop healthy saving and spending habits.

I will talk about the former later but let us talk about the latter.

Here is how Hugo work initially:

- Download the Hugo application from the Apple App Store or Google Play Store.

- Once you signed up for Hugo, they will give you an account number. With this account number, you can fund your Hugo Account.

- You can go to your bank’s internet banking platform and create a new transfer payee with this new account and name the account Kyith Hugo.

- Do an internet FAST transfer or in my case a local transfer to my Hugo account number.

- You should be able to see your money in your Hugo account after a few minutes.

Spend your money with your Hugo Visa Debit card

Once you set up the account, you can request Hugo to send you a VISA debit card.

The Hugo card is numberless.

There is an advantage to the card being numberless. If you lose your card, it greatly prevents the person who have your card from using your Hugo debt card to make internet transactions.

If you need the number for an online transaction, you can see the number on your mobile application (which you can download to manage your account).

This VISA debit card currently does not give you cash back or miles, but you can spend on a lot of things.

I use it for my MRT and bus ride with SimplyGo.

I use it to do Shopee purchases and when I eat at restaurants.

If you wish to set up recurring payments with it, I think you should be able to, even though I did not try that.

When you spend, Hugo will “round-up” your transaction.

Say for example I spend $3.32 on two train rides with Simply Go. Hugo will round up the $0.68 that would make $3.32 into a whole number.

In another case, if I ate Fish and Chips at Essien @ Pinnacle at Duxton and it cost $12, Hugo will have nothing to round up.

A sandwich at Belle Ville cost $6.40 and Hugo will round up the $0.60.

Now, this round-up is not a payment from Hugo. This is money from your own spending account that is set aside for investments.

As I continue to spend, I notice that my round-ups will start adding up.

Round-ups will be Channelled to Gold Savings

All the round-ups that you have accumulated periodically can be automatically configured to be put in Gold Vault.

Your account will automatically purchase different grams of gold.

This gold is stored in an accredited LBMA (London Bullion Market Association) vault. The gold is insured by Lloyds of London.

This means that while you spend from Hugo, Hugo will passively help you channel some of your money into a different form of saving.

In my short one month, I have put away $6.28 worth of gold.

Hugo earns through a nominal fee of 0.5% of each transaction (but this is waived until 28th November 2021). In contrast, most local channels may charge a 3-3.5% one-time transaction cost.

Create Different Money Pots to Compartmentalize Your Money

If you look at the first graphic, you would notice that Hugo allows you to do something else other than spend.

You can separate your money into different money pots.

What is the benefit of doing that?

This is a way for you to practice a kind of budgeting called envelope budgeting.

For envelope budgeting, you will create various virtual envelopes and name them according to what you wish to achieve. For example, one will be for your vacation, one would be for your emergency savings fund.

You will have a certain amount that you would like to build up towards.

With Hugo, the money that you have transferred from your bank account to Hugo can be “locked up” in these Money Pots.

You would not be able to spend them.

If you need the money, however, you can withdraw from these pots so that you can have assessed to the money.

Hugo, like many banks before them tries to do this but there are a few things each of them failed to implement well:

- In Hugo’s case, you can put away $5,000 towards a $12,000 goal, but you are not earning anything on this $5,000.

- If you hit the goal, what you could do is that you can close the money pot. The money will spill over to your main account and you can use it.

- To spend from each pot, you would have to withdraw from each pot, then spend. I hope we have the time to do that often. Like many implementations, we cannot choose which pot to spend from.

These are the areas Hugo can improve their money pots.

In fact, I can think of a few improvements to their platform. Let me go through them.

Reports on My Spending Pattern

I went through the trouble of using Hugo’s debit card for practically all the transactions that I can think of.

Hugo did a relatively good job of tagging each transaction. In each transaction, it allows you to add a note or upload a receipt.

You can also see the round-up that is taken from your account.

If I bought a sandwich from Belle Ville at 100am, it gets tagged under Bars & Eating out.

Some transactions were wrongly tagged. I had fish and chips at Essien and that was tagged as Entertainment.

What I understand from the Hugo team is that a third-party institution is helping them with the tagging. It is possible that the fish and chip stall incorrectly identify them as entertainment and thus we have this situation.

If a transaction is tagged wrongly, currently there is no way for me to amend that.

If you wish to change my spending habit, I would think it is important for me to know something interesting about my spending pattern.

Currently, there are no reports for me to make sense of what I am spending upon.

Reporting is a good feature if we are trying to change our spending habits.

If someone is serious about changing, I could just ask them to just use a credit card for all their transactions.

The downside of a credit card is that the statement shows the transactions but do not provide good insights into what you spend upon.

This is an opportunity for a fintech platform to help if they are serious about helping us change our financial habits.

The good news is that the team at Hugo will be looking to see what kind of analytics that they can provide to the users. I would likely update more when the phase 2 features happen.

More Incentives to Use the Hugo Debit Card

The alternative to using a Hugo card is:

- Using cash

- Using a credit card to earn miles

- Using a credit card to earn cashback

Subscribing to Hugo’s ecosystem allows me to save money in gold but that is on top of my spending.

I didn’t monetize my spending in this Hugo ecosystem so this would be an area that they can do better to incentivize us to choose them over the typical credit card.

The issue with most promotions is that the promotions only attract a segment of the people. Credit card companies need to have a range of promotions to be attractive to a wider range of clients.

The Hugo team definitely would like to collaborate with other partners, but they have their work cut out trying to find deals that looked useful to the consumers.

The Hugo Debit Card can be rather efficient in terms of fee:

- Usually, there will be two sets of forex fees if you use a credit card, one charged by Visa/Mastercard and another by the bank. You will be only charged the Visa forex fee and there won’t be any more forex fees.

- There are no annual fees.

- There is no fall below fees.

- There are no admin fees.

Why Save in Gold?

As an old school guy, I can make a justification for why we should hold gold.

Gold does not produce cash flow and does not have many industrial uses.

Gold is appealing as jewellery. For the longest time, gold is also a store of value and small enough as a medium of exchange.

Its value depends on how much its competitors (fiat money, digital currency, other alternatives) depreciate against it.

Gold as a hard asset is also similar to things like high-quality artworks and watches. Some investors have an appreciation for it and at the same time, it fulfils the value retention aspect.

Nowadays, I wonder how many of us would feel pleasant, or motivated if we just remember we held a small stash of gold.

I think perhaps if you replace gold with Ethereum, and stake it in a liquidity pool and earn 15% APR, people will have been more interested because they could visualize not looking at it for 1 year and it snowballed to a crazy sum of money.

But I think over time, Hugo probably need to state why gold is a go-to place for the target niche to put their money in.

By choosing gold, they are choosing gold over strategies based on other asset classes.

To be clear, it is likely they are bringing other stuff onto their platform and gold might be easier for them to onboard at this point.

Who is most suitable to use Hugo?

I had first came across a similar concept to Hugo with Acorns in the United States.

It can be difficult for us to determine how much to save because firstly we are bad with money stuff and our expenses are almost as much as our income.

Systems like Hugo and Acorns systematically made us save with less friction.

This means that Hugo works well if you have always been struggling with the saving aspect of your life.

For whatever reason you just could not get it or that the level of uncertainty in your expenses prevents you from creating a savings system.

Freelancers with very volatile cash flow would fit. Your friends who keep telling you “I cannot save money forever.” Would fit this.

The second group are those who believe in gold as an investment, feels paying a 0.5% transaction fee is ok, and wants to hold the investments through Hugo.

Beyond that, for most of us, there is little incentive.

The majority of the savings we will earn is based on round-ups. What would move the needle for most of us is to be intentional with our paycheck, to put away a sizable amount of our surplus from work.

Finally, parents might be interested to see if they could give their kids pocket spending through Hugo. This might be a bit challenging as the minimum age for Hugo is 18 years old.

If the age criteria are lower, I could transfer money to my kid’s Hugo and he could buy through the platform and have a way for him to save his money at the same time.

However, those young adults who are 18-year-old and above but not working yet may see the benefit of having a debit card like Hugo Debit Card.

An 18-year-old may be able to learn some adulting skills with Hugo still.

Conclusion

I do like some aspects of Hugo but if I am being honest, I would probably not get as much mileage to compare to others.

I tried to spend normally. At the end of the day, I wonder if my spending habit changed in any way as 1 month ago.

My conclusion is that my spending habits did not change.

I wasn’t restricting certain spending because there were no restrictions placed. There were no guidelines that tell me I should not spend more than the said amount.

This might be a start for Hugo to develop further.

If you are interested, do give Hugo a try today.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Jade Eswagen

Wednesday 30th of March 2022

Hi kyith, I have to be honest that for years I've been reading to learn more about investing, portfolios from one blogger to another, financial advisor to another. I've to say I've not read any article as detailed and simplified as you, and it's really a life saver for someone like me who has zero knowledge on the topic investment.Its been tough on my end with all the responsibilities I have to shoulder, that every cent is utilized monthly with nothing set aside and I just couldn't go about starting anything being too afraid of having to lose it in the end. I truly want to be financially independent, I am honestly not looking to live the luxurious life although maybe if that happens I'll be grateful but I just want to have something aside in any case of emergency.Money is always a sensitive issue and it can turn relationship even with your loved ones sour. Therefore I've always tried my hardest to not do any loan or borrow. I'll try to figure out more on the portfolio and hope I'll be able to create with interactive brokers

Jade

Kyith

Sunday 10th of April 2022

Hi Jade, erm where do you need help?