SPH have been a grandfather stock for many retirees and dividend stock investors.

- An attractive consistent 5-6% yield.

- A business that is well protected by the local government.

- Low barriers to entry but overwhelming incumbent.

- Main business is an old business that continues to do well.

I have to admit that for 2-3 years I have the impression that SPH is going to have a challenging business model.

- News will have no branding. Being a geek I am more attuned with how technology progresses. Although the internet have been around for some time we are at a certain stage where the 10-35 population will get most of their information from sources other than news paper content, be it BBC, CNN, SKY Sports, Soccernet, Teamtalk, Huffington Post, Download Squad, Finanical Times, Forbes. Those are niche providers of quality news and for readers of particular interest, the cost to switch to these other circulation medium is low.

- Free information abound. We don’t want to pay for it. We prefer to not be bound by subscription. News can be aggregated by Google News, iGoogle, RSS Feed reader from various sources. We also prefer news that are unbiased or from another perspective.

- News preference will shift towards social and search. GEN Y and Z lifestyle evolves to a form where they are very connected to the internet. There is a strong preference of information based very social and based on search. This is very different from the way we used to get news delivered which is mainly from the SPH journalist.

- End user attention shifts due to Smartphone and Social revolution.There is a smartphone revolution going on in Singapore. Singapore have one of the highest penetration rates of smartphone in Singapore. If you look around you on the bus or MRT the number of iPhones and Android phones outnumber phones that are at least one generation older. These phones with 3G connection are able to enable end-users to surf net where-ever they are, play games and stay connected socially. What this means is that instead of killing boredom on the train ride with newspaper and magazines, you would observe that they no longer need to do that as your smartphone can help you pass time much better.

All this points to

- The need for SPH to have a strategy to keep up with the times, leverage on new media and social means to deliver content to the evolving masses and monetize it.

- Protect the Advertising Revenue. This is an overlooked area. I used to have the idea that SPH based their profits on selling newspapers. Abit wrong there. I will illustrate later.

- Find other circulation means that they can monetize. They have to monopolize Singapore and regional information as much as they can.

- Find alternative sources of investments to diversify away the old-business risks.

How well has this worked out for SPH?

SPH’s Advertising Strategy

Here is my thoughts how SPH intends to be relevant:

Content is still king. Grab all the best content providers by offering them or buying them

At the end of the day, people will come to you if you provide the news they want. Where is the news they want? Buy them all up! If they don’t have it, Offer them!

One thing going for SPH is that they are still the largest provider of Singapore based content. They should not rest on their laurels but learn to open up and be more neutral in their content.

AOL’s example of buying Huffington Post for USD $300 million is the best example. AOL have slowly develop from offering internet services to becoming a content provider. All the highlighted links are leading content providers in each of their own categories.

The Key to the game is still advertising. Make your full suite of platform relevant to continue to attract advertisers.

It is made known that online advertising is much cheaper than traditional means. But really SPH do not have a choice, they have to take advantage of it. If not others will do it.

At the end of the day, the battle ground shifts, but SPH can still dominate it by hogging eyeballs. When eyeballs and content is theirs, advertisers will continue to see your platform as relevant.

Develop alternative sources of business to create recurring income.

Just like SingPost, they will need to put their Free Cash Flow to good use now. The best way is to evolve and not be reliant on their main core business.

Summary of SPH Businesses

Here is an analysis on their strategies.

- They basically have all the advertising medium sans TV and Radio tied up well.

- They have a 20% stake in MediaCorp as well which does the TV and Radio advertising.

- They are slowly building up their online portfolio of different segments. This is good but online readers can be more fickle than traditional readers. They will have to understand that and not use old management style for this.

- They have become a property development company. I viewed this as a negative since property development is very cyclical and does not provide consistent cash flow.

- They have recently bought The Clementi Mall to add to The Paragon. I like the idea that they are becoming part like a real estate investment trust. But the purchase of clementi mall was bad. It was expensive and they are working with NTUC. NTUC developed the disastrous Hougang Mall which thank god for Capitamall Trust who took over and resurrected it. Let me just say this: NTUC cannot develop a fun mall! I hope SPH knows what they are doing.

25 cents Dividend at 3.80 equates to a 6.5% yield

For its business, expecting a 6.5% market yield is not too demanding but also not very generous. Its just about right.

To pay out 25 cents, this would cost SPH 400 mil. The key is to see if SPH can consistently meet this 400 mil with Free Cash Flow or Profits

A closer look at readership, revenues and earnings

I know we can always focus on EV/EBITDA, Free cash flow and all those fundamentals but I would really like to show some 10 year data trends.

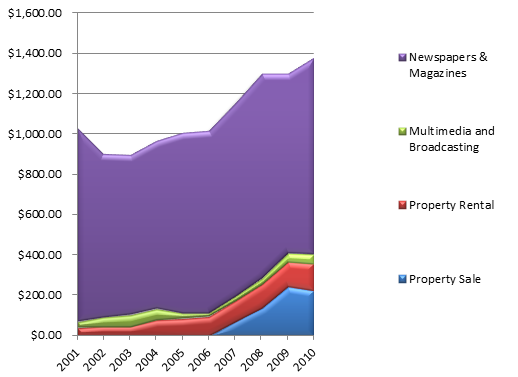

Segmental Revenue

Here is a chart showing the 10 year segmental revenue composition. Each segment stacks on top of each other.

Other than the dip in revenue during the recession in 2001 to 2002 (should be data of 2000 to 2001 really), total revenue have been rising.

Remember that back from 2001 to 2006, SPH does have a significant Radio and TV business. That flopped pretty badly until they sold it off.

From 2006 till now, they developed a property development business. This adds to overall revenue and profits to sort of diversify away the niche business risk.

But at the end of the day, a large part of the revenue is still made up of newspapers and magazines. I believe that much of the increase is due to the increase in population in Singapore.

In light of the challenges mentioned above, should we be concern?

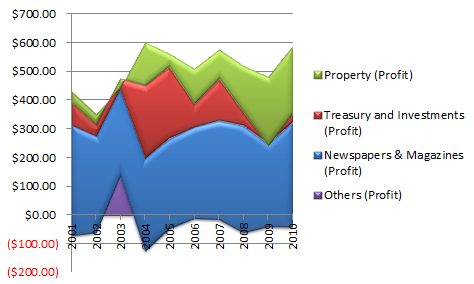

Segmental Profit

Here is a look at the 10 year profit by segments. Its abit different from the segments before.

Property is made up of both sale and rental. Treasury and Investments are the profits from their short term investments in bonds and equities. Others refers primarily to their old TV and Radio businesses.

Free Cash Flow analysis is a pain for me as there are many moving parts to it. I chose the lazy way of using Net Profits.

Average Net Profit for all segments for the past 10 years is 502 mil. For the past 3 years it is 530 mil. Safe to say based on profitability, SPH can pay out this 400 mil in dividends for 6.5% yield comfortably.

Its abit disappointing that no data showing New Media vs Old Media business segments. All of it are dumped within Newspapers and Magazines.

What we see here is that Property is making up for the performance loss in recent times from Treasury and Investments.

This segment of property + treasury and investments is important because it accounts for nearly 200 mil in overall profits. Quite sizable to the average Newspaper and Magazine profits which is around 332 mil.

The key for SPH is really to build up a sustainable alternative income stream not based on newspaper and magazines. Currently it is consistently at 200 mil, and we should see that Treasury and Investments are competing assets. The intention to acquire Clementi Mall signals the future as a quasi-REIT, but without the management fees.

If you are purchasing SPH as a niche newspaper play, you might want to look away because it is going against the core idea of focusing on where you are best at. Yet their management of Paragon have done ok. But what is Paragon’s net property yield? I have yet to uncover that. Shall try to post the question to investor relations.

A note on the segmental profit is the negative blue region. That represents the loss on investments in TV Media and Advertising. Its astounding why that segment really didn’t worked out. Perhaps the level of resources require (the quality that is) is not enough to making it worth while.

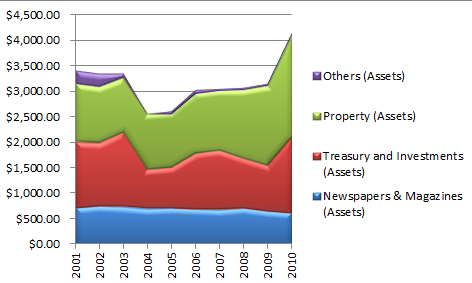

Segmental Assets

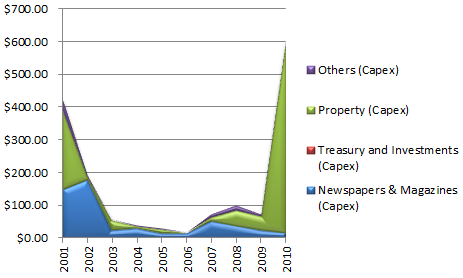

One area you will notice is that assets growth for Newspapers and Magazines(blue) have stayed largely constant. Little capital expenditure goes into this area in the last 10 years. (Capex figure below)

The economic moat of newspaper publishing is similar to that of postal in the sense that the same fixed assets where well maintain can be use for a prolong period of time.

But we should expect capital replacements once in a while as in 2001 and 2002 there is roughly 250 mil of capital expenditure.

In recent times majority of SPH’s assets were held in Treasury and Investments + Property.

Property assets stayed around 1 bil for long periods until the recent move to property development and purchase of Clementi Mall for rental result in a 50% growth in assets.

As illustrated, SPH capex have been low (less than 100 mil!) until the recent purchase of Clementi Mall which almost jacks up 600%

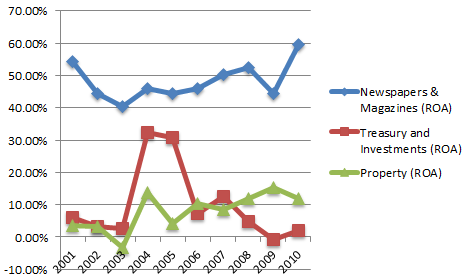

Segmental Return on Assets

How we was each segment performing over the years. I deliberately took out TV Media and Advertising because other than 2001 its been bleeding badly. It would skew the segments we should focus on which is Newspapers & Magazines, Treasury and Investments and Property.

Newspapers & Magazines have enjoyed a high return on assets as assets wasn’t climbing and population of Singapore have been increasing by foreigners. Notice that there was 2 periods of dip and are all related to recessions (2001-2003 and 2008-2009).

The impact of recession to advertising cannot be discounted. It is where the other recurring income offsets this.

Treasury and Investments performed really well in 2003-2005 there after returns have been very very low in recent times.

The up and coming segment have been in property, both rental and sale. On an average the return on assets is around 10%. Note that Clementi Mall’s contribution is not in.

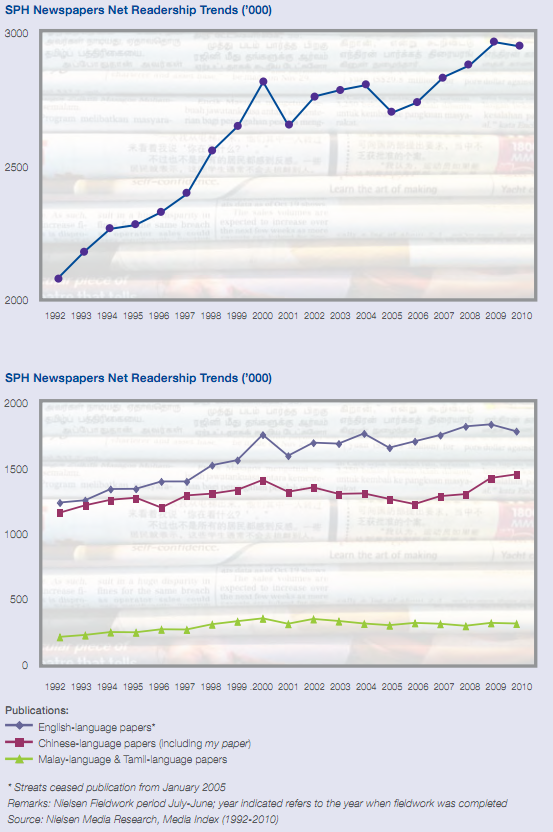

Newspaper readership have been increasing until 2010 where we see some stagnation. Back to the point of how new media impacts newspaper readership. We see clearly that readership trends might be falling off. 2010 might be a one off but I have a strong feeling it will continue.

English news readership is having a bigger impact from the smartphone trends and news alternatives competition compare to Chinese. Chinese readership increases is likely due to the influx of Chinese workers.

However, compare to segmental profits from Newspapers and Magazines, each drop in readership or increase in readership does not directly means net profit is affected.

We a dip in overall readership in 2004-2005 and 2009-2010 but profits have grew stronger in this 2 periods. I have no logically explanation from this.

I would say there are more factors in play such as cost expense that matters as well.

Conclusion

I would like to end off my re-look into SPH by saying that I am wrong about its cash flow in the past. It definitely has a positive free cash flow and it was my mistake to mis-interpret it.

Sustainability of their 400 mil dividend payout will depend on

- A shift towards greater distribution channels, more cross distribution.

- A focus on high quality content that is relevant to readers

- Acquisition of major content distributors.

- Maintaining their advertising profits.

- Increasing alternative recurring income sources. (Property)

400 mil is currently safely paid by an average of 300 mil in Newspaper and Magazines + 200 mil in Property and Investments.

To be safe the alternative recurring income source should build up to contribute more to the stability of the dividend.

Going forward the rise in assets from Treasury Investments + Property increases from 2.5 bil to 3.5 bil. That is a 40% increase in assets. A conservative estimate of 8% returns on this 1 bil will bring about an increase profit of 80 mil.

An alternative recurring income from properties and investments of 280 mil (200 +80) should largely cushion any fluctuations in Newspaper and Magazines. We could even anticipate a larger dividend payout.

I run a free Singapore Dividend Stock Tracker . It contains Singapore’s top dividend stocks both blue chip and high yield stock that are great for high yield investing. Do follow myDividend Stock Tracker which is updated nightly here.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Lion

Monday 11th of February 2013

I had hold on for SPH for pass 8years, good business on their Clelmenti Mall purhcase, if you go to the mall u will get what i mean

Reply to Comment by Vintire, how can Yellow page compare to SPH,whichSPHholding 1.5 bCash on hand

Cheers

Drizzt

Monday 11th of February 2013

i think a lot beg to differ whether its a good business because of deteorating fundamentals. this used to pay a much higher dividend. regarding cash, when did it have so much cash? last i checked its leveraged already.

Clementi mall was bought at a premium, and there is a upper bound to how much rents they can raise. the downsides seems higher.

juno tay

Wednesday 23rd of March 2011

Hi Drizzt!

Thanks for your illuminating article. SPH was one of my investment ideas but I eventually gave it a miss because of their increasing exposure to the property market in recent years.

Predictability is a big portion of my investment strategy. I am pretty sure that SPH publishing/online business will continue to thrive as long as it maintains its monopoly. Not too optimistic about the property acquisition's.

Nonetheless, I enjoyed your article!

Drizzt

Thursday 24th of March 2011

hi juno, i wrote this article because i wanna review it to see if i was bias about it. come to think of it i realise you werent wrong too much as Clementi Mall might end up being a dud. I have posted some questions to the investor relations so lets see how they respond. cheers

Vintire

Wednesday 23rd of March 2011

SPH seems to be trying to diversify its business...first media now reits...they seem to be neglecting their online section like online database and searches...and giving other companies like Yellow Pages a some leeway to manoveur...I wonder if Yellow pages a direct rival of SPH....

Drizzt

Thursday 24th of March 2011

hi Vintire, i don't think they are neglecting it. the key to the game is that there is no one strategy for this, no one channel to concentrate.

they have to provide a niche advertising strategy for their customers. Say if you want to spread the news that you have a "new tablet product like Galaxy" for the most bang for buck advertising with them through newspaper, presence on Asia One and Magazine give the highest success rate for the cost given.

grab the eyeballs then people will advertise with you.

Temperament

Wednesday 23rd of March 2011

Don't forget SPH is very, very important to the "PAPAYA". Of course everyone knows why. He who rules the "News" of the country rules the country. Many former "PAPAYA,s" elites are there.

Drizzt

Wednesday 23rd of March 2011

whether it is important to PAPAYA or not if it does not sustain a good cashflow its still a bad piece of investment

nitenite

Wednesday 23rd of March 2011

"We a dip in overall readership in 2004-2005 and 2009-2010 but profits have grew stronger in this 2 periods. I have no logically explanation from this."

On the above, is it due to the increase in price of the papers/magazines?

Drizzt

Wednesday 23rd of March 2011

hi nite nite not sure about that, but i doubt it will make that big of a difference.