19 months ago, DBS decided to revamp their higher yielding savings account offering.

I wrote about the account, and then I made this into one of the main savings account that I used.

The DBS Multiplier account was pretty refreshing when it was launched because it caters to a particular group of savers that other banks were not catering to.

On 1st of May this year, DBS decided to enhance their DBS Multiplier so that you may be able to benefit from higher interest rate and have this interest rate applied to a larger savings amount.

I took a look at the offering, and I think I will stick to the DBS Multiplier.

So let me explain to you the changes, why I decide to stick with my decision, and some of the ways that I can make use of it to help me build wealth better.

The Current DBS Multiplier

Before I carry on the explanation, you might be interested to hear my perspective of the Multiplier account 19 months ago. You can read the link above.

I think before I explain the changes it is better to refresh our memory how the Multiplier is like currently.

If we recall, the table above shows the interest that you can earned if you made different levels of transactions. If you have satisfied that particular band of transactions, and have fulfilled 1 or 2 categories of different transactions, you earn that amount of interest within that band on the first $50,000 in your DBS Multiplier Account.

If we recall, the table above shows the interest that you can earned if you made different levels of transactions. If you have satisfied that particular band of transactions, and have fulfilled 1 or 2 categories of different transactions, you earn that amount of interest within that band on the first $50,000 in your DBS Multiplier Account.

The mandatory criterion is that you must credit your salary into a DBS/POSB savings account. This does not have to be the DBS Multiplier account, it can be your savings account, multi-currency account, joint savings account with your spouse. DBS have a way to track the salary being credit to any account under your name.

There are 2 different tiers of interest rates that you could earn, and it depends on how many categories of transactions you can satisfy:

- Credit Card Spend with DBS/POSB

- Home Loan Instalments with DBS/POSB. Both contributions from CPF and cash payments for home loan instalment qualify

- Insurance with DBS/POSB. Selected new regular premium insurance policies purchased through DBS/POSB

- Investments with DBS/POSB. This includes dividends from CDP credited into your personal or joint DBS/POSB deposit accounts. New lump sum or regular savings plan (unit trust or ETFs) bought through DBS/POSB. Buy transactions made via DBS Vickers Online Trading, mTrading, DBS digibank, iWealth

This looks like any of the hurdle savings account out there in the market such as the OCBC 360, Maybank Saveup, UOB One, BOC Smartsaver, Standard Charted Bonussaver.

Except that instead of high minimum for each category, to qualify, the Multiplier allows you to aggregate ALL your transactions to see which transaction band you hit and what is the interest you can earn.

The minimum is to have $2,000 in transactions.

This sounds complicated but it is not let me go through some examples.

For example, suppose that I earned a take home pay of $1,500 and

- I spend $300 on a DBS/POSB credit card

- I bought a regular Manulife Term Insurance and paid $200 in premiums

So I satisfy

- The salary credit

- 2 categories of transactions

- The total transactions add up to $2,000, which satisfy the minimum $2,000 in transactions

According to the table, I will earn 1.80% per year in interest.

This is pretty sweet for you if you are starting out and do not earn so much. You would have failed other savings account qualifications.

If instead you spend $500 on your credit card (as an example, it is a bit irresponsible to earn $1,500 and spend $500 in credit card transactions!) and no insurance, investments or home loans, you satisfy 1 category instead of 2.

You still earn 1.55% per year in interest.

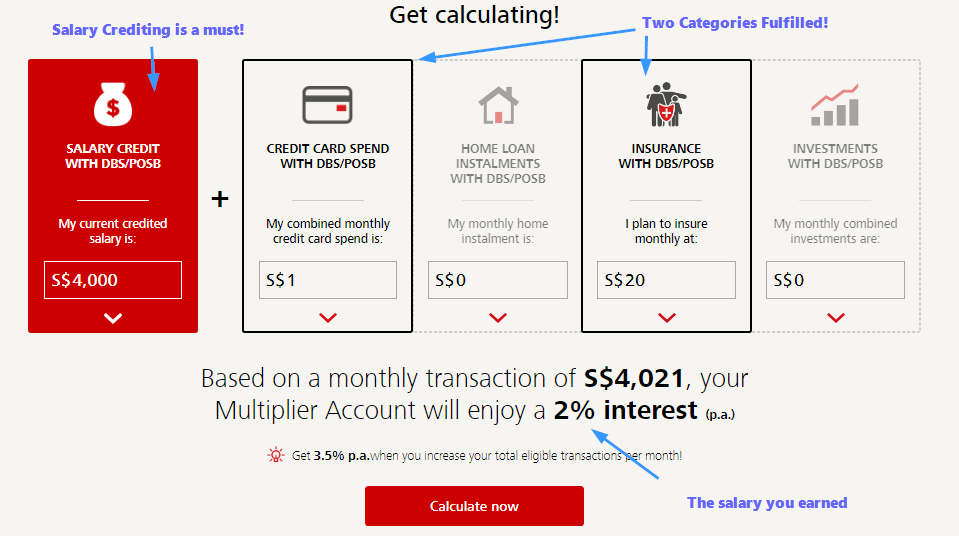

Here is an example for the graduates.

Suppose your take home pay is $4,000/mth and you spend $1 on a credit card transaction and $20 per month on an insurance product:

- You satisfy 2 transaction categories minimally

- You credit a salary

Your total transactions of $4,021 qualifies you for 2% in interest rate.

Notice that without a minimum amount for each category, unlike its competitors, you are able to qualify for the DBS Multiplier bonus interest rates. I will probably explain the advantages to me below.

Boosting the DBS Multiplier

DBS will be providing a boost to the interest you can earn on the money in your DBS Multiplier account.

Potentially, you can earn higher interest on $100,000 instead of $50,000 currently.

However, it is not so straight forward.

Let me explain.

So what I have explained in the previous section is still valid.

There are no changes there for the 2 tiers of interest rates, and transaction bands that I talked about.

DBS introduce a third tier of interest.

To satisfy this tier of interest you have to qualify one more category of transactions.

And if you manage to satisfy one more category of transactions, you earn a higher interest on another $50,000 of savings in the DBS Multiplier.

Let us go through an example.

Suppose you:

- Have $100,000 in your DBS Multiplier

- Have $4000 salary credited to another POSB savings account

- Have a $1400 DBS home loan mortgage paid via your CPF

- Purchase $5000 worth of stocks through DBS Vickers for the month

You have hit at least $2000 worth of transactions, 3 categories, and amassed $10,400 in total transactions for the month.

For this month your interest will be

- 2.2%/12 on your first $50,000 for this month

- 2.4%/12 on your next $50,000 for this month

If instead of three categories, you can only hit two categories, and amass $9000 in eligible transactions for the month, your interest for the month will be:

- 2.2%/12 on your first $50,000 for this month

So there is no penalty, you will still earn like your original multiplier.

Why I am Sticking with the DBS Multiplier

As a wealth builder, I have to balance my life and how hard my money works for me. So we are always evaluating which savings account we should use in our daily lives.

I will stick with the DBS Multiplier (unless a competitive bank comes up with a 5% yielding, low hurdle savings account!).

Let me share with you some of the reasons and my perspectives about the account.

1 Throwing down the Gauntlet if You have the Spending Ability

The original Multiplier did something really great.

And that is that it caters to those who have a lot of trouble hitting the high minimums of the various transaction categories in other banks. Due to that, if your earning and spending is low, you are left to earn a low interest of 0.05%. They changed that by enabling those who could hit $2,000/mth in transactions to earn 1.55%.

They took care of the lower bound. And they have kept that lower bound.

With these changes they are challenging those who can bank with DBS more :

If you have the ability to fulfil one more category in transactions, we are going to reward you with more! Higher interest on another $50,000.

But if you failed this challenge, they are not going to penalize you.

2 A Challenge with a Worthwhile Reward

And for me if you fulfil the additional category it is worth it.

By satisfying just one more category, and with no minimum category transactions, you get potentially $1000 to $1900/yr more in interest.

For those who have quite a bit of cash lying around, you may be struggling to fulfil 2 different hurdle savings accounts like the DBS Multiplier. Most would need to have salary credit and credit card transactions.

How does one have so much salary and spend so much money?

If you have a need for home loan, unit trust or insurance needs, it is a worthwhile hurdle to create another high yield savings account.

3 The Only Savings Account that Blends with Your Stock and Bond Investing

As an investor, there are no other savings account that have stock investing as a transaction category that leads to higher interest rate.

Except the DBS Multiplier.

And this suits me a lot.

- When I purchase local or foreign stocks using DBS Vickers as my broker, this counts as an eligible transaction (sell, contra and electronic payment of shares do not count)

- When dividends are paid by the stock and credited into my DBS savings account via CDP, this counts as an eligible transaction

As a stock investor who has dividends coming in, together with a minimum credit card transaction, I can satisfy 2 categories to earn the Tier 2 interest.

Now we know that dividends are not paid out in all months, so you might be wondering how do we consistently fulfil the investment transaction category.

You could

- For those months where there are no dividends, you buy a stock. This might be a bit tough and not really advisable for everyone as the potential losses might be heavier than the interest gain

- Implement the Singapore Savings Bond ladder. More on this later

- Buy a bunch of dividend stocks that provide dividends every month. More on this later

#3 is doable but I would advise against forcing yourself just for the sake of higher interest. One dividend investor, Paul Low, managed to invest in such a way, he has dividends payable to him every month.

For most of you, #2 looks to be the most applicable.

In 2015, MAS decide to package our AAA rated Singapore Government Bonds into a Singapore Savings Bond.

This bond

- Is AAA rated and very hard to default

- The way its packaged, if you sell it any time, you will get back your principal, and any accrual interest that have not been paid out. So you do not make loses on your principal

- Pays out interest every 6 months. The pay-out counts as dividends from your CDP into your DBS savings account

- The minimum amount you can apply is $500. Note that for each buy and sell of the Singapore Savings Bond, there is a $2 admin charge

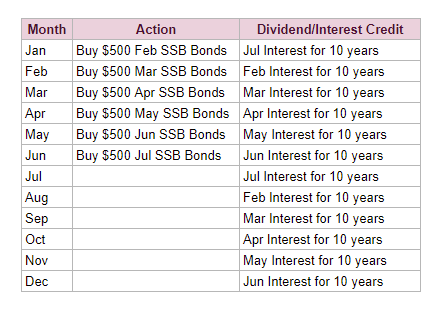

With $3000, you can form a Singapore Savings Bond ladder that pays you every month. You can look at the admin charge as the cost to get this higher yield interest.

An example of the Singapore Savings Bond Bond Ladder

The table above illustrate how this can be done. For 6 months, you will accumulate different series of Singapore Savings Bonds.

For the next 10 years, you will have 12 interest payment that comes in at all the different months that qualifies you for the investment tier.

Another advantage of the investments category is that, while my income is not more than $30,000, there are some months where I would purchase stocks worth $25,000 to $30,000 which allows me to hit the highest rate of 3.5%. With the enhancement to the Multiplier, I may be able to earn 3.8% on another $50,000.

It is likely I cannot be buying stocks every month at that frequency, I can offset my brokerage fee with this Multiplier interest.

The brokerage fee on a $30,000 transaction is about $60, and the extra interest on the Multiplier at 3.5% to 3.8% can reached $125/mth more. This more than offset my brokerage costs.

4 You may happen to have Insurance Protection Needs

And this would allow you to fulfil that all important third category. However, you have to note that the insurance premiums paid would only qualify you as an eligible Bonus Interest transaction for 12 months. After which, DBS will not count this purchase as a category anymore.

DBS have a 15 year working relationship with Manulife Insurance so there are an assortment of regular insurance plans that qualify for this.

They include:

- Endowment plans

- Investment linked plans (Kyith do not advise you to get this)

- Retirement plans

- Education plans

- Income stream plans

- Decreasing Term Mortgage Insurance

- Term Life Insurance

For most of my readers, I do recommend that you organize your financial objectives well. Do not mix protection and wealth building needs.

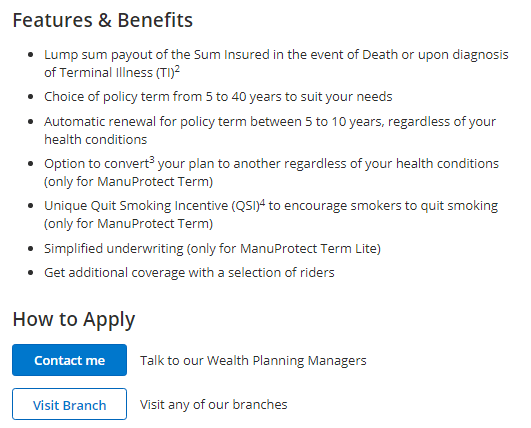

With the thought of satisfying this transaction category I can see you purchasing a term life insurance to augment your current insurance coverage.

The illustration above shows the description of ManuProtect Term, which is a term life insurance that should qualify you as an eligible transaction in this category.

More so, it is likely to meet your protection needs, does not contain cash value, and premiums should be low enough.

I can see myself getting a 5-year term worth $50,000 or $100,000 in coverage.

How much is the premium? You would need to approach a Wealth Planning Manager or a DBS Branch to get the quotation. This is because your premiums will differ based on your age, pre-existing conditions, the term you are looking for, and whether there are any riders attached.

However, we can have an estimation.

If you look at my Cheapest Term Life Insurance Comparison, a Manulife Term Plan covering $1 million costs $1523/yr for a 40 year old and $1044/yr for a 30 year old. While $1 mil is likely cheaper than smaller amounts, if you are covering $100,000, your annual premiums could be closer to $152/yr to $104/yr or $12.66/mth to $8.66/mth.

Now, if this qualifies me for the third tier interest, it means by doing this I can earn $50,000 x 2% = $1,000/yr in interest to $50,000 x 3.8% = $1,900/yr in interest.

It looks worth it.

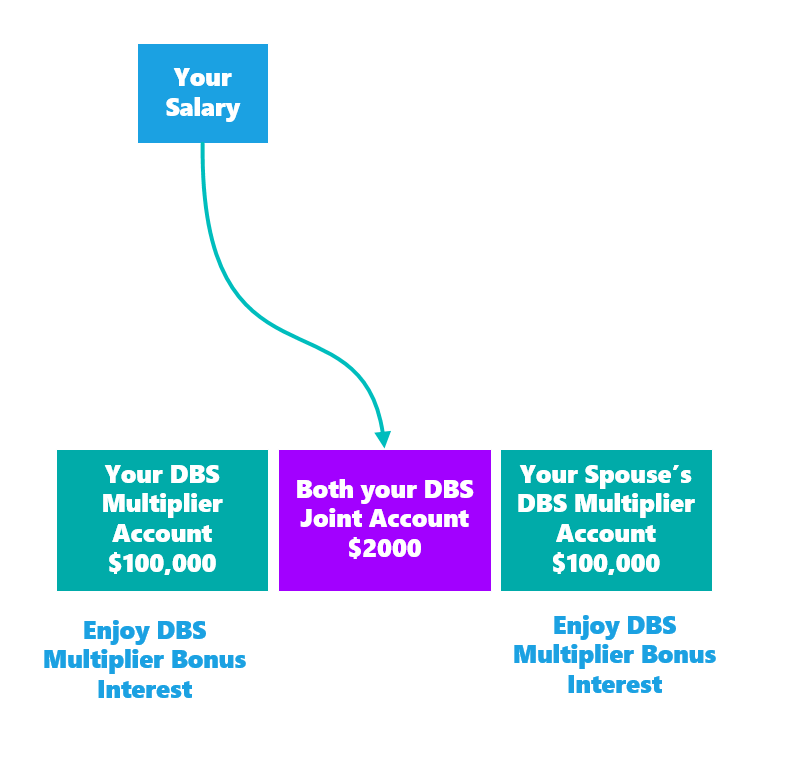

5 Allow you to Optimize Your Family Savings Well

Perhaps the biggest appeal that Kyith cannot enjoy is to use only 1 salary credit to potentially enjoy higher interest on $200,000 of your family’s savings.

I am not sure whether I should write about this, but it seems this is openly discussed in The Burrow, DBS’s own vibrant Facebook Community. So if you wish to find out more ways how to take advantage of DBS’s services, you can join the 10,000 folks in the community today.

So basically, you do not have to credit your salary into the DBS Multiplier Account.

You can credit into any DBS/POSB account and they will be able to track it.

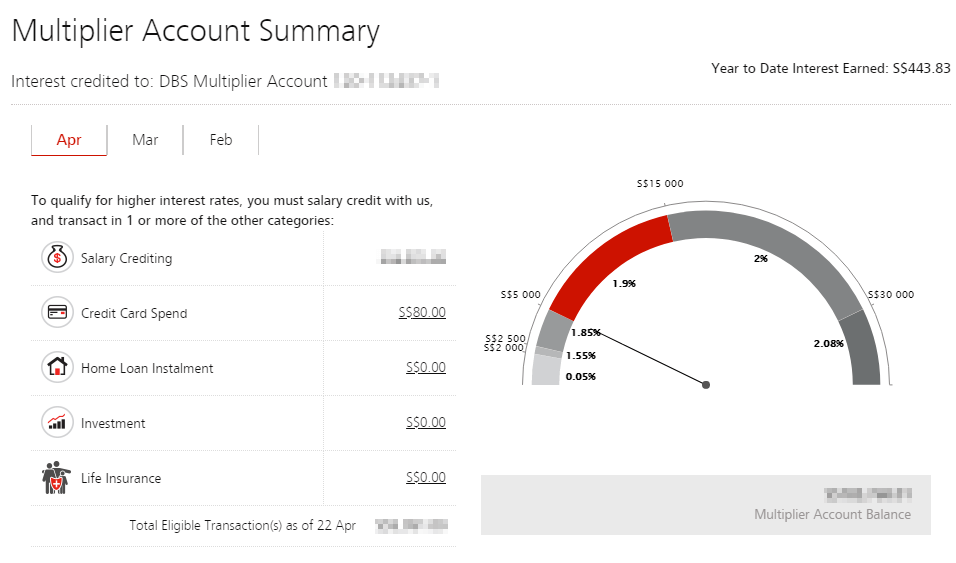

A pro tip: Under your DBS digibank, Under Accounts, there is a Bank and Earn Summary:

This allows you to see whether you manage to hit all the criteria and what is the interest tier you are. This removes a lot of the uncertainty whether your transactions qualify for bonus interest.

The beauty of the Multiplier is that if you credit the salary, and transactions to a joint account shared with your spouse, or another person, both your DBS Multiplier accounts will earn the bonus interest if you qualify for it.

So in the above illustration, suppose you qualify for 3 transaction categories, due to your salary credit both your DBS Multiplier can earn interest on almost $200,000.

This frees up your spouse salary to tackle another hurdle account.

The joint savings account is not the only account that you can maximise.

There are a few accounts that are joint, that can boost the total transactions:

- Credit card. Joint and supplementary cards

- Mortgage

- CDP Accounts. Both your buy transactions will boost the transactions, and so are both your dividends

6 No Minimum Transaction per Category is the Multiplier’s Greatest Advantage

You might not agree with me, but for me the absence of minimum transactions for each category is what made the DBS Multiplier the most appealing.

If I look at the competitors, the one with the lowest hurdle is UOB One Account. That enables me to earn an average of 2.44% on $75,000 in deposits. This is pretty good.

However, in the grand scheme, my transactions would likely give me 2.20% in interest on $50,000 on DBS Multiplier Tier 2 interest.

While we are at this point, we are comparing the different accounts whose hurdles you can realistically achieve:

- Salary credit of $2000

- Bill payment

- Credit card transactions of $500

And the realistic interest that you could earn with this permutation is:

- SCB Bonus Saver: 2.05% on $100k deposit

- MayBank SaveUp: 1.12% on $50k deposit

- BOC Smartsaver: 2.35% on $60k deposit

- OCBC 360: 2.1% on $70k deposit

DBS Multiplier, with Tier 2 interest of 2% to 2.30% is not so different from its competitors. For myself, since there is not so much difference, there is little impetus to shift.

What made me stick with DBS Multiplier is that for all of them, credit card transactions of $500 is mandatory.

And over time, the banks have been tightening up on what is considered as eligible transactions that allow you to earn bonus interest:

- AXS payment is not included

- Some town council payment is not included

- Ez-link, flashpay top up is not included

So what qualifies are the telecom spending transactions, real retail spending transactions, cab rides.

For some of you with higher household expenses, this might not be a problem, but for some of us who are more frugal, there might be some months where we do not qualify.

So it is very freeing to know that if I did not spend so much on my credit card, didn’t buy so much insurance or unit trust, I could still enjoy relatively good interest.

Finally, like DBS Multiplier, the other banks challenge you to fulfil higher transaction amounts to earn higher interests:

1. SCB Bonus Saver: 3.13%, if you bank with them, high credit card spends of $2000 and above

2. MayBank SaveUp: A lot of the minimum is just too high

3. BOC Smartsaver: 3.55%, if your salary is $6,000 and above and credit card spends is $1500 and above

4. OCBC 360: 3.0%, High minimum for insurance and investment plans

To earn the higher interest from the accounts of these banks, you need a lot of high, recurring insurance, investment, salary and credit card transactions.

With DBS Multiplier, you might need recurring insurance, mortgage and credit card spend, but you do not need to have high amounts.

It suits me that in certain months I can boost the interest rate if I make a large stock purchase.

Summary

I used to think that having a high interest rate is the be all and end all.

That was when I have readers that tell me that for some banks the interest is indeed high, but they cannot get used to the challenging interface.

For others, they are big credit card spenders, and in that case, some other high yield savings accounts might be more applicable.

Our consumption patterns are different, and soon you will realize what worked for me might not work for you.

I do think there are various aspect of the DBS Multiplier account that would appeal to a lot of you and I hope I have highlight them well.

Do check them out if you are interested. The folks at DBS paid me to tell you guys more about the changes to the account, but they did not put a gun to my head to use this account.

Let me know your thoughts.

This is a Sponsored Post with DBS. The views are of Kyith’s.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Eddy

Tuesday 3rd of September 2019

Hi, But the dividend from ssb is only recognized for first 12months right? I mean to be eligible for the extra interest rate for dbs multiplier

Kyith

Tuesday 3rd of September 2019

If i am right it is still more than 12 months. did they change something?

Evon

Wednesday 24th of July 2019

Hi, for SSB, should i use joint account to earn the interest or individual multiplier account?

Kyith

Thursday 25th of July 2019

you should let the SSB credit the dividends/interest to the joint account. that way both multiplier accounts will earn the bonus interest qualification.

yp

Saturday 8th of June 2019

Hi Kyith,

If you still happen to be talking to the DBS folks, can you please feedback that it's quite ridiculous for them to expect the card spend to be CREDIT card (apparently debit card spend will not be considered https://www.facebook.com/dbs.sg/posts/hi-i-have-just-opened-the-dbs-multiplier-account-i-have-the-passion-posb-debit-c/1899632870150953/). Those earning about $2,000 are certainly no eligible for their credit card that require minimum income of $30K a year. Thank you!

Kyith

Saturday 8th of June 2019

hi yp, will feed back about it.

Kongming

Friday 7th of June 2019

Hi Kyith, What can be do for term insurance after 12 months as you mentioned insurance premiums paid would only qualify you as an eligible Bonus Interest transaction for 12 months. After which, DBS will not count this purchase as a category anymore. Shall we change plan or add plan to continue enjoy this hurdle

Kyith

Saturday 8th of June 2019

you could cancel the plans after the 12 months. the lowest premium plan is a decreasing lite term insurance.

Andrew

Thursday 23rd of May 2019

Hi, how much interest will be given when the dividend (sg bond) is given on that month?

Kyith

Thursday 23rd of May 2019

are you refering to the singapore savings bond?