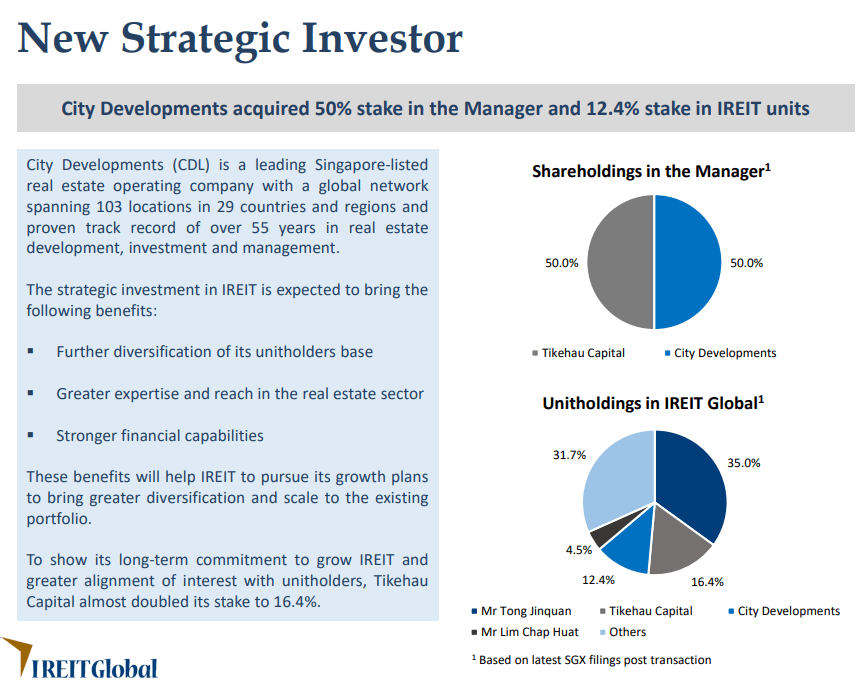

At the end of April, City REIT Management, a subsidiary of City Development Ltd (CDL) purchase 50% of IREIT’s manager. City Strategic, also a subsidiary of CDL, purchase a substantial stake in IREIT itself.

In November 2016, Tikehau Capital purchased a 80% stake in IReit’s manager. The rest of the stake is held by Chinese Tycoon Tong Jinquan and Soilbuild founder Lim Chap Huat.

Tong Jinquan owns 297 mil units (47%), Chap Huat owns 33 mil units (5.2%), Tikehau Capital owns 52.6 mil (8.3%).

In this deal, Tikehau Investment Asia Pacific bought back Tong’s stake in the manager. They then sold half the stake in the manager to City Reit Management, which is CDL’s arm in doing reit management.

Now, Tikehau and City Reit owns roughly 50% each in the manager.

Then, Tikahau increased the shares they held in IREIT. They bought 50 mil shares or 8% of IReit from Tong. They now own 16.4% of IREIT.

City Reit bought 75.6 mil shares from Tong and 3 mil shares from Lim Chap Huat. They now own 12.4% of IREIT shares as well.

Tong owns 35% stake in IREIT still.

The minority shareholders own 36% of the rest of IREIT Global.

What are Each Stakeholder’s Motivations

If you ask me whether it is CDL that is more interested in purchasing IREIT as a platform, or whether Lim and Tong are more interested in selling IREIT away to someone else, I would think it’s the latter.

Ho Toon Bah, a director in Soilbuild, stepped down as a director and in his place Frank Khoo of CDL became a director. Frank Khoo is CDL’s Group chief investment officer.

Subsequent to the announced deal, Tong is still pairing down his stake in IREIT little by little.

It sounds to me that Tong and Lim would like to reduce their stake in the Reit.

So Tikehau shopped around.

And CDL is rather interested in having a Reit platform that is non hospitality based. CDL already have CDL Hospitality Trust but other than that, they do not have a platform for retail and office.

Frank said this of the acquisition:

“As part of CDL’s transformation, we are developing our fund management business through organic growth coupled with the acquisition of assets and platforms,” Mr Khoo said.

“This investment in a Reit is in line with our aim to achieve assets under management of U$5 billion by 2023.

“Besides being earnings accretive with immediate contribution to our recurring income through management fees and attractive yield, the investment in IReit Global complements our existing CDL Hospitality Trusts and will strengthen our Reit management expertise.”

In recent years, you are seeing the developers following the footsteps of Fraser’s Property, to strengthen their recurring income stream as a larger percentage of their income stream.

It is as if telling us that development in the future is going to be extremely challenging.

Capitaland and Keppel are notable ones talking about this shift in mandate.

And I think Tikehau will find CDL to be the perfect partner for them to work with.

So much so that they are willing to increase their holding (or perhaps Tong is desperate to pare down)

Is this good news for IREIT’s shareholders?

This news might be good news for existing IREIT’s shareholders.

IREIT is getting close to being a 5 year old REIT. If you are an existing shareholder, you might be wondering about where the REIT is going. How Tikehau is going to grow the REIT.

When Tikehau took over from the previous manager, they provided a slide of potential acquisition target. They also sought to expand their investment mandate.

Since then, there were no acquisition made.

By working with CDL, Tikehau may have a partner that, in the eyes of local investors, are known to be rather astute property investors.

The main advantage for the shareholders is that with CDL, is that while they parent may not have so much offices, equity and debt capital raising might become easier now.

If both CDL and Tikehau has an economic incentive to grow their AUM, so that they can earn fees from it, they are likely not contented to just inject assets that would impede future assets from being injected into the REIT.

How would growth take place?

CDL is not known for most things other than luxury private homes and hospitality.

And if we are looking for a large pipeline of quality injections, we might not see that take place.

In recent years, CDL have acquired 2 office buildings in the United Kingdom:

- 2016: Development House

- 2018: Aldgate House for 183 mil pounds. Aldgate is grade A office and retail, 88% occupied with a 5% passing rent yield.

With CDL, Tikehau might still be looking at acquiring third party assets instead of these from CDL.

IREIT currently pays about EUR 3.56 cents.

With the weaker Euro, a conservative local DPU is 5.47 cents.

At a share price of SG$0.74, this works out to be a dividend yield of 7.4%. The current debt to asset is 37.7%.

IREIT’s cost of equity is still very high.

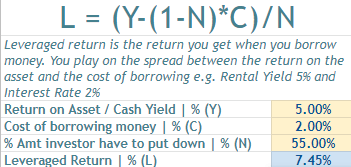

Suppose if we wish to make the CDL’s UK prime purchase to work out, and imagine that they inject this to the portfolio.

Based on the passing rent of 5% and UK cost of debt to be 2%, IREIT would probably need equity raising of 55% and taking on 45% debt to achieve an accretive acquisition. By doing this, it allows IREIT to be injected with good quality office asset that has good appreciation value.

But this is rather tight.

The hope is that with CDL, IREIT could do a non-renounceable rights issue that is 10-15% discount (a not very tight range) with CDL choosing to take a big chunk of it.

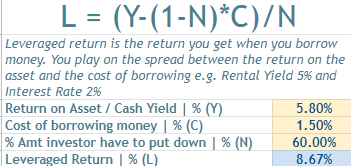

The likely long term acquisition horizon could be possibly in the areas that Tikehau highlighted in their slides long time ago.

The acquisition profile can be something like the above. The net property income yield would be higher than UK, and the cost of debt to be cheaper in Euro. Even by putting down more equities, it should still be rather accretive.

Fundamentals of IREIT Global

There are always some things that you like about a REIT and some less desirable things.

Let me go through some characteristics.

The trading volume is on the low side. I have list out the average trading volume below:

Average Trading Volume:

- ESR REIT: 4 mil

- Manulife US REIT: 1.1 mil

- IREIT Global: 0.4 mil

- Mapletree Commercial: 8.3 mil

- Capitaland Commercial Trust: 13 mil

The trading volume is important to provide liquidity. Without the liquidity, institutional investors, who have larger pool of money find it hard to get in or get out.

With difficulty, they might not want to get invested

Minority Shareholders hold a small proportion of shares. Not sure whether this is a good thing or not. On a day to day basis, there are currently not much surprises to the operation of the REIT.

And so since a large proportion of shares are tightly held my Lim, Tong and Tikehau, this REIT resembles more of those godfather property play where it is not so much traded.

Some of my friends like this kind of companies. Some do not like due to the lack of growth catalyst.

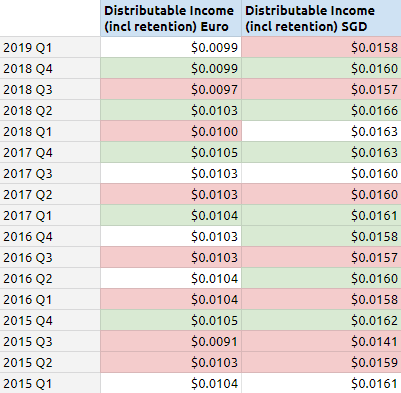

Dividend Per Unit not Growing. I have tabulated IREIT Global’s available distributable income over the years. This includes the amount that they retain, since IREIT only pays out 90% of their available distributable income.

I have listed out the amount both in Euro and Singapore dollars. Red denotes a decrease from last quarter and green denotes an increase.

If we look at the profile on its own, in terms of Euro, the distributable income have not been increasing.

This is despite a build in CPI escalation for most buildings. Since inflation is very very low in the region, recent decrease in distributable income per unit can be attributed to more expenses.

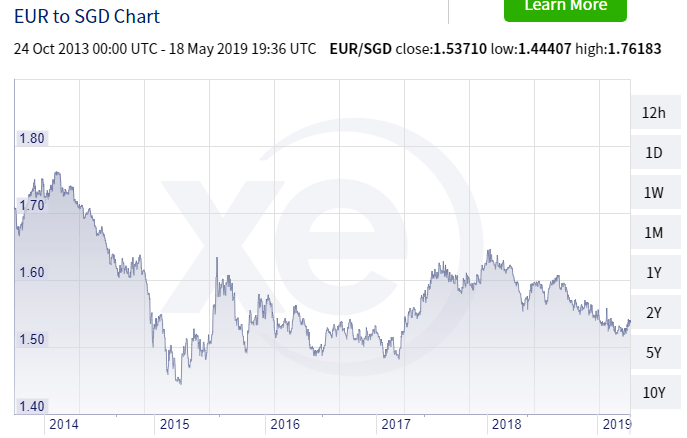

In Singapore dollars there are more decreases due to the strength of the Singapore dollar versus the Euro.

If we observe the 5 year chart of EUR versus SGD, we can see the currency fluctuates in a 1.50 to 1.60 band.

If we observe the 5 year chart of EUR versus SGD, we can see the currency fluctuates in a 1.50 to 1.60 band.

This is a 6% range and depending on how you look at it, your dividends may be

- 7.4% + 3%

- 7.4% – 3%

IREIT does hedge the dividends on a quarter to quarter basis 1 year in advance so as to smoothed out the volatility.

But if you look at where the currency is at, and if you are speculative, perhaps now we are at the lower side of the band?

IREIT not growing its DPU over time. This is due to a lack of organic growth through AEI, rental escalation, renewals. This is also due to the currency difference making the DPU volatile.

And that would be a problem for investors to participate in since, if DPU is not growing, the demand is not there, the share price would not grow.

Their yield on their AFFO/free cash flow/distributable income is likely close to 8.2%. It would take a quality REIT like Capitaland Commercial a lot a lot alot of DPU growth to reach this.

But investors prefer the quality REIT because despite the low yield, they know that, factoring currency fluctuations, vacancies, rental escalations, acquisitions, AEI, the dividend yield is protected (since each quarter is usually higher)

With a REIT with high dividend, there is this susceptibility that you have 8.2% this year but in the next few years, if the currency trended down, the dividend yield net of currency fluctuation is closer to 5%. There is a lot of uncertainty there, and investors do not like uncertainty, would choose not to get invested.

The inefficiency is when things are different. Currency is on a secular change in trend due to a change in trend in the region. The properties are more diversified. If the REIT is well managed, more diversified and gives you 7.5% for 4 years, perhaps some form of re-rating by the market will occur.

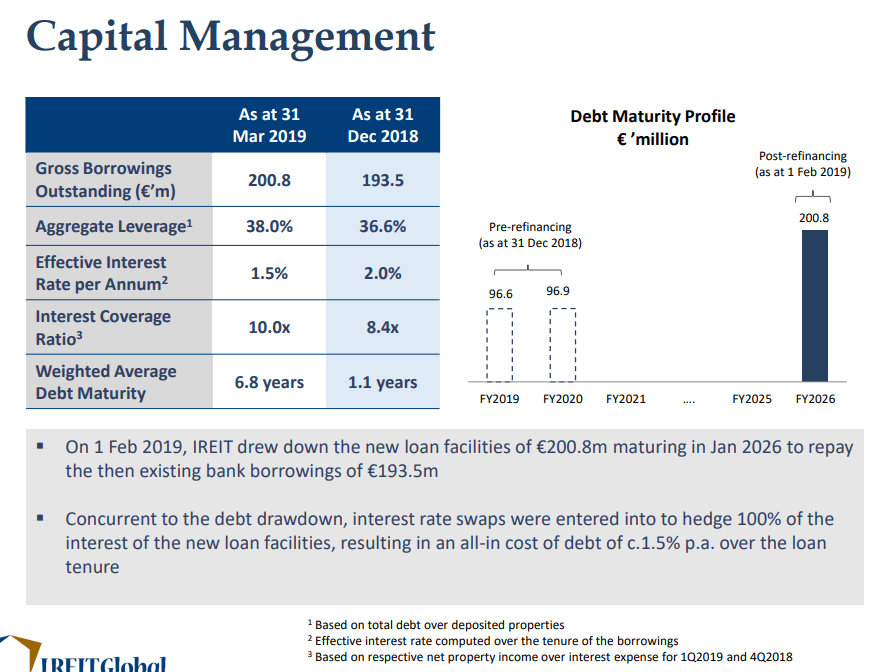

Debt Risk drastically reduced. The appeal of investing in Europe that counter balanced the lack of growth is that the cost of debt is low.

IREIT managed to refinance ALL their debt to 5 years later, at an average interest rate of 1.5% versus 2.0%.

This removed any debt refinance uncertainty.

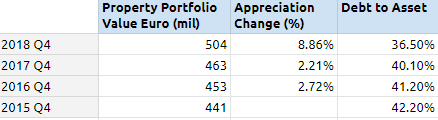

Asset Value is Slowly Appreciating. In land scarce Singapore and Hong Kong, we have seen much price appreciation in asset value. The advantage for a property investor is that it increases the amount of leverage that you can take.

When a new REIT comes onto market, we are not sure if they are dumping poor assets that would not grow.

If the assets are poor, their value goes down, it puts more pressure on the amount of debt you can take.

I have tallied the price appreciation/depreciation versus the debt to asset over the past 4 years.

IREIT global could possibly be the rare portfolio where there were no injections so we can see the effect of the appreciation over time.

The growth have been rather low. Well if you factor in non existent inflation then this 2% real growth is not too bad!

For some reason the latest property revaluation values the portfolio almost 9% higher.

And you can see the effect on the debt to asset.

What was not so safe, suddenly look pretty OK. Perhaps due to Brexit, and the relative strength of the German economy versus the rest of Europe have increased the demand for German property.

Summary

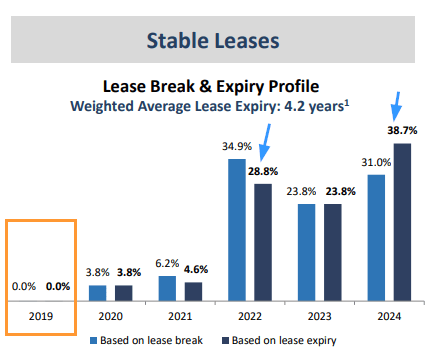

I think one thing I highlighted in my last post of IREIT 1 year ago was that there was 14.5% of the gross income has break clause and 8.4% have lease expiry in 2019.

Of the 8.4% expiring in 2019, 3.6% gets pushed to 3 years later, and 4.6% gets pushed to 5 yeas later. Perhaps not all tenants would want to lease for a long time. But at least it shows that there are demand for the spaces and that the manager is able to lease out the spaces.

Sometimes it does irritate me that I have to reverse engineer to find out some of these things. Perhaps they were revealed a few quarters ago and I have missed it.

In any case, with CDL’s involvement, I think IREIT will evolve.

How would it evolve, I am not much clearer than you. I do certainly think this is a good development.

I write more about REITs in my Learning to Invest section below. It is free.

Do Like Me on Facebook. I share some tidbits that is not on the blog post there often. You can also choose to subscribe to my content via email below.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

randomwm

Sunday 19th of May 2019

Every REIT manager wants to grow AUM and grow its management fee income, whereas REIT owners benefit form growing DPU and NAV per share. In order to fulfill their ambition to grow AUM, manager REIT managers will cause the REIT to do a rights issue, which is often to the detriment of the REIT holders.

Take Link REIT in Hong Kong for example - no rights issue but delivered to its unitholders 10x return in 10 years. Another Hong Kong listed REIT, Prosperity REIT had its rights issue blocked by its unitholders in 2016, with the blockage led by none other than the REIT's largest holder, Cheung Kong Property. The above two example goes to show that what REIT managers do may not have the best interest of the unitholders in mind.

It is time we change the rules and regulation in Singapore so that the minority rights of unitholders are better protected, and REIT managers are being called to task for destroying unitholder value.

Kyith

Monday 20th of May 2019

Hi randomwm, how would you change it. personally i do not think this is much of an issue. People vote with their money.

In any case, why is this a matter in this IREIT discussion?

latemonkey

Sunday 19th of May 2019

Thanks for the very informative post.

IReit Global draws 51% of its income from Deutsche Telekom. And it has been reported that Deutsche Telekom is now downsizing. The lease renewal with Deutsche Telekom will not happen until 2022/2023. But it's hard to go long on this reit. I see this as a problem. Not sure about other investors, though. Oh, that the stock is not as liquid as those of the big boys is also a concern, as you highlighted.

Kyith

Sunday 19th of May 2019

hi latemonkey thanks for raising that good point. that is a genuine risk there.

BlackCat

Sunday 19th of May 2019

Hi Kyith,

IREIT Global's main tenant, Deutsche Telekom, seems to be long term downsizing. See https://www.valuebuddies.com/thread-5432-post-152566.html#pid152566

So I'd wait for the lease expiries in 2022 & 2023, to see how they play out for IREIT Global.

Its a pity, because I liked everything else about them.

Kyith

Sunday 19th of May 2019

Hi BlackCat, nice to see you around! That will be a long wait but I have to revisit which tenant was expiring in 2019 and whether that is deutsche. if it is it may show that things are not so bad.

There is this part of me that thinks if things are very clear, then there might not be a premium there to be earned.