If you are planning for your retirement, you will approach your financial planner to help you plan how you can systematically spend down your wealth.

Your goal is probably to create a stream of cash flow that can meet your retirement expenses and perhaps, leave a sum of money for the next generation (we called this the bequest)

In the past, I have written about planning for retirement (RET) or financial independence (FI), how much you need, how do you know if you are ready, and what are some ways to systematically spend down your wealth.

I consolidated them in my Planning for Retirement section.

We cannot remove the relationship between how much you need in RET/FI with how you systematically spend down your wealth, how much you need to set aside for the next generation.

And thus some of the solutions that we suggested centers on a recently widely researched safe withdrawal rate called the 4% Safe Withdrawal Rate.

In 2 studies in the 1990s, by Bill Bengen and a Trinity Study, both determined that:

- Based on rolling 30 year historical US bonds and equity data, withdrawing 4% of your wealth in the first year is sustainable

- 4% is the lowest withdrawal rate out of a lot of withdrawal rate that will have a very high probability of success

- Based upon a 50% equity and 50% bond allocation (Bengen’s study and Trinity study uses different bond components)

- Based upon a 30 year period

- After the first year, your spending adjusts for inflation (typically 3%/yr). So if year 1 you spend $40,000, year 2 you spend $40,000 x 1.03 = $41,200, and so on. This rule ensures your spending keeps up with inflation

- Also known as the Constant Inflation Adjusting Withdrawal Method

The appeal for using this safe withdrawal rate in your planning is that it is very simple to find out if you are close to ready for retirement.

For example, if your current spending is $33,000/yr, how much you need to accumulate is $33,000/0.04 = $825,000.

If you are missing a couple of $100,000, it is rather motivating.

The downside is that:

- based on historical data

- rate of return in the past might be higher than in the future (the opposite is also possible)

- 4% might not be safe anymore

- based on 30 year period, which may be too short or too long for your case

- you might be less risk adverse

- you might be half working half enjoying

Still, I think 4% is a very simple way to let you know how close you are from thinking about planning FI this seriously.

As such, I have covered various ways people have thought of to systematically withdraw their wealth.

We called these Systematic Withdrawal Plans (SWP).

The idea is that your wealth is like your parent. They decide what is best for you. They want to be prudent, but also make sure you do not starve, not run out of money.

So they will say: “Girl, you can only withdraw $41,200 this year.”

I have written a few articles that explores various withdrawal methods:

- Variable Withdrawal Strategies for Financial Independence- The Definitive Guide

- Explaining Sequence of Return Risk and Possible Solutions

- Target Percentage Adjustment

- 4% adjusted, Guardrails, Floor and Ceiling

Today, we are going to add a different perspective to the discussion.

We are going to explore if we can incorporate some of the SWP rules of Endowment Funds.

Endowment funds and foundations are your universities, charity foundations.

They have a specific requirement to provide cash flow to the university and foundations but also to ensure they do not run out of money.

To a certain sense, they fit closely to those pursuing FI:

- you will spend a percentage of your wealth

- you need the money to last a long period, and you may wish to leave a bequest

- you will work on and off, to add on to your wealth or supplement your expenses

Thus compare to endowment, the requirements are pretty similar.

So let us see what we can come up with.

The Challenges of Endowment Funds

Endowment funds have unique challenges:

- They need to meet current spending needs

- They need to ensure wealth supports spending needs in the future as well

- If they spend more now, it might mean less money in the future

- Their time horizon might be infinite

A foundation’s spending needs include:

- university operating budgets

- periodic building projects

- grants to not-for-profit organizations

- medical research

As the endowment horizon is infinite, it would mean that the way that they invest has to be different as well:

- how they set up their investment structure

- their asset allocation becomes important

- aggressive, concentrated investing may cause the wealth to be destroyed by both the spending and the decline in portfolio

- conservative, diversified investing may cause the portfolio not to grow sufficiently to keep up with inflation

Depending on the endowment, some may prioritize spending needs over preservation of wealth, while for others their priority is the opposite.

You realize, that is how a lot of people live their FI lives as well.

Somehow I realize my concept of the Wealth Machine is somewhat about endowment funds.

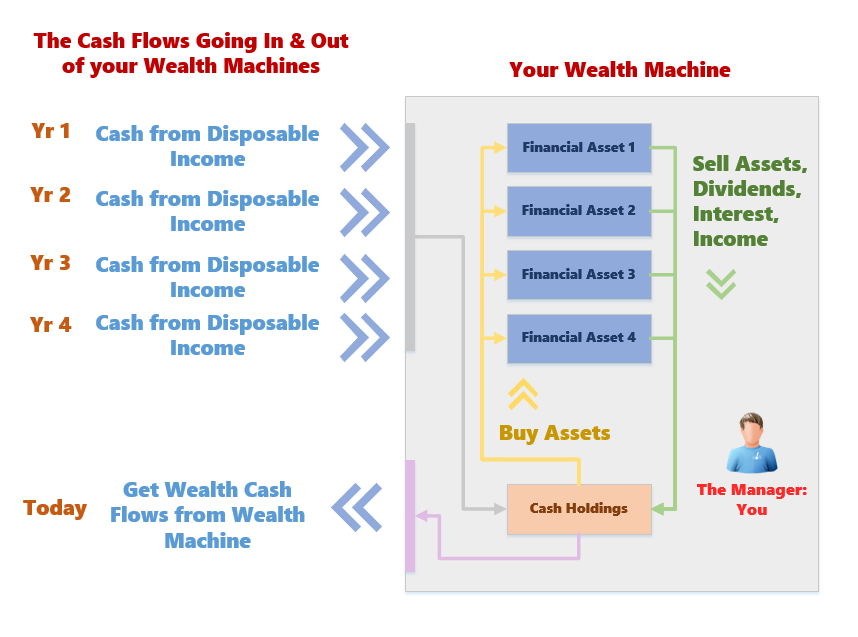

An illustration of how similar my wealth machine is to the endowment fund

Briefly your wealth machine:

- Is managed by yourself the manager. You might delegate to other managers (unit trust managers, whole life insurance participating fund managers)

- You fund your wealth machine with consistent cash flow from your disposable income

- As the manager, you take the cash holdings and deployed them into financial assets, based on your investment philosophy

- When your financial assets return the dividend, rental, interest income, realized capital gains or losses, they go back into the wealth machine

- Depending on the phase of life, and your objective, the manager, through their systematic withdrawal plan, tells you how much you can withdraw, so that you have a good amount to spend, but also that you do not destroy your wealth machine

What I do understand from a lot of people is that, they wish to keep their money infinite.

And thus their idea is only to spend the dividend and interest income, and at most the capital gains only.

The income and capital gains, make up the total returns of your financial assets. If their dividend income and capital gains fluctuate, your spending is going to be volatile. And they might not keep up with inflation. Thus, there are virtues of spending a percentage of your wealth rather than only spending the income and capital gains.

Click to view in detail

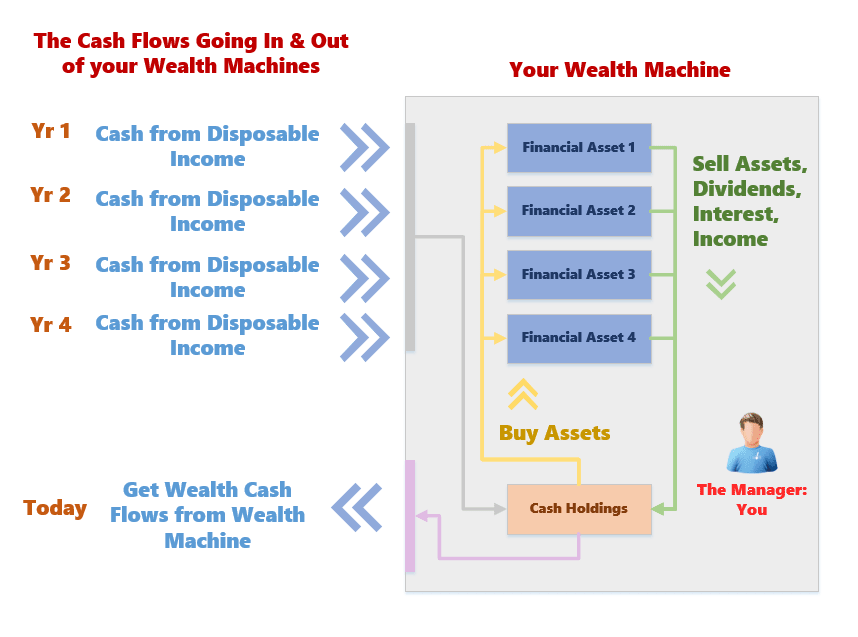

Your wealth machine can be model as an endowment where, depending the phase of life, and the scheme you live, you would choose to take wealth cash flow distribution. At different phase, you might still have income coming from disposable income.

There can be at times larger wealth cash flow distributions, and that could deplete the machine. Thus someone needs to keep a tight watch on things.

You wish to prolong it such that, any amount you do not use, the next generation can make use of it.

Endowments do have some unique spending characteristics that are similar to us: Periodic Predictable Large Spending.

While they need to upgrade their university premises, you will have to renovate your worn down home. While there may be many large projects proposed along the way of varying degrees, it is something that you can work into your spending since we know that as a university, you will have these proposal. Similarly as an individual, you are going to have grand kids coming to you with these proposals

What make Good Rules for Spending?

From what I gather, the following are some good rules when planning your spending to be endowment like:

- Allow an adequate amount of spending each year

- Have some degree of predictability from year to year

- Take into account inflation when applying the spending rule

- Allow spending to increase modestly during good times

- Maintain spending during difficult periods

- Do not spend so much that the portfolio declines on a real-basis

I learn this from some actuary blogger that this is more of a Sustainable Spending Plan. I guess the difference is that spending takes the center stage.

In a lot of the 4% withdrawal rate or variable withdrawal strategies, we are developing a Systematic Withdrawal Plan. In this, preserving long term spending and wealth assets take center stage.

With that, here are some spending rules that endowment funds would made use of.

The Different Spending Rules utilized commonly University Endowments

5% Constant Percentage Withdrawal

I think this is the starting point for a lot of endowment plans. It is one of the variable withdrawal strategies in my variable withdrawal strategies article.

The endowment will spend a agreed upon percentage of previous year-end market value.

It would seem endowment funds use 5%.

So if you are modelling this strategy, if last year your portfolio is $483,500, for this year, you can spend 483500 x 0.05 = $24,175.

The strength about this strategy is that you will not run out of money since it is always 5%.

The weak point is that, if the value of your wealth machine fluctuates, your spending will fluctuate.

To the point that it might not make sense.

The counter point to this is that, it depends on what you invest in.

You can

- lower the volatility of your wealth machine

- the returns are likely to be lower

- when the assets value is more consistent, so is your spending

Average Market Value Approach

This one builds upon the constant percentage withdrawal.

Instead of taking last year’s wealth machine’s value, we take an average of past x number of years.

This could typically be 3 years but I do understand endowments like to use 10 years.

Sometimes they will set a floor and ceiling percentage.

So we could have a rule that:

- takes the past 4 years average value

- have a floor percentage of 3% and ceiling percentage of 7% of current market value

If we build on the previous example, suppose the average past 4 years value is $350,000:

- 3%: $10,500

- 5%: $17,500

- 7%: $24,500

Since last years spending is $24,175, which falls within the 7% boundary, the permitted spending is $24,175.

What we have is a smoothed out spending. It also tried to preserve the spending power.

Inflation Adjusted Approach

This seem to be similar to the safe withdrawal rate.

The endowment take 5% of the endowment value in the initial year.

Then for subsequent years, the spending is adjusted for either the inflation that year, or a given inflation rate.

The upside of this is that at least the purchasing power is preserved.

Like the safe withdrawal rate, you may deplete your money if the initial percentage is not conservative.

Yale Rule

This is popularized by the famed Yale University Endowment Fund (managed by David Swensen)

It basically combines the average market value approach and the inflation adjusted approach.

So a typical Yale Rule could be:

- 50% based on 5% of last 3 years average market value

- 50% based on last years spending index to inflation

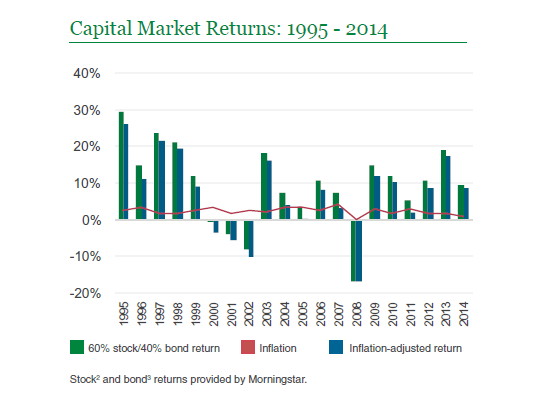

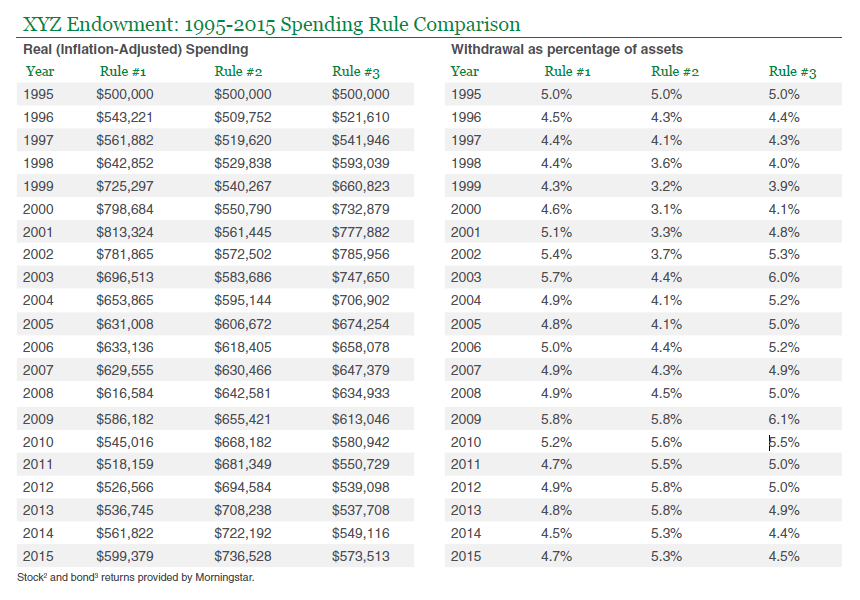

Simulating through the 20 years of 1995 to 2015

At this point, it seems this is not much different from my variable withdrawal strategies.

However, Let us take a look at some research how this fared in a 20 year period with 2 bear markets.

The research shows us the withdrawal rates for a $10 mil portfolio over the 20 years.

The parameters:

- Assets: $10,000,000

- Initial Withdrawal Percentage: 5%

- Allocation: 60% Stocks 40% Bonds, annual re-balancing

They took a look at 3 approaches

- Average market value approach: 5% of 3 year moving average of year end assets, but not less than 3% of current market value and no more than 7% of current market value

- Inflation adjusted approach: spend 5% of market value in 1st year, then adjust for inflation of 2%

- Hybrid approach: 50% of 3 year moving average of year end assets and 50% of last year spending indexed to inflation

This period saw some great capital growth but also 2 very drastic market downturn. One of them lasts 3 years while the other last 1 year but just as brutal. The inflation during this period is rather low.

This period saw some great capital growth but also 2 very drastic market downturn. One of them lasts 3 years while the other last 1 year but just as brutal. The inflation during this period is rather low.

The first thing we noticed is that all three survived relatively well.

The first thing we noticed is that all three survived relatively well.

Assets value go up from $10 mil to $17 mil at the peak of 2000, then drop to $12-13 mil at the end of 2003.

In terms of spending, inflation adjusted approach gives you the greatest spending. No surprises there as rain or shine, this rule preserve your purchasing power.

There is not much difference between the average market value and the hybrid approach.

Some notes.

Average market value approach:

- Spending in real terms, adjusts up but also adjusts down pretty fast

- In 2005, we can see spending 22% below that in 2001. This is because of the time delay as we take 3 year average of very poor years

- Withdrawal rates was between 4.3% (1999) to 5.8% (2009)

- Withdrawal rates was pretty smoothed out

Inflation adjusted approach:

- Spending keeps going up

- Withdrawal rate is the most volatile compare to the other 2 (3.1% to 5.8%)

- In 2009 withdrawal rate increase from 4.5% to 5.8%, but inflation was rather muted

Hybrid approach:

- spending increase more slowly compared to the first rule, but decrease more slowly than the first rule

- since 50% is inflation adjusted, real spending is more predictable than in the first rule

- withdrawal percentage is more volatile than first rule

Stimulating through Stagflation of the 1973 to 1982

The researchers decide to throw these 3 rules against a pretty challenging period.

The 1973 to 1982 period is littered with draw down and recovery, not to mention high inflation rate. If you want to see if your strategy lasts, this is probably one back test to do.

So this is how they did

1. Average Market Value Approach

The 2 chart above shows the nominal and real (neutralizing your purchasing power) withdrawals and asset value of this approach.

- the asset base dropped 28% in 1973 to 1974 in nominal terms

- in real terms the drop was 41%

- the asset value finished at $10.6 mil in 1982

- spending fell by 18% in 1976 in nominal terms and 37% in real terms

- due to high inflation, real spending kept falling

- by 1982 real spending was 53% below the start

- current withdrawal rate was between 4.4% to 6.0%

2. Inflation Adjusted Approach

- between 1973 to 1974, assets value fell 28% in nominal terms

- in real terms the drop was 41%

- due to high withdrawals, by 1982, asset value fell by 34% in nominal terms and 70% in real terms ($6.6 mil at the end)

- in nominal terms, the spending rose 160% over the first year

- in real terms spending only increase by 18%

- current withdrawal rate is between 5% to 19.6%

3. Hybrid Approach

- nominal asset value will finish at $10.1 mil at start 1982

- in real terms asset value went down by 54%

- nominal spending fell by 6 to 9%, remaining the most consistent out of the three rule

- in real terms, the spending fell by 52%

- current withdrawal rate is between 4.8% to 7% (1975)

Some Conclusions from the 3 Rule Study

We can summarize a few conclusions:

- Inflation adjusted result in higher levels of nominal and real spending

- Percent of market value gives the lowest level of spending

- Inflation adjusted depletes the asset base the fastest

- Percent of market value depletes the asset base the slowest

- Hybrid is always in between

Withdrawal Rates of University Endowment Funds

The following is what I gather of the withdrawal rate for different categories of endowments:

What is interesting is that for this regime of the markets, their withdrawal rates look very consistent.

It does look like they are balancing their budgetary spending versus capital preservation versus generating stable returns very well.

David Swensen was the one who pioneered allocating towards more alternative asset classes such as private equity, venture capital funds, timber. This is in contrast to a 60/40 portfolio.

In fact Warren Buffett in his recent newsletter, chided these endowment funds for likely paying excessive management fees rather than adopting a simpler approach.

I guess the goal is different for these endowment funds. They really need the low correlations between asset classes such that the overall portfolio volatility is much lower.

How Endowment Does Things is Not Much Different From the Withdrawal Strategies that We Explored

I looked at what Vanguard recommends institutions.

And I look at the problems that people think about these institution withdrawal strategies and they do not seem very different from the dark arts of retirement planning.

The most prevalent is the smoothed moving average of a percentage of market value.

The recommendation to get it better is to apply a floor and ceiling percentage, or inflation indexed it, or a mixture of the above.

And experts are questioning whether in a different environment, would the 5% constant percentage withdrawal rate is too dangerous.

When we contrast this to the dark arts of FI planning, its the same.

You can have a constant percentage of assets, floor and ceiling, or a combination.

And the downside are the same, which is you do not keep up with inflation and lose purchasing power.

In our personal retirement, the experts are wondering if the old 4% rate is too optimistic.

The Importance of Flexibility and Active Management of your Spending Down and Investing

What is recommended in a lot of the advice to endowment managers seem to be to be flexible.

And to be flexible can mean a lot of things.

I read this as to be flexible in your spending. Your spending is often tied to what are the “proposals” that are put in front of you. There are projects that, from the long term basis, is worth sacrificing, despite the markets not doing very well.

There are projects that could be delayed until the finances stabilized.

In your retirement, this is applicable as well.

The other thing that you need to be flexible is to anticipate the changing regimes. There are a lot to be said about how poor active management have under perform their benchmarks.

However, I wonder if our goal here is to under perform or to preserve our spending power.

If it is to do that, then anticipating a shift in the regime and a shift in asset allocation to one that preserve purchasing power might be more appropriate.

My financial independence and retirement stuff is at #6 below:

Do Like Me on Facebook. Join my Email List. I share some tidbits that is not on the blog post there often.

Here are My Topical Resources on:

- Building Your Wealth Foundation – You know this baseline, your long term wealth should be pretty well managed

- Active Investing – For the active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

Fred

Tuesday 4th of December 2018

This article looks like it is adapted, expunging and pasting from American literatures. Any retirement and financial subjects in Singapore that do not incorporate CPF and HDB structures, are just that; idle banters.

BigBoiBoi

Tuesday 4th of December 2018

There is another way adopted by the SIngapore Government in spending the Singapore's reserves: a) Net assets invested by GIC, MAS, Temasek - Spend up to 50% of net investment returns (long term expected real returns)

b) Other net assets - Spend up to 50% of net investment income (actual dividends, interest and other income received from investing the reserves, as well as interest received from loans, after deducting expenses arising from raising, investing and managing the reserves)

https://www.mof.gov.sg/Policies/Our-Nations-Reserves/Section-III-How-do-Singaporeans-benefit-from-our-Reserves

Kyith

Tuesday 4th of December 2018

Hi Bigboiboi, thanks for that. I sort of remember that but it would entail 2 different portfolio. basically a low vol portfolio made up of dividends, interest and other income, and a portfolio made from spending half of the long term real returns. I wonder how much the real returns is over time.