Would you escape one prison, only to find yourself jumping into a different prison?

One day, I stumbled upon this discussion between one of our associate adviser and a client adviser. They were discussing how much a lot of people would yearn to escape wage slavery by being financially independent.

However, in financial independence, you would be imprisoned by the anxiety in wondering how much you could spend, so that your money can last long enough before you passed away.

If you think deep enough, that conclusion is not too wrong. The prison, in this case, is to have something dear held captive against your will. If you are an office worker, you are forced to work for a paycheck which would pay for what your family needs. In financial independence, your stability will be taken away from you.

Anxiety Plagues those that have greater Financial Awareness and those whose Situation Are Borderline

I think that being trap in a prison in both cases is only true, for people that are paranoid by ensuring that they have quite a sound plan before they pull the plug to stop work, or in the case of work, jump into a job knowing full well that it is secured.

On the job spectrum, you are a self-aware terrible performer or a self-aware strong performer. The former knows that you might not be around anytime. Your situation might be volatile but you sort of accepted that and YOLO as much as you can. The strong performer knows that more or less she is safe and even if she is not, a strong performer should do well in another organization.

On the financial independence spectrum, suppose you think you need to spend $40,000 a year and you are really tired of working and wish to take a break. If your portfolio is $100,000, you know that sooner or later, you will need to look for a job. If your portfolio is $5,000,000, you know more or less you don’t have to work for a long time.

The greatest anxiety usually occurs when you are in the middle. In some scenarios, you are safe. However, in another scenario, you are not so safe. You are a self-aware average performer at work or that you know you have accumulate a sum of money that most trusted adviser cannot say for certain it will last for a long time.

There are also the blissfully unaware ones who have less anxiety (but that may not always be a good thing).

In the latest Schroders Global Investor Survey, the average percentage of retirement savings people think they can realistically take out each year and not run out of money is 10.3%. If you are a long time Investment Moats reader, you would notice that this is a very optimistic withdrawal rate. Perhaps too optimistic.

We May Need a New Way to Determine Levels of Our Wealth

I pondered on that discussion they have and wonder that perhaps whether you are rich or not is more of a state of mind.

Real wealth may be to free us from worries.

So the right measure is how rich can you be such that you do not need to worry about spending on ___________. The sign of financial independence readiness may be whether we can live a life with little anxiety.

In the past, I had introduce you to a ladder of wealth stages that you could use to track your progress when building wealth.

The idea is that you need to do things to get to a better wealth position. Each stage is an improvement over the previous one.

Each stage is also has a certain utility.

For example, as you become more motivated, you earn more, optimize your expenses and invest well, you will move up from Stage 4 to Stage 5. Having a wealth asset that is worth 5 years of annual expenses is definitely more useful than just 1 year. Imagine if you really do not like your domain at work and wish to make a career transition which can be risky.

You may need a longer runway to feel safer, and that can be provided by 5 years of annual expenses instead of 1 year.

The stages of wealth were distinguished by quantifiable amounts that is meaningful to you. If my expenses are $25,000 a year, stage 5 to me is $125,000. If your expenses are $60,000 a year, stage 5 to you is $300,000.

You may have encounter friends who have a lot of money, more than you but they seem to still suffer from the same anxieties as yourself.

In a way, quantifying your wealth might not make the person link to how to utilize this wealth. Perhaps only when you reached Stage 7, you are so far down learning about personal finance that you understood the utility of the level of wealth you have now.

Perhaps we need a better way to link our wealth to give us a feeling that money at certain levels are really useful.

Distinguishing Levels of Wealth Based on Mental Freedoms

Stewart Butterfield and his team tried to get a multiplayer game off the ground. The game didn’t get off the ground. However, they found that they really like this messaging component they built into the game very well.

So Stewart’s team decided to pivot and focus on turning the messaging component into an app.

This app is Slack, which is a messaging application that many teams use today to communicate. Slack got listed in Jun 2019 and this made Stewart Butterfield a very rich man.

In an NPR | How I built this with Guy Raz episode, Stewart told the host that wealth beyond a certain point does not make your life better.

That is very cliche. However, Stewart did list what he considers as his three levels of wealth:

- Level 1. I’m not stressed out about debt: People who no longer have to worry about their credit card debt or student loans.

- Level 2. I don’t care what stuff costs in restaurants: How much you spend on a particular meal isn’t impacted by your finances.

- Level 3. I don’t care what a vacation costs: People who don’t care how expensive the hotel is or which flight they go on

Compared to my stages of wealth, Stewart’s levels of wealth does not quantify the wealth but focus on quantifying the financial freedom that it provides.

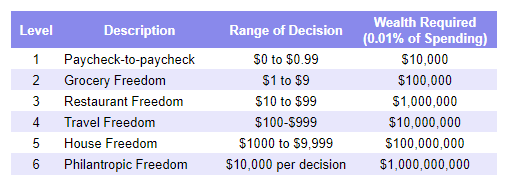

Nick Maggiulli from Of Dollars and Data expanded on this beautifully by re-engineering Stewart’s three levels with something we often can relate to:

- Level 1. Paycheck-to-paycheck: A $0-$0.99 per decision. You are conscious of every dollar you spend. This includes people with crippling debt.

- Level 2. Grocery freedom: A $1-$9 per decision. How much specific grocery items cost don’t impact your finances.

- Level 3. Restaurant freedom: You eat what you want at restaurants regardless of the cost. A $10-$99 per decision

- Level 4. Travel freedom: A $100-$999 per decision. You travel when you want, how you want, and stay where you want.

- Level 5. House freedom: A $1,000-$9,999 per decision. You can afford your dream home.

- Level 6. Philanthropic Freedom: A $10,000+ per decision. You can give away money that has a profound impact on others.

The beauty of Nick’s ladder lies in that he help us quantify how much wealth we need to have so that we will not spend and be anxious about it. Nick determines that if a spending decision is varying just 0.01% of your liquid net wealth, it doesn’t matter much whether you choose something more expensive or cheaper.

Let us take Level 2 as an example. What would make your choice of grocery be inconsequential? Take $10 divide by 0.0001 and you have $100,000.

Whichever grade of celery, chicken that you choose, it will make very little impact on your net wealth at $100,000.

This gauge I feel is pretty good. For example, when it comes to eating out, I really care less about the prices now. Whether a meal is $5, $10, $40, it really matters less to me. In comparison, my portfolio gyration in a day is the difference of 1 or 2 MacBook. My choice of food would impact my finances less than what happens to my portfolio.

When you attain a certain level of wealth, you should feel rich enough. It should free you up from something that you were constrained to.

Does Nick’s Solution Alleviate Anxiety Well?

If Nick and Stewart’s levels of wealth worked on me, then it is truly remarkable.

Unfortunately, money anxiety is a state of mind.

Long-time readers will probably know my rough liquid net wealth. My level would probably be Restaurant Freedom on Nick’s level of wealth.

We eat 90 meals a month. If each of my meals cost $100, that is $9000 a month. In 1 year, this moves 10% of my liquid net wealth.

Going crazy on one or two meals do not matter. Going crazy with the frequency matters. Perhaps the real Restaurant Freedom is when you have $10 million.

Despite this, I got to give props to Nick for creating a better framework for us to think about this.

You Should Try to Spend Well According to Your Level

Another beauty of what Nick created was that it allows you to see what kind of spending decision you can loosen and what you cannot loosen.

If your liquid net wealth is $100,000, you could loosen on eating out and groceries because the impact is less. You should control how much you spend on vacations and home choices. They still impact your wealth.

If your net wealth is less than that, then in order to progress up, you cannot ignore control of your groceries and restaurant stuff.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- New 6-Month Singapore T-Bill Yield in Late-April 2024 to Drop to 3.70% (for the Singaporean Savers) - April 18, 2024

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

Steveark

Sunday 12th of January 2020

I'm at the top level of any rational scale. But that only removes the trivial worries of life. The important stuff, how your kids are doing, the health of yourself and your spouse, those are real things that matter that money doesn't help with in the least. The cost of restaurant meals, that's an insignificant thing to be concerned about. Money only removes inconsequential worries, it can't touch serious ones.

Kyith

Sunday 12th of January 2020

Hi Steveark, for a lot of people we have to fret about these stuff.