Kudos to Lloyd’s Investment for giving novice investors like us this concise essay on how one can build a nested eggs through attainable means. We have read alot of articles about compounding and investing in equity, but this article throughly put all of it together.

In our capitalist culture everyone wants to grow wealthy–to retire early, to feel more financially secure, or just to join society’s upper echelon as measured by net worth. However, if you are like most people, you have a hard time getting started on the road to riches and an even harder time sticking on course.

Over the upcoming month, I will present an easy-to-follow plan that anyone with financial discipline can follow “in their spare time.” It is a passive investing strategy, designed to complement your primary source of income from your “real job.” Simply put, passive investing–when properly executed–can be highly rewarding. The approach I describe is, in my opinion, the best way to maximize net worth, while concurrently pursuing a satisfying career and favorite hobbies and spending quality time with friends and family.

The plan itself is really a “no brainer,” so much so that you’ll probably feel as if you’ve previously heard much of what I am going to say. If you are fortunate enough already to have a net worth exceeding a million dollars, this discussion is not intended for you (though if you continue reading, you might run across some of the same thinking that got you to where you are today). On the other hand, if you are a member of the overwhelming majority–the 90% of all American households who are not yet millionaires–I encourage you to read on. (For a summary of the wealth distribution among American households, see this table in an earlier post here.)

From the outset, I emphasize that this is NOT a “get rich quick” scheme. It will not make you into a millionaire overnight. It will not allow you to retire tomorrow. It does not promise spectacular 1000% and higher annual returns. It is not a magic formula for creating “something from nothing,” implementing “no money down” methods, leveraging “other people’s money” or deluding yourself into similar wishful thinking. Nor does it promise to turn you into the next Bill Gates, Warren Buffett or Sheldon Adelson.

Instead, my recommended plan is a slower-paced, highly practical approach to growing wealthy in the most predictable manner possible. It offers an eminently feasible way to start from zero net worth and become a millionaire within the foreseeable future, within your own lifetime and conceivably even within the next 15 years (by the year 2022). I will explain how to take a measured approach to risk and sidestep the “poor house” in the process.

Here are the basic steps of the plan, just five in total:

- Save at least $1,000 a month

- Set realistic return expectations

- Invest in equities

- Minimize fees, expenses and taxes

- Stay on course

I will cover the first point today and take up one additional point each week for the following four weeks.

Starting with a Savings “Seed”

“You gotta have money to make money,” said a college classmate of mine, citing a rich uncle or other such role model. Having marched through school and a successful career over the past few decades, and now hovering post-career and pre-retirement, I have had the opportunity to see and experience first-hand how making money works in real life. Personally, I know many colleagues who have accumulated enough of a “nest egg” in a couple of decades of employment, enough so that they are now able to live off of their savings and investments, and no longer “need” to work (even though many choose to continue working).

Now, there are two sides to saving:

a) Income side: Working to earn money, and

b) Expense side: Exercising fiscal discipline by living within one’s means.

Of course, as everyone knows, savings are the result of managing your personal finances so that your income exceeds your expenses.

I recall my later college years in graduate school in the 1980s when I worked as a teaching assistant earning about $5,000 a year (along with a tuition waiver), which allowed me to pay about $200 in monthly rent for a small room in a group house, cover food and miscellaneous expenses (books, an occasional movie, etc.), and still save over a thousand dollars a year. Upon graduation, when I took a job in New York City, my rent rose more than four-fold to $900 a month, but my salary more than compensated for the increase in my cost of living, enabling me to save a sizeable chunk of my earnings. Surely, both as a student and in the early part of my working career, I could have lived in more luxurious accommodations and pursued a more extravagant lifestyle, but I chose not to. Deliberately, I decided to live within my means, adjusting my lifestyle to make sure that I could save at least 10% to 20% of my income.

Just as acquiring wealth begins with fiscal discipline, which is really a mental and emotional balancing act between needs and wants, in many ways “being wealthy” is also a mindset. People who live paycheck-to-paycheck without saving any money are not wealthy, regardless of how much they earn. Conversely, people who are able to put aside a portion of what they earn, however modest their salary may be, either are “wealthy” (in the sense that they are able to buy more than they need, but choose not to spend all that they earn) or at least have a reasonable chance of one day becoming wealthy (as measured more traditionally by net worth).

One’s first objective on the road to wealth, then, should be to start saving, which really means educating or training yourself to work a job that generates sufficient income to support your lifestyle and allows you to save a significant portion of each paycheck. Often, it can also boil down to focussing on the expense side by moderating your lifestyle so that at least 10% to 20% of your take-home pay accumulates in your bank account rather than disappearing as discretionary spending (ever consider that maybe you really don’t need your jolt of caffiene from Starbucks today?).

Putting savings into a global context, it is interesting to compare the U.S. to other countries in terms of propensity to save. The bar graph below shows results of an ACNielsen survey polling respondents in various countries on how they use their “spare cash.” As might be expected, given that the “average American” has a savings rate close to zero, the U.S. has a very low propensity to save. In the results of this survey, the U.S. ranks towards the bottom of the list way down in 33rd place among 38 nations. The countries with the highest propensity to save are all in Asia: India, Taiwan, Singapore, Indonesia, Philippines, Hong Kong, China, Malaysia, Thailand, Japan. Although now is not the time to go into specifics, my guess is that there is a fairly high correlation between savings rate and GDP. Suffice it to say that a regular savings plan is a good starting point for anyone who wishes to boost their “personal cumulative net GDP” (i.e., net worth).

For the purposes of our discussion, let’s assume that any American seriously interested in building wealth is able to save $1,000 each month, for without this prerequisite savings “seed” it is truly difficult to build significant wealth. So, here I am not referring to someone working an unskilled labor job (e.g., flipping burgers at McDonald’s full-time) and earning a minimum wage of $10 per hour, or $1,700 a month (about $20,000 a year), since admittedly living on just $500 a month after taxes (in order to save $1,000 a month) would be quite challenging. Our discussion does, however, encompass this same proverbial fast-food worker who has sufficient motivation and foresight to enter a local community college and begin training himself for an entry-level position paying $20 per hour, or $3,400 a month (about $41,000 a year). At this higher income level, saving $1,000 a month, or about one-third of one’s take-home pay, becomes a very realistic proposition, since it is possible for individuals and even small families to live on $2,000 a month in most cities by being frugal consumers, i.e., choosing housing, food and transportation carefully and eliminating unnecessary expenses. For anyone completing a four-year college or obtaining a higher degree, earning more than $20 per hour becomes increasingly likely, making saving more than $1,000 a month not just possible but almost expected. . . .

For the moment, my advice on what to do with your $1,000 a month savings “seed” is literally to put it in the bank. Currently, with the yield curve “inverted” (i.e., short-term interest rates higher than long-term rates), many banks are offering savings accounts with very attractive interest rates of around 5% per annum. These accounts are FDIC-insured, offer full liquidity, have no effective minimum balance, and carry no monthly fees. A few examples I am familiar with are the online savings and free checking packages offered by Citibank and Washington Mutual, and a stand-alone savings account offered by E*TRADE Bank. Other banking alternatives are listed at Bankrate.com. You might also wish to check the ads in the business section of your local newspaper for any attractive offers.

What Investment Return Should We Target? (Part 2 of a five-part series)

Being successful in passive wealth generation involves setting realistic targets that are consistent with inherent market risk. You might want to become a millionaire, centi-millionaire or even join the rarified ranks of the world’s billionaires, but if you try to get there too hastily, you’ll in all likelihood never even reach your first financial milepost.

Get Rich Quick?

We’ve all received “invitations” (translation: advertisements) complete with “complimentary VIP tickets” to attend “once-in-a-lifetime financial conferences” that promise to teach the “secrets” of how to “buy real estate at 40% to 60% below fair market value,” earn 1000% and higher annual returns buying and selling stock options, or retire in a couple of years with additional cash flow of $9,000 per month. Such get-rich-quick schemes are tantalizing for the ambitious novice investor. However, since I have never run across anyone who has succeeded in making money through these programs, I am skeptical. I tend to believe that the schemes generally turn out to be losing propositions for those gullible enough to pay thousands of dollars in seminar fees to fast-talking finanacial “coaches” offering hope but ultimately little more than what amounts to an express route to the poorhouse.

At iamfacingforeclosure.com you can follow the latest developments in a timely and well-publicized case in point, about a guy who paid to attend a few real estate seminars and attempted to implement the “no money down” techniques he heard about. Unfortunately, instead of getting rich, he ended up losing substantially more than he invested. In his own words, “I made some mistakes and fell flat on my face with millions in debt and [am now] facing foreclosure.” In fact, the poor chap’s financial circumstances have become so dire that he is also considering bankruptcy. Obviously, this is hardly a pleasant outcome for someone so energetic and driven as he appears to be.

(By the way, if anyone reading this knows of a wealth generation program that actually does consistently achieve returns in excess of, say, 20% per annum, I would be very pleased if you could share information about the program and provide a detailed investment track record for everyone’s perusal.)

Rather than greedily go “elephant hunting” for enormous returns using unproven wealth generation techniques whose effectiveness is, at best, very difficult to verify, I recommend following a more predictable course to which we now turn.

Historical Market Returns

Let’s look at the historical record to get a feel for what type of investment returns are possible across commonly accessible financial markets. The bar graph below shows the annual performance of cash, bonds, stocks and real estate over the 15-year period from 1992 through 2006, based on historical market data from Global Financial Data and the Office of Federal Housing Enterprise Oversight.

- Cash: Money market accounts, bank CDs and Treasury bills offer comparable rates for holding cash. The 3-month Treasury bill averaged a 4% annual yield over the 15-year period.

- Bonds: The 10-year Treasury bond showed a 5% average yield. Bond returns vary with changes in interest rates; however, over long holding periods, yield becomes a good proxy for approximating annual investment return for bonds.

- U.S. Stocks: The S&P 500 stock index has given a 10% average annual return over 15 years, with annual performance ranging from -23% in the worst year (2002) to +34% in the best year (1995).

- Foreign Stocks: U.K. stocks (FTSE) averaged an 8% annual return (U.S. dollar-based), similar to the performance of the U.S. stock market during the same period. Impacted by a lengthy recession during the 1990s, Japanese stocks (Nikkei 225) averaged just a 2% annual return (U.S. dollar-based) with considerable volatility, returning -35% in the worst year (2000) following a +51% rise in the best year (1999).

- U.S. Real Estate: The median value of single-family homes sold across the U.S. has appreciated 6% on average over the past 15 years, including the annual double-digit gains during the recent real estate boom that now appears to have ended.

Gold, other commodities, options and futures, collectibles, etc., are also possible investment vehicles. However, broadly speaking, these alternative investments tend to offer average multi-year returns similar in magnitude to the equity-related (i.e., stocks and real estate) returns discussed above.

Targeting Realistic Returns

For passive wealth generation, what then is an appropriate target to set for annual investment returns?

Even though the past 15 years are not necessarily a reliable indicator of the financial market performance that will actually transpire over the upcoming 15 years, we can use the historical record to help set reasonable expectations for the future. First of all, if, among the three stock markets (U.S., U.K. and Japanese) surveyed above for the 15-year period 1992-2006, the best year in the best market produced a 51% return, it is clearly unreasonable to expect to achieve in any consistent way returns higher than this level. In particular, a rational investor should be highly skeptical when hearing anyone claim to have a scheme that can consistently achieve anything like the 1000% returns touted by certain get-rich-quick seminars.

Next, we must decide the extent of risk we are comfortable taking on to achieve higher investment returns. A conservative, risk-averse investor will want to allocate assets primarily to bonds and cash, which can be expected to produce 3% to 6% annual returns. Investors seeking higher returns will want to weight their investment portfolios more heavily towards equities. In fact, given that equities have historically outperformed bonds and cash, I would recommend that anyone with a long-term investment horizon should seriously consider owning as close as possible to 100% equities, allocating only a minimal amount of one’s portfolio to cash for liquidity purposes.

Given that the S&P 500 has averaged about a 10% return over the past 15 years, it is reasonable to target similar returns for an equity-based investment program over the next 15 years. Specifically, here’s what I recommend:

Look for investments that can produce 20% annual returns, while realistically expecting 10% average annual returns and understanding that somewhat lower 5% average annual returns might actually result.

In my opinion, anyone “reaching out” for annual returns substantially higher than 20% is speculating more than investing. Of course, speculators do occasionally hit the jackpot, but the hard truth of the matter is: people who choose to speculate rather than invest are generally setting themselves up for predictable financial failure rather than measured financial success.

Investing in Equities (Part 3 of a five-part series)

Working with your savings of $1,000 per month and a realistic targeted investment return, your next job is to identify the appropriate investment vehicles to begin your multi-year process of passive wealth generation.

What Drives Equities Higher?

We have seen how over the past 15 years stocks (and real estate) have outperformed bonds and cash. This tendency of equities to beat fixed-income instruments over the long haul is a familiar pattern. As discussed in this blog a couple of years ago, the historical record shows that stocks have generally outperformed bonds across international markets from as far back as the data go (i.e., from the late 1800s to the present). For anyone interested, see books such as Jeremy Siegel’s Stocks for the Long Run and Elroy Dimson’s Triumph of the Optimists, both published in 2002, for informative background reading on the topic.

Despite the historical evidence in favor of equities, it is also important not to assume blindly that the recent 15-, 25-, 50- or 100-year period will necessarily repeat itself. To quote Dimson, et al, from a paper titled “Irrational Optimism” (2003):

Although the probable rewards from equity investment are attractive, stocks did not and cannot offer a guaranteed [italics added] superior performance over the investment horizon of most investors. Furthermore, their prospective returns are lower than many investors project, whereas their risk is higher than many investors appreciate. Investors who assume that favorable equity returns can be relied on in the long term or that stocks are safe so long as they are held for 20 years are optimists. Their optimism is irrational.

It is important, then, to keep our optimism in check, noting that, while the outperformance of equities over bonds and cash in the 15-year horizon we are considering is arguably likely, it is by no means a certainty.

To add perspective to the quantitative analysis cited above, I now give a qualitative argument for why equities ought to continue to outperform bonds and cash: Our economy is fueled by investor greed but steered by government policy. Entrepreneurs and investors, driven by their “profit motive,” expend their time, effort and capital to develop technology and build companies that produce consumer goods and services. The government, presently under the direction of Fed chief Ben Bernanke, targets a narrow band of moderate inflation (about 3% to 4% per annum) by periodically adjusting short-term borrowing rates higher or lower to control the availability of capital in the financial system and, in so doing, manages (to the extent possible) the overall rate of corporate expansion and economic growth.

The two key elements in this mechanism are: a) government-mandated inflation, and b) technological innovation. With 3% to 4% inflation in consumer prices, the revenue of the companies producing the goods and services that consumers buy naturally rises. The “cost” side of the income statement is also impacted by moderate inflation; however, increasing efficiency from improvements in technology keeps expenses in check, allowing profits (i.e., revenue minus expenses) to rise at a rate significantly higher than inflation. Rising corporate profits, in turn, drive stock prices higher–at a rate of appreciation higher than the inflation rate. Through substitition effects, the value of other equity-based assets (real estate, collectibles, commodities, etc.) likewise rises.

Regarding technology, a solid argument can be made that innovation and corresponding equity returns are not just increasing but are actually accelerating (e.g., see the discusssion of Ray Kurzweil’s so-called “law of accererating returns” in a prior post). In short, the combination of government-mandated inflation and efficiencies brought about by technology gives us good reason to expect that equity returns will continue to exceed bond returns over the decades ahead.

Common Equity Investments

I use the term “equities” to include stocks and real estate. Three broad equity asset classes available to us as passive investors are:

- U.S. Stocks: Investors can buy individual stocks (e.g., Exxon (XOM), GE (GE), Wal-Mart (WMT)), stock mutual funds (actively managed by “stock-picking” fund managers), and index or exchange-traded funds (ETFs, which track market indices instead of attempting to pick the highest-performing stocks). A tremendous variety of stocks and stock funds is available to suit the gamut of investing styles and preferences: large-cap, mid-cap, small-cap, value, growth, income-oriented, sector-specific, geographically oriented, etc.

- Foreign Stocks: A good selection of large-cap (and to a lesser degree, mid-cap and small-cap) foreign stocks is available as ADRs (e.g., Petrochina (PTR), Toyota (TM), Vodafone (VOD)). As with U.S. stocks, exposure to foreign stocks is also available through mutual funds and ETFs.

- U.S. Real Estate: Many homeowners consider their own home (and any vacation home they may have) to be investments. Single-family rentals, multi-plexes and larger apartment complexes are more typical residential real estate investments. Commercial properties (office buildings, retail centers, mixed-use developments, etc.) are common investments for individuals, partnerships and LLCs seeking direct exposure to the real estate market. Publicly listed and traded real estate investment trusts (REITs) offer individual investors an indirect but “hassle-free” way to invest small amounts of capital into the real estate market.

Hedge funds and private equity funds are also available to individual investors but these investments tend to cater to those who already have a net worth in the millions.

Basic Considerations In Selecting Equities

Determining the most promising investments from this wide range of investment alternatives can be a bewildering experience. A few very basic guidelines, however, should help narrow the field considerably:

- Suitability: Know thyself. It is important to select investments that are a good match with your interests and personality, since doing so will give you an “edge” over the average investor in the same securities or properties. If you naturally follow the news about a particular industry, it is more likely that you will be a better judge of which companies have more competitive products and will be able to generate higher long-term profit growth. If you tend to follow general market trends but do not pay close attention to particular companies, ETFs may be a better investment vehicle for you than individual stocks. “Hands-on” investors who enjoy negotiating with buyers and sellers and engaging in property management may wish to invest directly in real estate properties.

- Simplicity: Keep it simple. Given two investment alternatives that you view as comparable from a risk-reward perspective, always choose the one that is easier to analyze and understand, involves less paperwork, and is generally less time-consuming to manage. Personally, I prefer stocks over real estate because stocks are simpler to buy, sell and own. However, there are certainly times when knowledge about a local real estate situation can lead to an opportunity that is “too good to pass up,” thereby justifying the additional administrative time needed to work with brokers, banks, escrow companies, inspectors and property managers to close a deal. I believe that success in investing comes largely from “buying right,” and consequently recommend focussing on the investment decision (i.e., deciding what to buy) instead of overtrading your portfolio.

- “Lumpiness”: Limit diversification. Owning few good investments is generally better than trying to keep track of a large number of holdings that inevitably include losers along with winners. I find that a “lumpy” portfolio of just 10 to 20 different stocks and real estate properties gives me adequate diversification, while allowing me to feel the impact of the individual investments on overall portfolio performance. To profit from the higher GDP growth offered by economies outside the U.S., it is important to have international exposure, which generally comes from owning ADRs, international mutual funds or ETFs. Investors with a global mindset should consider weighting exposure to major international markets along the lines of GDP (see graph below). Note that, while the U.S. has the world’s largest economy, it comprises just 28% of the world’s total GDP.

- Quality: Buy quality. When considering what to buy, do your own due diligence to make sure that the companies underlying the stocks you buy have strong businesses and are likely to thrive and remain leaders in their particular market niches over the next 10 to 15 years. If you are buying mutual funds, pay attention to who is managing the fund, inspecting both their qualifications and their track record. When buying real estate, keep in mind that properties in better neighborhoods generally show more predictable returns and tend to be less time-intensive to manage.

- Efficiency: Strive for high efficiency. Portfolios built on longer investment horizons are usually more efficient. Benefits of lower portfolio turnover are deferral of capital gains taxes (or use a 1031 exchange for investment real estate), minimization of trading costs, and reduction of administrative time spent executing and accounting for transactions. When investing in mutual funds, select a quality fund with low advisory fees. Keep in mind that round-trip fees can be very high in less liquid markets. For example, real estate deals typically involve round-trip fees and costs in the vicinity of 5% to 8% of property price, which translates into 10% to 16% of equity amount for 50% leverage, and 25% to 40% (wow!–that’s astronomically high compared to stock commissions) of equity amount for 80% loan-to-value–which is why it is so difficult to make money quickly by “flipping” properties.

By adhering to these basic guidelines, most investors will end up investing most of their savings in highly liquid, mid- to large-cap stocks and ETFs, with some allocation to local real estate. I would recommend using the following “model” portfolio as a starting point for asset allocation:

- Individual stocks (can include REITs): 40% to 60%

- ETFs (or mutual funds): 10% to 30%

- Real estate (including own home): 10% to 30%

- Cash, CDs: 5% to 15%

For my own portfolio, I am heavily weighted in individual stocks and very light on cash, with a modest amount of real estate and little to no allocation to mutual funds and ETFs.

Why Controlling Fees and Expenses Matters (Part 4 of a five-part series)

Running an efficient portfolio is the easiest way to “stack the cards” in your favor to achieve long-term investing success. Let’s begin by way of analogy–with a trip to the supermarket.

How Do You Shop for Your Groceries?

You might have heard that Ben Graham recommended investors buy stocks like they buy their groceries (and not as if they are splurging on perfume). Well, over the year-end holidays my wife and I happened to receive as a gift a 1000-page coupon book for 2007. Though I don’t much enjoy clipping coupons, I was curious enough to find out if the book really is worth its $40 retail value and began to page through it. One of the most useful discounts in the book is a set of four “$5 off” Safeway (SWY) coupons, one for each season of the year, valid when purchasing $50 or more of groceries. Because my wife (who does most of our grocery shopping) was tied up last week, and since I wanted to make sure that we use the winter coupon before it expires later this month, I decided to make a run to Safeway myself.

With the weekly Safeway ad in hand, I strolled into our local store, grabbed a cart and started down the aisle. Since oranges were on sale for just $0.33 a pound (an amazingly low price, particularly in light of the recent news of an estimated $1 billion of frost damage to crops in California), I loaded up on 20 pounds’ worth. Noticing broccoli and cauliflower at $1 a pound (a good price for the winter season), I bagged a few pounds of each. Continuing on to the meat section, I found the chicken breasts advertised at $0.99 a pound (regularly $1.99 a pound) and the London broil steaks at $1.99 a pound (normally $4.79 a pound) and selected a couple of packages of each. In the bakery section, New York-style bagels were on special (three for $1); so I picked up a dozen. The French bread, hot and right out of the oven, was on sale for $0.99 a loaf (regularly $1.39) and smelled too good to pass up; so I tossed a couple of loaves into my cart. Then came the laundry detergent, toilet paper, toothpaste, tortillas, milk, cookies and ice cream–all on sale–to top off my shopping cart.

When the cashier rang up my total, it initially came to $115. Then, miraculously (listen up–this the important part), after I slid my Safeway club card through the reader and handed the “$5 off” coupon to the cashier, my total dropped precipitously to, not $100, nor $90, nor even $80, but all the way down to . . . $55! Amazing! A 52% discount, just from selecting sale items, showing my Safeway card and using a discount coupon. And, guess what? I even got a bonus: because I spent more than $50 in a single purchase, the next time my wife or I fill up with gas at the Safeway pump, we get 10 cents off per gallon, which will save us another buck or two.

That’s how I shop for my groceries–paying attention to what’s on sale and taking advantage of discounts that come my way. Really, it takes very little extra time and effort to realize significant savings in a most predictable way.

The Control Factor

Moreso than the absolute dollar amount of savings on groceries, the important point here is what I like to call the “control factor,” i.e., taking advantage of elements that are within your sphere of control. In the context of investing and maximizing net worth: when you have the opportunity to improve your returns by exercising a little more care in how you go about managing your personal finances, you should!

We can also see this principle at work in Ben Franklin’s advice, “A penny saved is a penny earned,” in Warren Buffett’s willingness to stoop down low to pick up a penny in the elevator even though he’s already a multi-billionaire, and in the secret to riches as reported in Thomas Stanley and William Danko’s The Millionaire Next Door. Essentially, controlling the parts of your personal income statement that you can–whether part of earnings, savings or expenses–is vitally important to wealth-building.

The nature of markets is that so many factors are beyond our control. We do not know with much certainty if the particular stocks we own will rise or fall tomorrow, whether interest rates will head up or down next month, which way oil and gold prices are headed, or if the dollar will strengthen or weaken next year. All of this uncertainty creates the “volatility” that investors worry about but shouldn’t. My point is that, instead of spending the time worrying about the big “macro” factors you cannot control, you should focus on the more manageable, comparatively small items that you can control. Learning to take advantage of the opportunities offered by what is within your grasp is often what makes the difference between winning and losing in investing.

Low-Cost Investing

Let’s now consider an example from long-term investing. You’ve probably heard of John Bogle, the Vanguard founder, who is adamant about the advantages of index funds over actively managed mutual funds. In a recent speech, Bogle provided results of a study indicating how actively managed mutual funds with higher expenses and turnover have grossly underperformed those funds with lower expenses over the decade 1995-2005. As shown in the table below, the performance differential between the low-cost and high-cost quartiles over this ten-year period is a striking 75 percentage points (207% for the low-cost quartile vs. 118% for the high-cost quartile). Clearly, anyone would be happier seeing their $1000 grow to $3070, instead of the lesser figure of $2180, over a ten-year period. This is the low-cost advantage.

Bogle concludes that “Yes, costs matter.” He also goes further to advise: “So do your best to minimize your investment expenses and your own emotions, rely on your own common sense, be very careful, and then stay the course.” I agree wholeheartedly.

Efficient Investing Habits

In the broader context of personal portfolio management, here’s what I recommend:

- Self-Reliance: Cultivate an open-minded, do-it-yourself attitude. I have found that keeping my investment portfolio simple allows me by and large to avoid calling on expensive experts (accountants, lawyers, financial advisors). If and when you do hire professionals, make sure that they are delivering value to you that more than offsets what they are charging you for their services.

- Minimize Fees and Expenses: If you enjoy the challenge (like I do) of picking your own stocks and properties to invest in, by all means go ahead and do so!–since this way you keep your out-of-pocket portfolio management expenses to a bare minimum. If you are not comfortable or just do not want to spend the time picking your own stocks, do the next best thing–buy index funds to keep fees and expenses low. Avoid actively managed mutual funds, unless you are convinced that the fund manager has a superb track record that is likely to continue. Note that even the fund managers with the best performance records, such as Bill Miller of Legg Mason’s Value Trust whose 15-year streak of beating the S&P 500 ended last year, can and do have bad years.

- Low Turnover and Taxes: Keep portfolio turnover as low as possible. I like to target 10% turnover per year, consistent with a 10-year horizon. Before buying any stock or real estate property, make sure that it is an investment you can expect to hold for the next decade. Low turnover saves on commisions and bid-offer costs that degrade returns. It also means lower taxes from tax-deferred compounding of embedded gains, since capital gains taxes are due only at time of sale.

- Don’t Worry About What You Can’t Control: While it may seem counter-intuitive, you should care more about the $100 you can easily save, than the $10,000 swings in the value of your portfolio that you have no control over. Over the long haul, the small $1, $10 and $100 savings have a way of adding up to increase your odds of outperforming the market, while the large $1,000 and $10,000 drops in portfolio value due to market volatility tend to get more than offset by positive moves (recall that equity markets tend to rise over time).

To sum up, you can and should take advantage of the controllable, easy-to-find discounts and “freebies” that enhance your chances of being successful long-term as an investor. Work on what you can control–let the secular upward drift of the market take care of the rest.

Perseverance in Long-Run Investing (last of a five-part series)

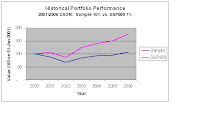

Figure caption: Example of “beating the market.” Sample portfolio with 10% CAGR over 6 years (2001-2006), versus S&P 500 with 1.2% CAGR over the same period. Sample portfolio goes from $100 at the beginning of 2001 to $177 at the end of 2006, versus $108 for S&P 500.

If you’ve been following along from the beginning of this series, you are now (at least hypothetically):

- working and saving at least $1,000 each month,

- setting a realistic return target of up to 20% per annum,

- investing primarily in equities, and

- keeping your expenses low.

Today we’ll put everything together and take a look at a few scenarios to see how long it will take to reach the $1 million goal I mentioned at the outset.

Wealth-Building Scenarios

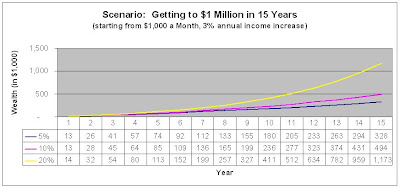

How fast does your savings of $1,000 per month grow when diligently invested each and every month for the next 15 years? To run realistic scenarios, I assume that the “seed” amount you are able to save grows at a moderate inflation rate of 3% per year, meaning that this year you save 12 x $1,000 = $12,000; next year (in 2008) you save 3% more, or $12,360; the following year (in 2009) you save 3% more than that, or $12,730; and so on. As you save this money, you invest it primarily in equities (stocks and real estate) each year.

Although your return-on-investment (ROI) will vary from year to year, in accordance with the volatility of the market, for calculation purposes let’s see where you will end up 15 years from now (in 2022) if you are able to achieve certain benchmark rates of return on your monthly savings (starting this year at $1,000 per month). Here’s how the numbers look:

- 5% annual return-on-investment (ROI): Reach $330,000 at 15 years;

- 10% ROI: Reach $500,000 at 15 years;

- 20% ROI: Reach $1.2 million at 15 years.

The graph and table below show the path your money follows as it grows over the 15-year investment period.

Certainly, if you are able to achieve a 20% ROI (which, by the way, would give you a stellar track record) in your investing, you will reach the zero-to-a-million-dollar goal by the end of 15 years. However, it is important to observe that you can also get to $1 million under the scenarios with a lower ROI (note: realistically speaking, these are the likely scenarios for most of us) by figuring out how to earn more from whatever work you do and (rather than spending your extra income) exercising the financial discipline to save and invest it. To reach $1 million in 15 years, here’s what it takes:

- At 5% ROI: Save and invest $3,000 per month;

- At 10% ROI: Save and invest $2,000 per month;

- At 20% ROI: Save and invest $1,000 per month.

Safety and Hope

For my own portfolio I like to have a blend of value and growth stocks. The value stocks are typically low P/E shares of well-established companies, conservatively run, generally large-cap, some of which pay dividends, and all of which have what I consider to be fairly predictable revenue, earnings and cash flow streams. The predictability of the underlying fundamentals gives me a sense of safety, i.e., assurance that the enterprise is almost “too big to fail” and will still be around in 10 years’ time.

Examples of stocks in the value category are Citigroup (C, forward P/E of 11) and Berkshire Hathaway (BRKA or BRKB, forward P/E of 19), both of which I have held for over a decade. Another long-standing position is Equity Office Properties (EOP, forward P/FFO of 24), the REIT run by Sam Zell, which has become target of a private-equity bidding war between the Blackstone Group and another potential acquiror led by Vornado (VNO). (By the way, I also consider the house that I own and live in to be a value-oriented investment, since it is located in a fully built-out, stable neighborhood with decent long-term appreciation potential.)

Investing (and life) would be psychologically boring without the growth side, which complements the “safety” of the value side by introducing the more exciting element of “hope.” The nature of growth stocks is higher P/Es, higher volatility, greater potential upside, typically no dividends, and younger underlying businesses with faster growth, often in the technology area.

An example of a growth stock in my portfolio is eBay (EBAY, forward P/E of 21), which I have held since shortly after its IPO in the late 1990s. I have also recently added Baidu (BIDU, forward P/E of 70), the Internet search leader in China, and Netease (NTES, forward P/E of 19), the leading Chinese gaming company with a horizontal portal, both of which I discussed in an earlier post covering Chinese Internet stocks.

In choosing your own portfolio, you will, of course, generally end up with a different selection of stocks (and ETFs, real estate and possibly mutual funds) than I have. However, regardless of the particular investments you select, I strongly recommend investing in a blend of value and growth, small cap and large cap, dividend-paying and not, domestic and foreign, tech and non-tech, young and old companies, etc. Once you seriously begin to run a “lumpy” portfolio with a few carefully selected stocks, you’ll be surprised at how much diversification is actually possible with a very limited number (as few as 10 or so) positions in the mix.

Staying in the Game

Having come to this far in our discussion, you might be wondering if the investing methodology I am recommending really works. Will it enable you to accumulate wealth, achieve significant returns over the next 15 years, have a good chance of beating market benchmarks, and ultimately achieve your net worth goals?

First, in principle, I see no reason why the approach shouldn’t deliver solid results, since the core assumptions behind the methodology are reasonable ones:

- Regular savings provides the steady flow of investment capital your portfolio needs;

- Setting realistic return targets helps to avoid “losing it all” through speculating;

- Equities should continue to outperform bonds and cash over the long run; and

- Minimizing expenses and fees enhances your chance of outperforming the market.

From a more practical perspective, I cannot offer conclusive, quantitative “proof” that the approach works, but I am willing to share my own experience to date. From 2001, when I began to manage my own money using the general “measured” approach outlined, I have kept track of my own performance. Somewhat to my own surprise (even though intellectually I am convinced that the approach “makes sense”), in each of the past six years I have managed to outperform the S&P 500, resulting in the sample portfolio return line displayed in the small figure at top of this article. Of course, as with any investing record, the future is what really counts and we will just have to wait and see if my outperformance continues in subsequent years.

A Monopoly board game analogy helps shed light on the nature of investment performance: Most people will agree that Monopoly is a game of both luck and skill–luck in rolling the dice and landing on the right properties at the right time (and skipping past other players’ properties), and skill in trading properties with other players and deciding how rapidly to deploy your cash to build houses and hotels. After playing the game a handful of times with my own children and winning most of the time, I have begun to appreciate the role that skill plays at crucial junctures in the game. Sure, there is a great deal of luck involved but what I have noticed is that the eventual outcome of the game often hinges on particular decisions made by individual players, e.g., how much to pay for a property that’s up for auction, or whether to prioritize obtaining all of the railroads for steady income or a complete color set of properties to begin building houses and hotels early in the game. In my opinion, the “investing game” that we all play in real life involves a luck-skill relationship much the same as in Monopoly–luck is important in short-term performance, but the many little skill-oriented decisions we make over the years soon enough add up to determine our long-run success as investors.

My closing advice:

Save whatever you can and invest it, pursuing the measured approach I’ve outlined. In both up and down markets, stay in the game and be patient. Persevere through good and bad years and, with a little luck, you’ll soon enough succeed in riding the market to the $1 million milepost and beyond.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

- The LionGlobal APAC Financials Dividend Plus ETF Won’t Give Singapore Investors 5% Dividend Yield Always. Further personal thoughts (with some data). - April 13, 2024

rokawa

Saturday 15th of October 2011

there's no need to diversify stocks. Pick n hold "good" stocks. No need to hold 10 or 20 stocks. the actual term for diversification is if u invest in stocks, then u if u wan to diversify it means u also invest in other asset class like commodities or real estate. When u buy company A B C D etc, u are still investing in paper assets which is not diversification. if buying dif companies is diversified, when market crash when panic selling happen, every stock will drop. how come your diversified portfolio of stock do not help to limit the loss? Coz they are all under the same asset class. if u had invest in gold, and stock amrket crash, gold price rise. then yur portfolio may suffer losses in stock market but your gold assets will help u make money.

Guest1

Sunday 1st of May 2011

in this article, you mentioned one should hold a little cash (if for long term investment). And you did hold a little cash. But, your current portfolio shows that you hold more than 50% cash. Can you enlighten me why you have a different strategy ? Thanks

Patrick

Wednesday 7th of January 2009

rnI know this article was from awhile ago, but thought I should comment on this comment above.rnnbsp;rnYes, saving accounts in some countries are good, i.e. Australia was giving out on average 6-7%p.a. on savings accounts with no strings attached like FD accounts etc.. most do have a smally monthly maintenance fee.rnnbsp;rnThe problem to this approach isrnnbsp;rn1. Are you able to open an account in the country of choice?rnnbsp;rnIf you have some way of getting yourself "outstation" to your country of choice, then perhaps you can meet their ID checks and open an account.rnnbsp;rn2. Risk of FX lossesrnnbsp;rnFor example, based on your comment made in 20, May. SGP -gt; AUD was about SGD1.2 to 1 AUD.rnnbsp;rnAssuming you had transferred $50k SGD into this saving account, as of today 7 Jan 09, you are in a negative position because of the large drop in AUD against SGD, even taking into account a 8%p.a interest given.rnnbsp;rn3. Lastly the hassles of moving this money, especially those in large amounts in and out of the country via TT etc..rnnbsp;rnI could be wrong, just my thoughts.

underaged investor

Monday 19th of May 2008

Why must I invest in S-Reits that offer abt 5% yield PA and expose my cash to so much risk when overseas banks in the US or Aussie offer much better Interest rates (Savings) without the risk in the stock market?

Singapore stockmarket

Monday 5th of May 2008

great site