Bill Sharpe, creator of the Sharpe ratio, said that retirement spending is the “Nastiest, Hardest Problem in Finance”.

There are good reasons for Bill to have that point of view. There is just so much uncertainty behind the planning. We are essentially trying to plan 20-40 years ahead for our future-self, who will live in a world that is total different from the one we experienced when we are planning it.

Recently, a string of thing happen. And it make me feel like… am I the only one around that is concerned about some of these technical aspect about retirement planning.

I started going down this rabbit hole when I got curious whether I am REALLY financial independent. I find that while the fianancial numbers may show that you are financial independent, if you are less sophisticated, you are always curious if you have “missed something out”.

What are the things that sophisticated planners know that you don’t know?

On top of that, sometimes I find myself creating these “strategies” that may sound smart on paper/pixels. But years later, after knowing more, I realize some of these “strategies” are pretty flawed.

There are some nuances of retirement income I find that… if you are not nearly there, or that you are retired, you would not easily noticed. And if you did not easily noticed, your plan may not have catered for it.

It leads me to this idea that: If your financial planner is not retired or near retirement, would they give you a good plan?

Very subjective topic.

About 3 weeks ago, I listened to this interview with Don Ezra on the Rational Reminder podcast. I wasn’t having high expectations but turned out to be a rather good interview.

Don Ezra has an interesting profile that made me feel like I need to pay attention to what he says:

- He is retired ( he is about 77 years old today) and spending down his money.

- A trained actuary.

- For 26 years, he worked in Russell Investments on the investment side of pensions. Became the director of Russell, and managing director of consulting and also director of Investment policy and research.

- Served on the executive boards of the Canadian Institute of Actuaries (Vice-President for Pensions).

- Served on editorial boards of the Financial Analysts Journal.

- Served on the Rotman International Journal of Pension Management.

It is tough to find people that are experiencing retirement spending, technical, knows the challenges of retirement spending, the challenges of the qualitative aspect of retirement, for most of his life consulted with pensions tackling this very problem.

Don probably have more money than a lot of us.

But more money does not always give you the retirement income you want.

So I decided to sit down, meditate on this podcast, and see if there are some little answers to some of the outstanding doubts that I have.

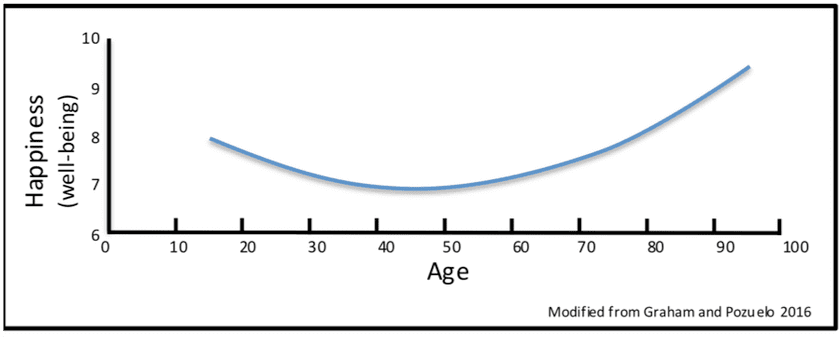

The Happiness U-curve and its Relationship with Retirement Age

Don says that if we average the happiness score that people give themselves over an entire population of the country by age, it will look like a U-curve.

Your happiness starts off very high at age 20 when you do not know much and you are getting ready in life for an adventure.

The experience of real-life starts tainting you, as you realize it is difficult to achieve the perfection you want.

The happiness tends to go down and bottom somewhere in the age range of 45 to 50 years old and then it starts climbing up.

Don investigated this happiness thing and eventually wrote a book called Happiness: The best is yet to come.

Don wanted to let people know that the peak of that happiness curve is at the end.

That peak happiness is not correlated with retirement age but is purely based on brain chemistry.

Dopamine drives us to be perfect and if we are not perfect, we are trying to do better and better and better. Eventually, the dopamine flow starts declining over time and the drive for perfection starts to decline as well.

At someone around the range of 45-55, happiness goes up because our frame of reference changes.

We became more satisfied despite our imperfections. We satisfice.

The 3 Fundamental Questions a Pre-retiree need to Ask Themselves Before Retirement

Don felt that all the difficulties people have about retirement tend to boil down to answering 3 questions:

- What is their identity? Who am I? When people retire, they lose a big part of their identity due to work.

- How am I going to fill my time? How am I going to coordinate this with my partner?

- Will I outlive my money? This is the financial question.

Why do we worry about outliving our money? How do we get “Happy Income”?

Don feels that the main reason is that it breeds uncertainty.

The amygdala part of our brain gets triggered, it freezes us or gets us in a fight or flight response.

We have been used to getting a paycheck very regularly and suddenly it is not there anymore. (Just like work income, annuity income can be addictive)

Being afraid that it is not there is a very normal response.

Someone said that since Don has written about happiness and retirement, what is considered a happy income?

we are looking at three things that are separate:

- We are looking for safety. Make sure my money is there safely when I want it.

- We are looking for growth. For most there is not enough really to do everything we want to do, so we need some growth in the future.

- We need some kind of hedge against longevity. This has got nothing to do with investment retirements and safety and growth. It is longevity safety, et cetera.

Don quote the work of Jan Tinbergen, who won the first-ever Nobel Price in economics.

However many independent goals you have, you need at least that number of financial instruments in order to do it, otherwise, you are doing it inefficiently.

Basically, to target certain goals, you need certain financial solutions.

The tough thing is that there may not be ideal instruments in certain countries.

Some people just want to know how to get income

Ben shared with us about their experience with multiple clients (they work for a Canadian financial advisory firm)

The clients biggest concern is not how much money they have.

Their biggest concern is how to get the money into their bank account.

The solution is the simplest to them.

All they have to do is carry out an electronic funds transfer twice a month just like a paycheck.

But to a lot of client’s they were astonished that it could be done that way.

Don’s philosophy towards explaining the sequence of return risk and variability of outcomes to retirees

The sequence of return risk means that the order of the sequence of returns you experience in your retirement or during your accumulating years will affect whether your money lasts during your retirement and whether you accumulate well during your years of accumulation respectively.

I wrote an article explaining the sequence of return risks and possible remedies to tackle this complex problem here.

Don feels that the sequence of return or the variability of returns should not be explained solely to only retirees.

The sequence is more important to retirees because they are not having any income and the return sequence affect them more than accumulators, who are not spending down their portfolio and not putting pressure on their portfolio.

Don feels that people need to understand that everything in life is uncertain.

The deeper question for financial planners to explore with their clients is how uncertain life can be and what are the ways we can go about hedging the uncertainties.

What causes more uncertainty for retirees: Life expectancy or Random stock returns?

Don was a trained actuary.

But he readily admits that he is even older than baby boomers ( he is a World War II baby)

As much as we are struggling with this today, it is even worse for him because he does not have any of the resources we have!

As an actuary, he has to deal with investment uncertainty and longevity uncertainty.

So this question occurs in his head, which of these two is bigger.

Here is a thought experiment he did.

- Imagine there are two very unusual planets, planets A and B

- Planet A: Longevity is certain.

- Everyone lives to the same age and you know exactly how long you are going to live.

- But returns are uncertain.

- How much money do I need for my standard of living for the rest of my life? There is financial uncertainty.

- Planet B: Investment returns are certain.

- I know exactly what I am going to get every year.

- But I don’t know how long I will live.

- How much do I need?

Don wanted to find out whether the uncertainty on planet A or B is bigger.

When he was 60 years old, he did some rough calculations. Here is his rough conclusion.

For a male aged 60, longevity uncertainty caused less of a financial impact than being 100% invested in bonds. Most of us can take a portfolio of 100% bonds.

Longevity uncertainty was not the problem.

As we age, the two uncertainties come together and cross. By the time we reach age 75, longevity uncertainty has a bigger financial impact than being 100% in equities.

Both uncertainties decline with age, but longevity uncertainty declines slower, so that is a bigger uncertainty than equity uncertainty.

If at age 75, you might be unwilling to invest in a 100% equity portfolio because you feel there is too much risk.

But you should be even less willing to take your longevity risk because that risk is even bigger than the financial impact of a 100% equity portfolio!

The number for females is five more years (instead of 60 and 75, it is 65 and 80).

How does an Actuary estimate how long they will live?

Don uses the mortality table (he calls it the longevity table instead) at longevityillustrated.org, which was put forward by the social security people in US.

Don says that longevity is greatly misunderstood.

Longevity is the average length of time for a group of people of your age and gender. 50% will live less than that and 50% will live longer than that.

If we do not want to outlive our assets, we need some kind of margin. Longevityillustrated gives a 25% and 75% number.

For his wife and him, they use the 75% number because he wanted to reduce the chances of outliving the money.

How should a new retiree looking for advice think about the stocks and bonds allocation?

The average person has no idea about stocks, bonds and allocation.

But the allocations influence the returns you get and their variability.

But Don feels that we should not primarily focus on investment returns. Returns are a means to an end.

The key things to focus upon:

- What kind of life you want to live.

- Will you have enough money to live the life you want for as long as you want.

- How much lifestyle risk can you endure.

Answering these questions will translate into your asset allocation.

- Stocks: Help us eat well in the long term, because that is where the growth comes.

- Bonds: Short term help us to sleep well because it goes down less.

Don urges the pre-retiree to think about the balance between sleeping well and eating well.

Because you need a balance between the two.

That is all there is to it.

And let the financial experts worry about the allocation. You don’t have to be good at that.

Don feels that risk tolerance questionnaires get too focus on how much we can take asst shortfall, and not enough of answering the 3 questions to focus upon.

With interest rates this low, should we still have bonds in our portfolio?

Don feels that we should not be confused about the two main roles of bonds:

- To reduce the volatility relative to stocks. Bonds reduce the overall volatility of your portfolio so that it is more livable.

- Liability-driven investing. For the first few years, can we get bonds to have a predictable cash flow to match the cash flow you need. (I wrote a little about liability-driven investing here)

Don feels that this low-interest environment is an indirect tax on the people.

How Don generates retirement income in his own portfolio

Don reiterate they want three things:

- Investment safety.

- A safety bucket but they don’t know how big.

- Growth because they might live a long time.

First, Don dealt with the Longevity part of the equation.

At age 70, he redid his calculations. His wife is some years younger than him.

The 75% joint and last survivor expectancy at recalculation was 31 years.

Based on the calculations, Don is likely to survive till 101 years old. That is 31 years away.

There is still a 25% chance one of them will outlive that but they felt 25% is acceptable.

Then, he dealt with the Sequence of return risk and returns variability

Don want to know that if markets fall, he does not want to keep taking out money if he suffers from a poor sequence of return.

Don wanted to find out how long do the markets typically go down before they go back up and he is safer.

This will dictate how much he has in the safety bucket.

Based on Don’s calculation, 75% of the time, 5 years in the safety bucket will do it.

The safety bucket is his insurance bucket, with 5 years worth of withdrawals.

The rest of his portfolio will be in stocks.

This plan allows them to eat adequately and sleep well at night.

Currently, the allocation is 25% in the safety bucket and 75% in stocks. This should give them enough for 31 years.

He does not subscribe to the view that he is older than 75, he should not have 75% in equities.

He needs growth.

The thing that enables them to sleep well at night is the safety bucket.

If the markets go down more in the future than in the past or stay down longer, then the rest of the world is in a very problematic situation.

They will not be the only ones suffering in that scenario.

Being flexible with your expenses.

Don thinks it is important for retirees to be flexible about the amounts they spend each year.

Nothing in life is certain, that is even during your working years.

This is how Don considers flexibility:

- Split your budget between needs and wants.

- Needs: absolutely need to have no matter what.

- This need is not what the rest of the world says is necessary but it is based on your lifestyle and your outlook in life.

- The rest is your wants.

You are clear then that when you make a cut, it is cutting the wants.

Don’s adjustment is based on what he learned from pension funds, defined benefit pension funds.

If there is a deficit or shortfall in income, he will spread the shortfall over 31 years. This is factoring in all sorts of spending corridor adjustments he heard of.

Should retirees consider annuities?

Don thinks that if we want to hedge the higher longevity risk after 75 years old, we can consider annuities.

Annuities to him are the cheapest form of getting a longevity hedge.

The problem with an annuity is that if we focus everything on longevity hedge, we give up the opportunity for growth.

Most people find it difficult to balance between growth and hedging.

The way to look about this is to identify how much or our expenses we should hedge so that if we do not have enough money at 110 years old, we would want that income.

Ben asks Don if not buying an annuity after age 75 is equivalent to being 100% in stocks and Don says that is the way to look at it.

Is inflation a big risk in retirement?

Don is on the fence whether inflation poses a bigger risk to retirees.

Inflation is a problem because:

- There is less time, less opportunities to recovery from inflation.

- When working, we have our human capital and may be able to deploy to get money to make up for it. After retirment, human capital is gone.

- Your time horizon of investment is also shorter.

Don have seen studies that have compared the spending patterns of retirees against the spending patterns of workers, and how much is the inflation difference.

Short term it does not make a difference but over the long term the difference is typically less than a quarter of 1% a year on average between the two groups.

The basket of services don’t get cheaper, they increase as much. The studies normalize the lesser consumption of retirees. Factoring that, the inflation is about the same.

Even though we hear a lot of wailing about do we really need a retiree inflation index, it is not going to be that different in the long term.

Decrease in consumption as a natural inflation hedge

Don cites the work of David Blanchett who came up with the retirement smile.

David depicts that due to our energy level, our consumption pattern can be broken up into three phases:

- Go-go

- Slow-go

- No-go

For no-go, Don says the best statistics he came across was from US insurance companies who say the long term care beyond 90 days, which is when the policy kicks in, affects about 33% of the people.

66% of the people shouldn’t have more than 90 days of long term care.

David came up with a nice way of comparing the length of the decline with inflation, and said typically if you can manage to cope with inflation minus 1%, that is what you have got.

So the consumption adjustment over long term is 1%.

Solutions to tackle Inflation in Retirement

Long term, equity stands to out perform inflation by quite a lot. Don does not think equities as an inflation hedge but because equities work in parallel to inflation, he consideres equity as a non-inflation hedge, and that it will outperform inflation.

So part of the solution is make sure that you have enough equities in your portfolio, despite the volatility.

In the short term, Don does not have the best solution. He did suggest perhaps inflation index bonds.

Don suggest having a flexibility bucket.

He really likes the bucketing system because we have different purposes and different risk tolerance for the purposes.

Psychologically, he does not see his money as one big portfolio but a few purpose-driven buckets.

So this flexibility bucket is like your insurance bucket.

You would have 2 to 3% of your assets in this insurance bucket. This lets you cope with sudden inflation, and with all kinds of events.

This is why he came up with 5 years of worth in his safety bucket.

The Default Planning Norms Don Uses

Here are some numbers Don used in his planning:

- All returns after fees.

- All returns in real terms.

- 0% a year for the safety bucket.

- 4% a year for equities.

Those were his original numbers. Today, he thinks some of the numbers are abit optimistic.

If he were to do planning today:

- -1% a year for the safety bucket.

- 3% a year for equities.

Don baked in enough margin of safety in his plan.

They also plan for a 25% failure ration rather than a 50% failure ratio.

They used a joint and last survivor scheme and planned the scenario that most likely the male will go first and the expense will drop.

However, they did not factor this automatic drop into their plan. This is the second margin of safety.

The third margin of safety is that they could downsize their home and they can do this without worrying their legacy as they have already given their kids their stuff and the kids are not expecting anything further from them.

The Personal Funded Ratio

Don learn this from defined benefit plans.

We compare the amount of money we have versus the amount of money we need.

The key to figuring this out is to figure out the duration of longevity.

For a large group in a pension, this is to figure out the average longevity estimate. For an individual it is to figure out our individual longevity hedge.

For pension, if the money is not enough, the guarantor will put in more money. For his wife and him, if the money is not enough, they take out less.

His wife and his is more of a target benefit fund instead of a defined benefit fund.

The personal funded ratio is how well funded their needs are.

If they are 100% funded, that is good. If it is below 100% then that is not good, and the couple will need to consider action such as cutting back spending.

Ben thinks that the personal funded ratio is very simple to implement.

Advice to people on how to figure out what to do with their time

He recommends the book How to Retire Happy, Wild and Free by Ernie Zelinski.

Don thinks on-call job, on-call career, volunteering, doing things that you are good at will fill time as well.

The 7 Asset Classes of Your Life’s Abundance Portfolio

Don got this idea from a person called Ed Jacobson who was speaking at a conference Don was speaking at.

Ed was talking to financial advisers about how to have useful meetings with their clients.

One of the thing he shared was this life’s abundance portfolio.

This is a portfolo of all the good things in your life that is important to you. By right, we should go through this 7 areas, rate how we did from 1 to 10, just as a check.

How to Assess and Challenge Your Financial Adviser

The first thing we have to do is to explain ourselves to the adviser in a way where we can then apply the financial adviser’s knowledge to us.

A client should not be afraid to confront and say, “I don’t understand. Please put it more simply than that.” or “If that’s your recommendation can you explain to me in a little more detail what it’s based on? Where did that come from?”

When Don was explain to his wife about his 5 years safety bucket plan, he has to explain what its based on, which is history. He also have to explain what if history doesn’t work out. Then they are in trouble and have to adjust.

Make sure that they understand what is your goals and how the things they recommend to you is going to help you get there.

Summary

I like Don’s plan.

The starting point of his strategy is right. The world is uncertain. Longevity is uncertain. Returns are uncertain. Inflation is uncertain.

Knowing that, we then come up with a plan.

He practices liability-driven investing, which is similar to what I have written here. Break things down based on goals. Don’t confuse other things with retirement income.

He breaks his spending into two piles: needs and wants. And he is ready to be flexible about the wants.

His retirement income solution, based upon a two segment/bucket system, is simple as well.

Doesn’t complicate things.

His plan includes using conservative assumptions. That leads to a certain level of oversaving or buffering.

I noted the change in his planning assumptions if he is planning today. In a low return world, we may need to lower the planning assumptions.

I written more on retirement planning and financial independence in the most bottom link below.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

sotidy

Monday 12th of July 2021

Hi Kyith,

I have been following your blog for a number of years and this is the first time I am commenting because I simply love this article and its insights. Thank you so much for the effort and sharing.

Kyith

Wednesday 14th of July 2021

Hi sotidy! Thanks for leaving this comment. Took me almost 8 hours to listen for the second time, process and write this out.

DainBramage

Sunday 11th of July 2021

I like your articles generally but at the same time a lot of them are unnecessarily (super duper) long-winded, and this one is a prime example. A TL;DR would be good to keep readers interested.

I stopped reading after the first 4-5 paragraphs perhaps, because it didn't seem like you were getting to the main points soon.

reader

Wednesday 14th of July 2021

@Kyith, LOL. That was an interesting reply. =)

I watched that podcast and it was definitely one of the best for me especially. His perspectives are so personal and a lot of ideas are very well explained.

Kyith

Sunday 11th of July 2021

Thanks for trying to read. If you didn't get value out of it I hope you do well for your retirement journey.