I worked in the technical role in the IT industry for most part of my working career.

In the past, I can’t believe why we get some horrendous projects thrown to us. What is the back story there.

As I get more senior, my project manager started throwing me to coordinate more with the sales side of the business.

That is when I start to understand why things are so horrendous.

Why Projects Fxxk Up

A lot of the times, the project eventually take longer than expected to deliver.

This can be due to projects being more complex than imagined, staff that are task to carried out the work being incompetent, the project manager being incompetent.

However, a lot of projects got overrun because realistically the projects were under-priced, so that the bid is competitive.

If won, the budget to execute that project is severely limited, so that eventually the project can be estimated to earn a minimum profit margin that the big boss wants.

Under-price can mean a lot of things but I feel the most common is this: I promise you the world for that price, in the end the requirements are so much that we cannot deliver within the budget.

The sales person, the customer and the project manager in charge of delivering the project has a different view of things.

Most of the time the project manager tries hard (if he doesn’t quit first) to deliver something that won’t break down during user acceptance test.

The ones that are being left holding this are the user.

Bloggers Often Promise the World in Their Narratives

Is this problem prevalent in other fields? I think so.

In financial blogging, the issue of economic bias, what is communicated across to the readers, and the actual reality the readers experienced might have a lot of disconnect.

There was 2 interesting articles I read these past weeks that lead to this article:

The first article was written by Tanja at Our Next Life. She recently gain financial independence with her husband after both working in individual six figure annual income jobs that is not in the technical field. Before this, she couldn’t reveal her identity, but was able to after both of them left their job. I like Tanja’s blog because she writes well, explores a lot of the philosophical side of financial independence.

I also find it interesting that she separates herself from a lot of the other bloggers, who depended on the 4% withdrawal rate as the main bulk of their plan for financial independence.

She tries to plan out her cash flows in a very detail manner, listing out which account to draw down first, then follow by cash flow from the rental properties follow by tax deferred accounts and social security.

You can sense that she is more of a practitioner who wishes to ensure that her plan is sound, robust against a lot of scenarios.

In this article she calls out what seem to be a prevalent narrative among the FIRE bloggers. FIRE stands for financial independence retire early.

It basically refers to the people who aspires to have adequate wealth assets to be able to be financially independent AND take the plunge to retire early.

If you append bloggers to the end of it, that means that you write about your journey, you evangelize this way of wealth accumulation with this wealth goal in mind.

What are the stuff spoken that bugs her?

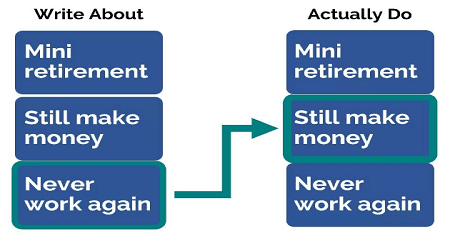

1. Marketing and Reality Mismatch in the ‘Product’ Sold. There are a few types of retirement possible and they can be save enough for mini retirement, semi retirement, and never worked again.

We could want different forms of retirement but the most prevalent sold by FIRE bloggers she encountered are those that sells the “Save enough to never work again”

The problem is that while they are allegedly selling this message, they are making income peddling this message. So if they reached financial independence, and they said they retire, yet they still receive income from the blogging, affiliates then isn’t that a bit hypocritical?

2. Ignoring the Reality of Many Readers. Tanja alleged that the FIRE bloggers didn’t realize that most of them earn above middle income salaries. In fact a lot of those that can realistically pursue this scheme of life are those that have annual household income in higher percentiles.

So when they sell that “anyone can do this” and if I may add “if you are not reaching this its because you are not earning more, or cutting down enough”, they are not acknowledging that there are economic realities that make these things difficult.

What Tanja wishes to see are more bloggers being upfront about:

- whether you are testing out your own plans

- what are the parameters of your own financial independence

- say you have a high income

- disclose whether you are working

- be clear about why you would go back to work

- explore more about your backup plans

- whether sharing partial numbers such as only sharing your savings percentage is useful to the readers at all

- be responsible and stay in touch with the technical aspects and the financial realities

The second article is written not by but on a couple in the FIRE blogging community.

The writer introduces the readers that a lady that goes by Mrs Frugalwoods on her blog, has written a book on how frugality was able to allow her and her husband to retire at 32 years old.

The writer does not buy in to the narrative that the main reason for them being financial independent is because they are frugal.

He cites evidence of them owning a home in the very expensive Cambridge Massachusetts, their 71% savings rate do not include the tax deferred account 401k, both earning six figure income. He points out that they are not the only one doing it, that there is a lady blogger who begin saving at 7 and have half of her university tuition fees covered by parents, and another blogger who dishes anti entitlement advice yet his personal income on his blog in January alone is US$155,000.

His conclusion is that by saying that all we need to do is to be more thoughtful with their money and things will be okay, we are sending a very dangerous message. The reality is that frugality is just a lifestyle enhancement for those that have higher income.

With that said, here are some of my thoughts.

Most Writers on the Subject have High Income

Tanja raised a good point that it gets to the point where a lot seem to lost touch with the reality.

I wouldn’t call myself a FIRE blogger but I do write extensively about personal finance, building wealth, financial independence and retirement.

And at times in my early phase of working career, as a single, I really lost touch of reality.

And there are some reasons (not necessary good ones)

Most writers on the FIRE subject got triggered because suddenly they realize their wealth assets could lead to FIRE in the near future.

Or that based on their net cash flow afforded by their higher income, they can reach there in a realistic manner.

There are those that do not have high income but just think this is a sensible way of living.

Thus when they start a blog chronicling their journey, they might get to a stage where they think this is applicable for all.

Of course its applicable for all if your peers are all earning good incomes.

Usually at work you mix with people on roughly the same income level. If you are an engineer earning higher than average income, you will think that since most of your peers are earning this way, that is the reality.

You get into contact with your NUS, NTU and SMU classmates and they are also earning around that range.

So that kind of income range became your reality. But that is not the reality for a group of people.

The people that would write a blog also tends to be folks that are more introspective about the things that they come into contact with.

They tend to live a life more of agency, and what leads up to this kind of agency life may likely be due to higher education, which tends to lead to above middle income earnings.

Do I think this is a problem?

We cannot change our experience with the FIRE content, we cannot change our higher income.

However, we can factor in the narrative that our higher income makes this path easier for ourselves.

The problem for a lot is that they don’t think their income is high (because all their peers is earning roughly the same!)

So that has been my experience as well.

I studied in NUS, and when I get to this current stage, almost all my peers are senior engineers, managers or high level engineers.

Its easy to think FIRE is possible, until you failed to realize the efficiency you enjoy as a single.

When you talk to more people, learn about their experiences then you realize not everyone is living the good stable path to wealth.

It is important Not to be Ambiguous about the Different Schemes of Wealth

Sometimes, you might say, “Kyith, why harp over these terminology? Isn’t all of our financial independence path different?”

It is different for you if you are not writing about it.

However, if you are sharing this experience, or introducing this way of life to people, people need to know how suitable and viable it is for them.

By not making things clear, you might have oversold or undersold something.

This is why Tanja said that the reality and the marketing can be totally different.

And many might only realize it when they get to a certain stage in their journey.

The reality is that full blown retirement is not easy.

You wish to feel utterly safe, you gotta bring down your initial wealth withdrawal rate to closer to 2-3% of your wealth assets. This will mean you need more money.

Usually, people need to balance between finding a certain level of wealth assets that gives them a reasonable retirement, yet develop another profession or business. You can’t vacation and play games all your life. Most people should retire to something and that becomes manageable.

So in reality, most of them lived a semi-retired life, or would aspire to be something like that.

Thus the marketing and what their audience is chasing could have a disconnect.

Your Perception of your Readiness or Comfort in Retirement Varies When you Have an Income Coming in

One blogging friend tells me, if you have an inheritance coming in, it will affect how much risk you would subject your current wealth assets to.

Entrepreneurs need to be able to bleed, and thus those who can bleed, and not worry about the future tend to be those with well off background. They are what my friend Christopher Ng thinks should be the ones who do more of these seeding.

If you do not have an inheritance, you tend to want to be freaking sure you are doing something fundamentally sound with your money, with a viable plan.

When you are making income writing about FIRE, you do not need to draw down on your wealth assets just yet. When you do not need to draw down on it, it can grow further (you avoid the negative sequence of return risk)

Of course you are more confident about your plan, you have less anxiety and can write with a more confident tone.

The readers reality is different.

When they are being sold this retire and not work again, they will get the anxiety and questions whether the actual implementation is really that simple, and viable.

The writers experience this less because they know the blogs have been bringing that income.

Frugality is Not Just for the High Income. In fact, it is the Opposite

The writer at the Outline got it very wrong.

I think he is trying to detect flaws in the plan.

To be fair, if you save 71% and that does not include your 401k contributions, your income tends to be high.

However, one of the reason why the Frugalwoods can have such a high rate is because they are very clear about what they value, what they don’t.

They also develop that higher level competency to deconstruct things and get things for the cheap.

In various podcast interviews (she went on a spree of podcasts), she cited that back when she started out earning US$10,000/yr in New York, she was able to save US$2,000 on that salary.

That is seriously tough to do (NY is a high cost of living place).

In the book Portfolios of the Poor, the writer explains how the really really low income manage their money.

Because the income is so volatile, they need to become master money managers.

When you have less money, to build wealth and live a life, you need to know what you value, what you do not, and optimize your money accordingly.

When you have high income, you do not need to do that.

You can afford many wealth mistakes. Your buffer for mistakes is much higher.

The writer probably got very tired of that same narrative of these privileged folks dishing out the same spew, while at the same time not acknowledging it is their income that gives them the major leg up.

What gets you to financial independence fast is a good net cash flow. You cannot ignore the math.

However, it is one thing to want to push back on the narrative, its another to attribute frugality is a high income earner’s plaything.

Summary

At the end of the day, your blog is personal.

What you wish to write about, not many people can stop you. However, you do have to entertain the push back if a lot of people harshly disagrees with what you wrote.

In Singapore, FI is getting popular. FIRE is a different animal and not many would willingly say that is the path they pursue.

The higher income earners get a high income at the start and have all these materials to learn from. They will get there in a more efficient manner. And they will suffer from the same unconscious FIRE writing without respecting that many people are in a tougher circumstances.

There are still ITE grads, poly grads and private degree grads that do not start off with that. It is still hard for them to get into a civil service job and they will face the volatile job challenges that comes with slogging to earn enough money and respect.

What Tanja didn’t get right is that many folks still do not know what they do not know.

Somewhere in their blogging journey, they would gain further insight, and realize that the reality is different. You hope that they do highlight these changes so that the readers would know.

If you like materials such as these and would like to enhance your Wealth Management towards have a Wealth Machine that gives You Financial Security and Independence, Subscribe to my List Today Here >>

If you like this do check out the FREE Stock Portfolio Tracker and FREE Dividend Stock Tracker today

Want to read the best articles on Investment Moats? You can read them here >

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Alan

Wednesday 25th of April 2018

Hi Kyith,

I think theres alot of FIRE garbage around, and this really appeals to those stuck in the tedium of a 9-5 job and forever hating their bosses and colleges.

And half the time , some of the bloggers don't reveal that they have an inheritance somewhere or that their blog brings them a certain amount of income or that they earn among the top 20 percentile salaries . They peddle frugality but there is quite the dishonesty around with their sponsors, and sources of revenue and/or their information given.

I would say that Financial Awareness or being Financially Responsible and Educated is important, and thats what the good Financial Bloggers teach us. They share their experiences and failures and also their thought processes.

Through transparency, through their own mistakes and also through their honest and thorough analysis which they put out everyday to inform others. They point you to the right books and processes and dont try to sell you snake oil .

Kudos to them and to you as well.

Kyith

Friday 27th of April 2018

Hi Alan, thanks for the compliments. There can be some conflict of interest. A few years a go one USA blogger seem to know that this financial frugality, independence theme works very well, so kept promoting his blog as such. Got onto a few prominent sites.

Then his friends started outing him. This was 4 years ago > http://www.budgetsaresexy.com/the-millionaire-liar-next-door/

csky

Sunday 22nd of April 2018

Hi Kyith, nice summary of some of these "hidden issues" about FIRE. To be fair, many of them are teaching good financial principles (save as much as you can) and invest wisely.

Although I agree that it's pretty hypocritical to preach for everyone to retire early [never work again] while these bloggers continue to get lots of side income from their side gigs.

Also, many of the US bloggers have the advantage of investing in low-cost vanguard index funds, where they are lucky that the US indexes have gone ballistic since the GFC. Passive investment in the STI index is unlikely to yield such good results.

So, as with many things, it's a case of readers' beware! Just like I have much reservations about the hype around Rich Dad Poor Dad that encourages everyone to be their own boss, I guess, it's good for readers to know FIRE is an option and possibility, but you will have to figure out your own path based on your own circumstances and needs.

Rather than FIRE, I would like to focus on FI which is a necessary goal for everyone. FIRE kind of skew the situation into some sort of a crazy race to see who can get there faster. And like you say, many of the FIRE folks are not retired, they are simply FI and still working!

P.S: I could comment on your posts in Safari. Had to open up Chrome to leave my comment. Maybe this is something you want to look into.

Kyith

Sunday 22nd of April 2018

Hi CSKY, thanks for contributing here. I think you brought up an important point on the advantage of low cost index funds. That is an advantage not just in America, but in Australia, UK, Canada.

My question is, if the Blackrock, Vanguard and Dimensional Fund Advisers do set up shop for singapore and you need to invest 10k in one shot would that be a viable solution.

FI is a worthy pursuit but i think the narrative becomes retire early. FI always have some utility provided you don't lose everything and focus upon it.

I am trying to fix the mobile issue. I do not know why the comments are not showing up!

Jared - SMOL

Sunday 22nd of April 2018

Kyith,

This post and some of your recent posts...

I sense a shift in the balance of the Force!

If you get too many "rubbish" dump on you for being a "dustbin", you know who to contact for coffee during weekdays ;)

Kyith

Sunday 22nd of April 2018

I know. I will look the person up haha!

Createwealth8888

Sunday 22nd of April 2018

Those F.I.R.E bloggers in Singapore whom I know are previously earning high income with high saving rate. In investing, your account size really matters!

Kyith

Sunday 22nd of April 2018

Hey uncle CW8888, it does and perhaps eventually the cater audience is actually those that are doing well not those that are trying to get somewhere