Singapore Press Holdings announced their Q3 2012 results yesterday.

- Net Profit for the quarter down 10%. this was largely due to lower Net Income from Investments

- Net Debt edges up. Net debt to asset is now 16% from 13% a quarter ago. This is largely due to investing in new Seletar land for shopping mall development

- Operating Cash Flow, Investing Cash Flow largely negative due to higher receivables and investments in new Seletar land venture

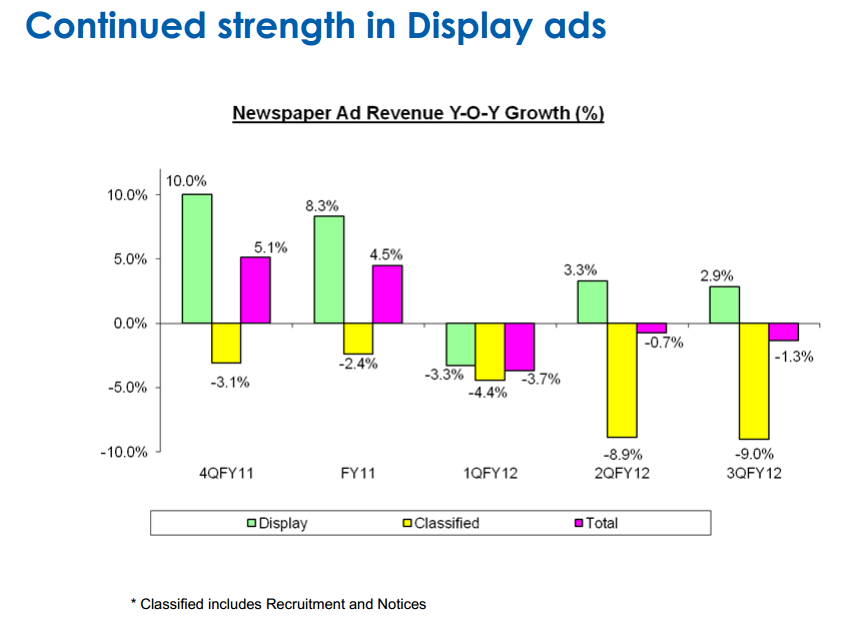

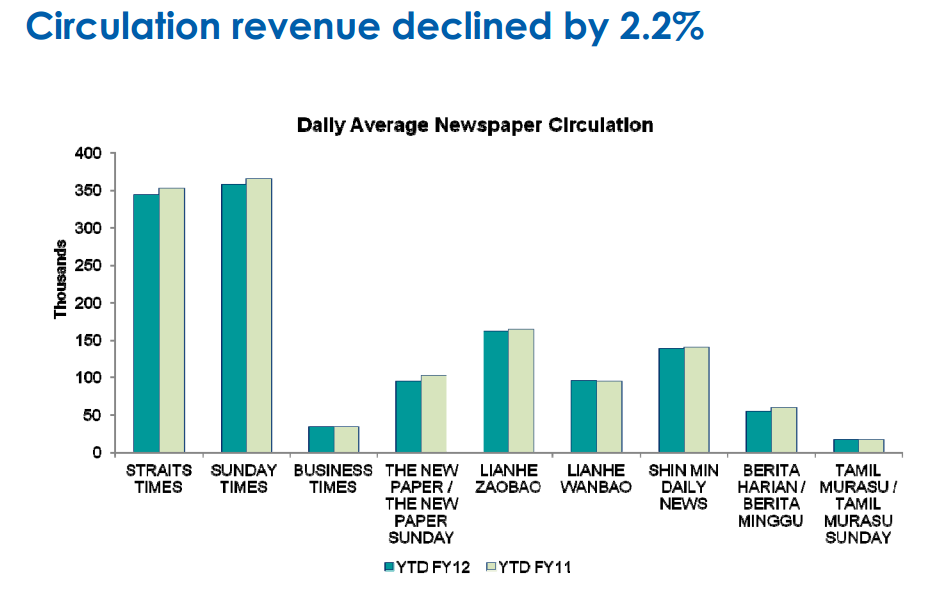

Fall in newspaper circulation

I went for a three week reservist training not too long ago and as I usually do not buy the Straits Times I took a look at it. The content is largely the same. The surprising thing was how thin the classified section was. Full page ads still look pretty well taken up.

I asked around and seems like no one orders newspapers at home any more. But it is somewhat surprising that circulation figures published by SPH remains strong.

Perhaps I didn’t pay enough attention to the figures as I suppose to. Classified section have shown a dramatic QOQ fall. It used to be that if you would like to sell cars, find jobs you have to use the papers because that is the most prevalent media.

Now its different. Singapore is one of the country whose population spends the most time online. Online job sites, free classifieds like Hardwarezone to buy and sell things and SgCarMart provide better alternatives.

SgCarMart charges $48 for a front page space to list your car for 6 days compare to $36 per day on a weekend classified listing.

The puzzling thing for me is if everyone I talked to are not subscribing to it, why is the circulation still so high. Perhaps it’s the trend that people prefer to buy it off newsstand.

Should the circulation trend continues to go down to a much lower terminal rate, advertisers will re-evaluate whether print media reaches their target audience effectively for the amount they pay for it. Other media sources could be more effective per unit cost.

Revenue is likely to trend down base on economics. I still don’t see it being affected in a big way.

New online ventures acting as insurance rather than adding to bottom line

SPH online media strategy is to capture all the popular eyeballs and be in the face of internet users. If there is a new startup garnering a lot of eyeballs, they will acquire it like Hardwarezone, if there is a lack of demand they will create it.

They sell advertisement space on these new media. However, the dynamics of the economics of online information space is different from last time. In the old days, information sources are scarce. Its either the TV, newspaper or bill boards.

Now, Singaporeans can have access to overseas content sites for niche information on healthcare, technology, investments.

Still local news is where SPH has a niche. But so do Mediacorp, which is owned by Temasek and they readily offer it through Channel News Asia for free rather than behind a paywall (Straits Times and Business Times online are subscription based)

Singaporeans are a strange bunch. They have a tendency not to spend on digital goods compare to physical ones.

They will need their news on their smartphones, but the usage pattern is also one that people need to consider. A group of people like to have papers so that they can occupy their journey to and from work.

Now that Singapore have become so congested its not feasible to hold on to large newspapers.

News apps to commuters is a way to keep up with latest news. But not many would value a detail coverage. They may like to know what actually happen rather than well thought out editorial, which you need good journalist for. In such a scenario, channel news asia serve its purpose,

This would mean people not opting for paywall based local news.

The advertisement revenue for digital space is also lower so all this means is that unless the Singapore folks value good local news, SPH will find it hard to totally replace print media.

They can spread out the profit stream but its probably replacing a 50% ROA profit stream with one earning < 5%.

Right now, these online media ventures are reflected in the Annual reports or financial statements as Others, which is losing money for a few years.

SPH essentially look at them as some form of insurance hedge but doesn’t develop them as an income stream. I wonder if this is the right strategy to take.

Largest Cost cannot be reduced easily

To compound to the two points mentioned before, the largest part of the cost for SPH have been staff cost, which accounts for 41% of total cost.

With wage inflation rampant, this component have been rising due to increase in headcounts and better payout to retain quality staff.

Revenue trend is falling, major cost is rising. Not a good picture.

Creating a Retail Rental Income stream

I was told by my friend that there were thoughts that SPH may want to sell of their Paragon Shopping Center. Looks like they make a wise decision not to.

SPH in the past two years have sought to prepare for slowing news media income segment by building up a retail rental business.

They acquired Clementi Mall at a crazy premium.

Since SPH was originally not leverage, they can leverage up to increase their income stream. I originally like the idea that unlike a REIT, they would have the flexibility to pare down the loans using their excess income.

Dividend Cover

But I realize that even with this new leverage segment, they are barely keeping up to pay their dividends.

Paragon and Clementi Mall are likely to contribute $100 mil to their cash flow which can be used to pay their $0.24 dividend, which requires $383 mil. Even with Seletar Mall coming online in 2015, that should contribute another $30 mil at a 5.5% Cap Rate.

SPH will continue to create more malls, but it only serves to make up for loss newspaper income stream.

The worry for investors is whether they can come online fast enough or is the newspaper slowdown going to be much faster than anticipated

Warren Buffett buying up local community newspapers

Warren Buffett was in the news a few months ago and also these few days telling the media he has been and will continue to buy newspapers.

The key here is that he is not buying the corporation behind rather than the local newspaper publishers that provides updates that are more community centric

“These are smaller newspapers generally. Newspapers used to be primary virtually everything. They have lost their primacy in many areas. If you lived in Nebraska and you are interested in at Nebraska football or your high school and what is going on with your neighbors, you are only going to find it in the independent papers. The smaller paper is still primary to many areas of interest.”

He also gives his take on whether he will buy newspaper corporations:

“I would rather buy newspapers myself directly…I like buying individual papers at the right price. The prices should be low because their revenues are going to decline over time. We are not buying into a business where revenues are going to increase. We have to buy them at the right price. We have to buy papers that are subject to less erosion because they have lost their primacy.”

Essentially, what he see is that upside is capped and the price you pay for it is important. He sees that he can get reasonable value since these news corporation wants to sell away these papers on the cheap.

Back to SPH. If you look at SPH as two publishing unit, the local and non local news, what they provide can be something that Buffett describes. In that context, There will always be a group that wants their news in physical paper form and are willing to pay for it.

However, the internet penetration I feel, seem to point to a more internet, smart devices and TV centric news consumption and it points to Channel News Asia being a bigger competitor in the future.

Closing thoughts

I see SPH as a bond like equity. When you assess this bond you look at the reward for the risk borne. As a media shop they are not going to go away, but a poorer business model means that this bond have no clear room for future growth.

Free cash flow is maintaining at 380-400 by new property income stream. However the difference is that it is maintained by additional leverage.

With a price earnings of 17 times and EV/EBITDA of 11 times, it seems to be value more like a fair stock but a great return on asset like IBM or ARA Asset Management.

Yet the problem is that its future return on asset looks to be much weaker.

Yield chasers would have to beware and not buy this at a dear price.

To get started with dividend investing, start by bookmarking my Dividend Stock Tracker which shows the prevailing yields of blue chip dividend stocks, utilities, REITs updated nightly.

Make use of the free Stock Portfolio Tracker to track your dividend stock by transactions to show your total returns.

For my best articles on investing, growing money check out the resources section.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- New 6-Month Singapore T-Bill Yield in Late-April 2024 to Drop to 3.70% (for the Singaporean Savers) - April 18, 2024

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

KC

Saturday 21st of July 2012

Thanks Drizzt for sharing with us your thought on SPH which was insightful vs the typical analyst reports

I took a look at Washington Post’s FY2011 Annual Report.

The newspaper publishing business now comprises 15% ( US$648M ) of total sales of US$4.2B. WP has diversified into other businesses like private education (58% of sales), cable TV, Television broadcasting. Even in the private education space they are facing government regulations to phase out the fly by night providers ( same in Singapore) and it affected their performance badly. Newspaper publishing recorded a loss from operations ofUS$18M.

Daily circulation has dropped to 524K in 2011 vs 615K in 2009.

Chairman says tt they need to transition to a new business model for publishing. Take tt to mean digital news ; they have developed new products like personalized news site called Trove and a facebook app. Washingtonpost.com averaged 273.4M page views per month; average of 35.7M unique visitors per month. Chariman says cost cutting is inevitable and crucial part of the future.

Fortunately SPH has fared better than WP. Newspaper and mags sales was S$1B and comprised 80% of sales and it is profitablefor last financial year. SPH combined daily circulation( English, chinese, BT,etc) is 981K.It is also declining yearly which is a worrying sign. However I think that erosion will be slower because SPH is a monopoly and although digital media had eroded that competitive advantage it has a few more good years to build up its digital business and diversify into other businesses like property. I heard that they bidded for a fairly big education company in Singapore but were out- done out by private equity funds.

I don’t quite know how to evaluate the success of its digital news attempts and how profitable it would turn out to be.

For a LT investorlike me I think SPH is safe for now. Need to constantly monitor this stock but it should not comprise a significant part my portfolio. I will not buy at current price. Rgds.Adenium

Drizzt

Saturday 21st of July 2012

hi KC, no thank you for sharing this with my readers. i take that to mean WP have become a conglomerate. news publishing and media goes hand in hand and i wouldn't be surprise if M1 and SPH merges.

imagine M1 have exclusive free or heavily discounted delivery of Straits times digital.

as investors, we need to know why we invest in it, and what are the clear markers that this is not a good investment. if we view it as a leverage equity bond yielding 6%, when the cash flow cannot meet this, we should be thinking about switching.

i believe we should be able to find more similarly leverage play yielding 6% with a brighter and sturdier moat.

B

Monday 16th of July 2012

Good article.

SPH imo is a matured business. And when a business is a matured one, we will at times be looking at declining demand and declining profits at times when you compare year on year. I think it is an anticipated outcome given the nature of the business don't you think so.

Just thinking from a different point of view and would gladly have your thoughts on this as well.

Not vested at the moment.

B

Aaron

Monday 16th of July 2012

Hi Drizzt,

I believe that SPH knows that their circulation revenue is declining because of the boom of smart phones and tablets and hence they decided to venture into property to ensure that they are still able to get decent rental yield and at the same time retain it's property value.

But i am also certain that they are slowly moving away from the print business due to our small population

Just my 2 cents

PS : I like reading your posts =)

Drizzt

Tuesday 17th of July 2012

Hi Aaron and B, on first analysis that seems to be the case, but the speed of the fall in earnings from advertisement and circulation is rather subdued. Circulation and classifieds are down big. If they are down drastically before proprty starts ramping up their 24 cents dividend may be under threat.

James

Monday 16th of July 2012

Hi Drizzt, I've similar thoughts as you about SPH. A quick read of its latest results show that the only component that contributed to its growth is its property portfolio. Without it, its results would have been badly negative.

When the circulation decline starts to pick up pace, its advertising revenue will fall as well, when advertisers shift to other avenues.

SPH looks to be expanding its property portfolio. I read that it is developing Seletar mall. Please correct me if I'm wrong, it's business model is slowly becoming like a F&N.

smallbear

Sunday 15th of July 2012

Hi Drizzt,

Regarding ur question on newspaper Subscription remaining strong could be due to hotel subscriptions for their residents. If the tourist arrival rate remains strong, the subscription may remain strong.

As to the acquistion of online startups, i think they have made a gd acquisition of shareinvestor. But they need to do a lot more on this area as i think the media war of our century would be found on the internet front.

Juz my 2 cents worth....

Drizzt

Sunday 15th of July 2012

hi smallbear, thanks for visiting. that is a permutation that i have not thought about but in my opinion it should not add up to that much.

the media war is shifting but SPH seems to be the old industry that refuses to give up because the new play ground is not that much fun.