Suppose you need to spend $40,000/yr the next year for your family.

Based on the proverbial 4% Safe Withdrawal Rate, you would need to accumulate $1 million in order to seriously think about whether both spouse could both retire or not.

The 4% withdrawal rate is tested through historical rolling 30 year periods, on a 50% equity 50% bonds allocation. 4% gives a high probability your money would last 30 years.

It is inflation adjusted and therefore preserve your purchasing power.

So could we use this to evaluate we are ever ready to not work?

In yesterday’s New York Times article, a 35 year financial planning veteran presents some real life contrast to using the simple 4% withdrawal rate.

Read The Myth of Steady Retirement Spending, and Why Reality May Cost Less

From his observation, financial planner Neal Van Zutphen wishes to highlight the following:

- Your spending tends not to be in a straight line

- You pay be more ready to retire than you think

- healthcare costs go up but a lot of the cost goes down typically

I think this is not the first article to point out about the spending trends. There are some recent research that says your spending tends to go down over time.

Certified financial planner Michael K. Stein breaks up your spending in retirement into 3 phases:

- Go-go years

- Slow-go years

- No-go years

Here are the data from the Bureau of department of statistics:

- 55 to 64 year old headed household mean spending $65,000

- 65 to 74 year old dropped to $55,000

- after: $42,000

- housing cost steady

- healthcare cost rising

- transportation, entertainment, clothing, food and drink decline sharply

David Blanchett, head of retirement research at Morningstar thinks the spending resembles more of a smile. It does down then comes back up. The later years spending usually is related to healthcare.

Mr Blanchett suggest the financial planner create an alternate projection where inflation is 1% less.

What I Think: You Can Accumulate Less, but Only if your Current Expenses are not Extremely Optimized

Generally, I think you got to trust a little what a veteran financial planner says. They probably observe enough of how retiree spends to make that comment.

However, this article sought to give confidence to people.

And generally researcher Michael Kitces have emphasize that the 4% withdrawal rate is the worst case scenario.

In a lot of the 30 year rolling periods, the rate of return on a 50% equity and 50% bond asset allocation is higher, and thus can condone a higher withdrawal rate.

That would mean you need less money and you might be ready to retire much earlier:

- 4.5% withdrawal rate: $888,888

- 5.0% withdrawal rate: $800,000

You could accumulate 10% to 20% less.

However, there are caveats to this.

Your expenses are more likely to go down if your spending is not the super frugal sort. Your expenses could include helping out your children in their daily living, education, going for holiday.

In that case, you would have some areas to cut down.

However, if your expenses is already super frugal, you might not experience a sharp drop in your expenses like the go-go, slow-go and no-go scenarios.

To retire, you would need to understand your annual expenses well.

To sum it up, here is how you can visualize your withdrawal rate.

If you want to make a 5% withdrawal rate to work, your annual expenses should need to be divided into

- 3-3.25% mandatory expenses that you cannot cut down

- 1.75-2.0% discretionary expenses for rich life living

This will make up 5% but essentially what is important to you is that 3-3.25% withdrawal rate.

Based on research, 3-3.25% withdrawal rate is safer in a

- lower growth scenario (market returns are lower)

- traditionally more expensive valuations

- longer period (>30 years to 60 years)

the other 1.75% to 2% is to be cut down if the situations get a bit challenging.

In short, we called this variable withdrawal spending (read my guide here).

A lot of you are planning in mind that you would never have to go back to work.

That is a psychological thing and we all define risk adverse very differently.

For some of you, you wish absolute safety, then I would say, shoot for 3-3.25% withdrawal rate. So if you need $40,000/yr then its $1.23 mil.

For some, you have high confidence you could always go back to work or have some ways to cut your expenses, then its 5%, knowing you can cut to 3.5% if you need. You can work with $800k or 30% less.

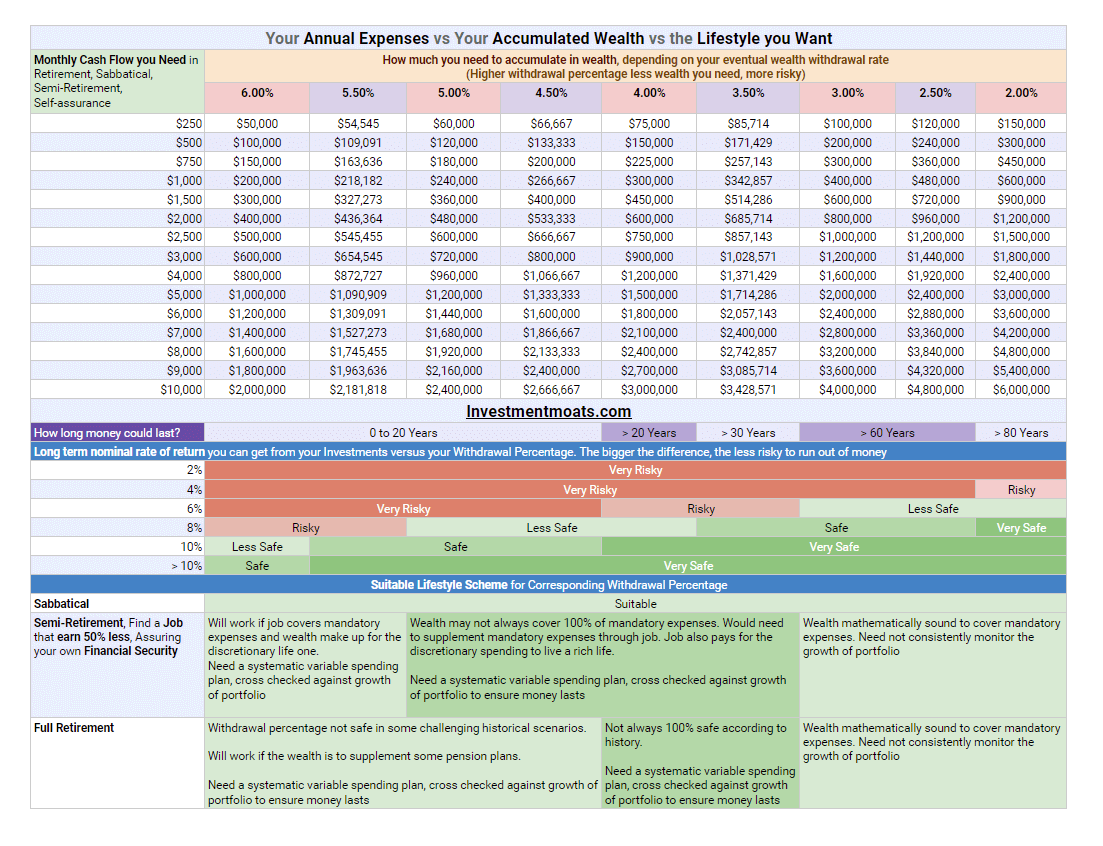

This is probably the first time I debut this, but the following table could help you figure out the relationship between:

- your annual expenses

- your investment returns

- how long your money last

- how much you need to accumulate

- the lifestyle scheme you want

click to view larger illustration

There is a relationship between those 5 items:

- higher withdrawal rates in retirement or financial independence means the less wealth you need to accumulate (vice versa)

- higher investment returns over time means you take on more risk, but you can have a higher withdrawal rate (vice versa)

- higher withdrawal rates means your money may not last as long (vice versa)

- higher annual expenses means you need to accumulate more wealth (vice versa)

- the more risk seeking your lifestyle choice, the less money you need to accumulate (vice versa)

Going back to that example, suppose your current family expenses is $3000/mth. Based on the 4% rate, you would need to accumulate $900,000. If the average rate of return you get is around 6%, it is rather risky, but if its 8% its not very safe but its doable. Your money probably will last between 20 to 30 years.

These are based on worst case scenario.

Those who are more risk adverse would step down to 3.0%. They would need 30% more to accumulate to 1.2 mil. Even a 6% rate of return might be workable. Their money would last 60 years.

The risk seeking ones can work with a withdrawal rate of 5.0% and aim to achieve 8% investment rate of return. Their wealth covers majority of their mandatory expenses, while the work covers part of their mandatory expenses and most of their discretionary expenses. While traditionally a 5% withdrawal rate can run out in 20 years, supplementing with work can extend this and make it viable.

Thus, you might need less money, but you might be so risk adverse that you do not feel safe.

I think the table can help you better sort out things

My financial independence and retirement stuff is at #6 below:

Do Like Me on Facebook. Join my Email List. I share some tidbits that is not on the blog post there often.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

John Drent

Thursday 6th of December 2018

But the question is: is 3% withdrawal rate a sustainable amount even as we move ahead in a world of incremental pricing. The number may work well for active retirement for decades, but I think it does depend on the individual.

Kyith

Thursday 6th of December 2018

i think they went through a lot of rolling market cycles, with 30 year, 50 year, 60 year duration. what do you mean by incremental pricing?

Sinkie

Sunday 2nd of December 2018

Ideally the best would be a national pension plan or annuity, using the 3% withdrawal rate & 50:50 equity-bond mix.

This would remove the psychological aspect & wavering risk appetite from individual investors.

3% withdrawal rate from a 50:50 portfolio has very high chance to last many decades, but whether individuals are disciplined enough to maintain it, rebalance annually etc?

Kyith

Monday 3rd of December 2018

yup 3-3.25% on a 50/50 works. if you want 3.5% perhaps 75/25. still good enough. but i think the national pension plan people would worry of a shifting goal post.

Createwealth8888

Sunday 2nd of December 2018

Beware that our risk appetite may gradually change when we step into non incurring earned income from full-time employment after some years and especially true for those who are marginally financial independence.

Kyith

Monday 3rd of December 2018

i think living off savings is psychologically different than thinking of living off savings