One of my friends raised something interesting during one of our lunch conversation.

She said that I should write more about millennials and divorce.

I was curious about why this topic in the first place. She revealed that more and more of the young adults around her don’t seem to be able to stay together.

I am not sure if this is a prevalent trend. I am probably at the border as the oldest millennial and most of my friends remained married. There are the odd one or two that I think (guessing) that are divorced. (If you are observing the same thing as my young friend, do let me know in the comments)

I explained to her that it will be a little weird for me to dish out any advice or recommendations when it comes to relationships and money. Usually, the problem is less about money but our internal programming and relationships.

I just came across a rather good Wall Street Journal Article on this topic and decide to do my own summary (without the flowery language) and shared it here.

What you will realize is that…. we tend to have money insecurities, but our coping mechanisms are different.

The problem is… folks that are uptight about money tends to be attracted to folks who treat themselves like their friend’s ATM machine.

My conversations with my friends make me agree with this quite a fair bit. It seems I am always talking to the spouse with the better money habits and they are telling me horrendous money stories about their spouse.

So this article may help you frame how you can look at this.

The answer may be to go for therapy.

Your relationship style has a close relationship with how you approach money.

Your stability and security with your interpersonal relationships tend to mirror your financial stability and security.

If you honestly self-reflect and dig into your current and past relationships with others, you may be able to understand your spending, saving and investing habits.

Studying Your Attachment Style

We all have a unqiue interpersonal attachment style. Your style falls somewhere in a spectrum of secure and insecure.

Typically, we are tilted towards the insecure side. The spectrum of behaviors associated with insecurity range between:

- Anxious – Like your dog that cannot get enough of you

- Avoidant – Like your cat who behaves very well without you

Anxious people tend to use money as a means to be loved and be appreciate and have people around you. Common traits would be picking up the check, give expensive gifts and regularly buy new cars and wear pricey clothes.

In short, you are like other people’s ATM machine. They also feel like the Amazon deliveries are like love arriving in a cardboard box.

Avoidant people tend to save money so that they do not have to rely on others or so that they can exert power over others. Examples would be that if you give money there are strings attached.

Avoidant people tend to develop resentment towards those who take their money. They are naturally distanced from others, and this would further distance themselves from these people.

Avoidants would also interpret investments on their own. Avoidants tend not to trust financial advisers or market sentiments.

Avoidant types may become so obsessed about not spending money that they go for cheap grade of service that end up costing them more.

Many of us will not fall into either anxious or avoidant but may have both traits. Typically, it means we are insecure enough.

I think if everyone is trying to accumulate wealth in our own ways, we are insecure and therefore these traits are bound to surface.

Studying Your Childhood and Money Stories

Your attachment style and how you are with money is determined by:

- Upbringing

- Experiences and cultural influences

You may associate your personal intimacy and money by proxy with:

- Safety

- Peril

- Protection

- Secrecy

- Control

- Prestige

- Power

- Weakness

- Virtue

- Vice

- Acceptance

- Rejection

These are established during your childhood and are hard to re-programmed. Most don’t even know they were programmed during their childhood by their experiences this way. (Think a fish doesn’t know it’s wet)

Financial flashpoints you encounter early in life about money affect your future behaviors.

Dr Brad advise us to ask ourselves expansive questions to understand the interpersonal attachments and experiences that shape our beliefs.

Dr Brad Klontz have a Money Script test to discern your personal money script by asking 33 questions. You can take it here. (Readers can see at the end of this article Kyith’s Money Scripts)

Another method is to trying and talk to money.

Depending on your personality, the money will often “sound different” to many of you. For some, the money will sound influential and for others not so much.

Money Privacy and Personal Shaming

We tend to keep our relationship with money private and not discuss this with others.

Some feel shame about how much money they have. Some feel shame about how little money they have. We will also manage money better or wose than others.

Keeping these conversations question may create money distortions that grow more powerful and potentially damaging.

Dr McCoy, a license marriage and familiy therapist as well as certified financial planner admits that at an early part of her life, she thinks money is the root of badness. If you want to be a good girl, you buy into the church’s message in giving and sacrificing.

Her internal brain looked at her brother, who is good and math, and decided there and then that math is not her thing but something his brother is good at and she should keep to what she is good at.

She had to go through therapy to re-program some of that. She also married someone overly vigilant of his money, which re-centered how she thinks about money.

Anxious and Avoidant People Tend to Attract Each Other

Opposites tend to attrach each other. Some married each other.

This tend to cause different degree of conflicts.

Financial Coach Dave Lowell helps couples get to the bottom of their mismatched, often warped money beliefs so that they are more at ease with their finances and around each other.

Here are some of the things Mr Lowell did:

- Ask each to fill up a questionnaire that asks about their past significant relationship, memorable money experiences. These experiences may be influencing them today.

- Talking about these money experience allows the spouses to understand each other’s money stories and why they do things this way

- Clients do tend to slide back in old ways when they face stress. Anxious spouse will overspend and avoidant will be obsessed about not spending when things get expensive

- The trick is to talk about why they do it, recenter and get back on track

- He recommends automation of as much of their financial lives as possible

- Automatic paycheck deductions for retirement accounts

- Money-fund transfers to accounts reserve for goals

- Designated fun money accounts

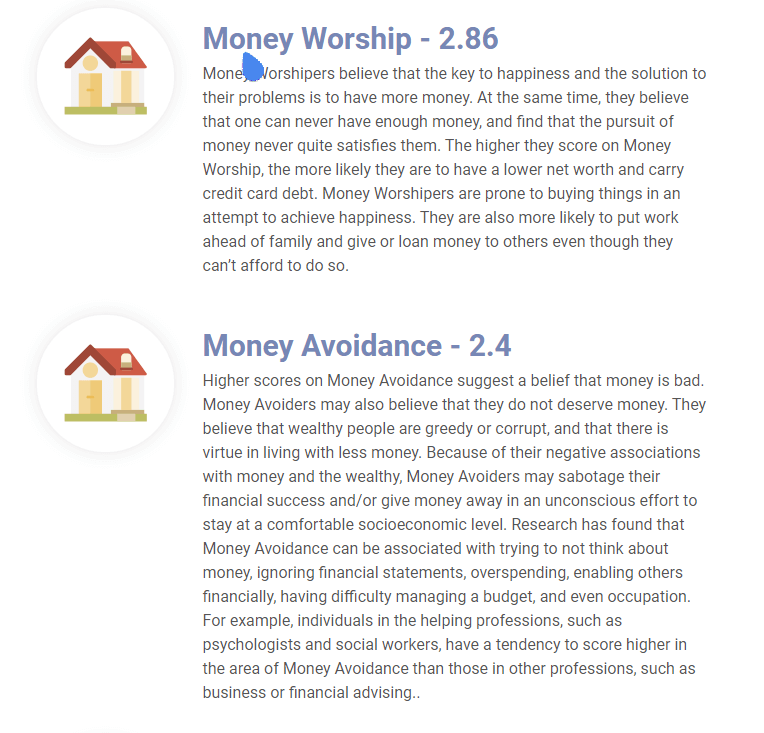

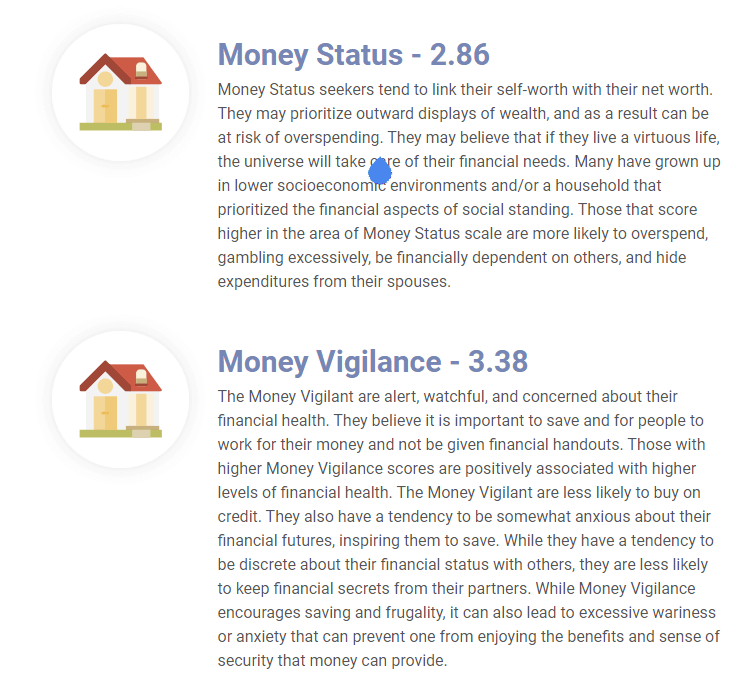

Kyith’s Money Script

I answered Dr Brad Klontz’s 33 questions to see what kind of money script I have programmed in me.

The questions are really damn simple and I believe I ended up having a lot of “disagree”

The KMSI-II has been researched extensively by Dr. Brad Klontz of Your Mental Wealth Advisors, the Financial Psychology Institute, and Creighton University. Dr. Klontz and his colleagues have found that money scripts are associated with income, net worth, financial behaviors, and other aspects of financial health. For many people, discovering and exploring their money scripts is an important step toward increasing their income, net worth, and improving their financial health. Scores on the money script scales range from 1 to 6. Higher scores indicate stronger levels of conviction in the particular category of money beliefs. It is not uncommon to have money scripts that seem at first glance to contradict each other, such as endorsing the belief that “money corrupts people” while also believing that “things would get better if I had more money.”

Scoring Key:

- Scores lower than or equal to 3: Suggest you do not exhibit the money script

- Scores between 3 and 4: Suggest you exhibit some characteristics of the money script

- Scores higher than 4: Suggest you exhibit many of the characteristics of the money script

Your results are Below:

It looks like I do not have much money scripts! Well except for being more vigilant with money.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024