You may be planning for your retirement.

And you might be thinking about what kind of risks you should be considering in your planning. The common fear is that in the first 5 years of your retirement, you experience a very large draw down of your portfolio.

On Investment Moats, I have highlight the risks of a negative sequence, and the havoc it could do to your retirement. Some friends have asked me: What if you have very good rate of return? Does that mitigate the risk?

Well…. Yes and No.

Because while sequence of return is a big monster to tackle, high inflation seemed to be a bigger monster.

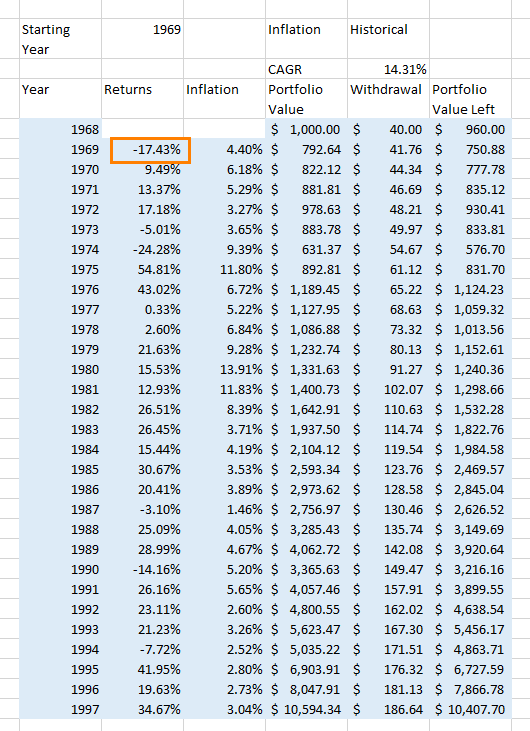

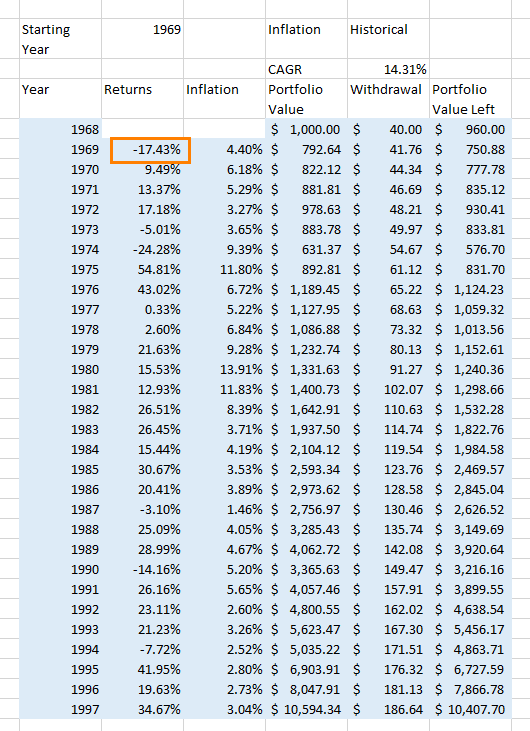

I managed to do some data crunching recently. They told me that the most challenging 30 year period was either 1966, 1968 or 1969.

1969 was a real monster. But the most surprising thing about 1969 after I looked at the numbers was that…. I couldn’t detect what was so bad about this sequence.

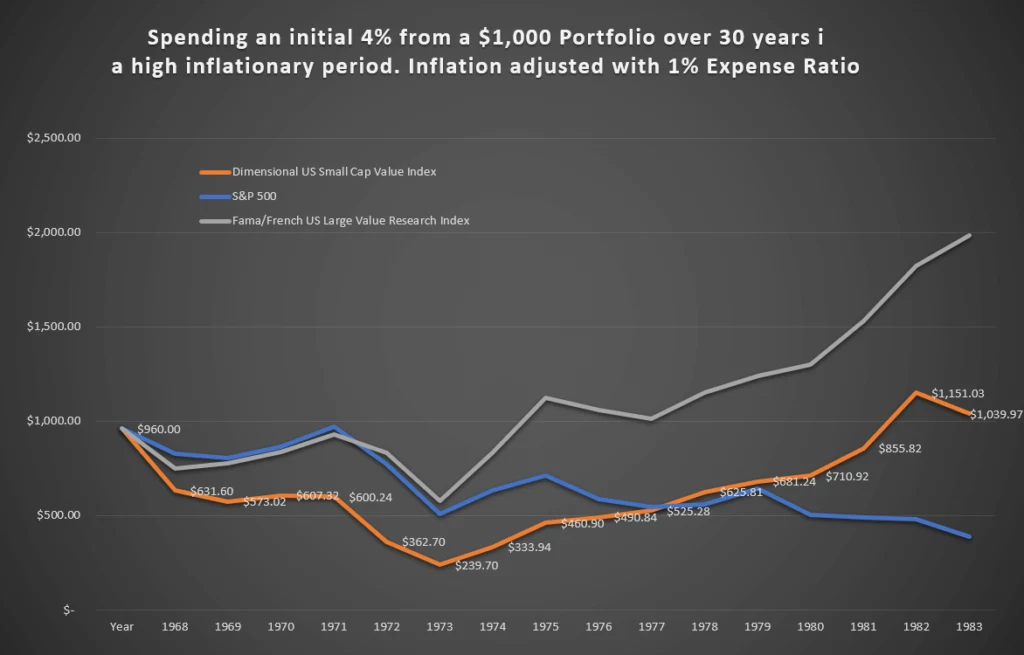

I am going to show you how some indexes perform for the period of 1969 to 1998:

- We factor in a 1% annual expense ratio

- The portfolio is a 100% equity portfolio in that index

- The initial portfolio is $1000 and we will withdraw $40 in the initial year (the 4% withdrawal rate)

- After spending the $40, the year after, we adjust by the inflation for that particular period

We want to see if we are able to spend an inflation adjusted income for the 30 year duration.

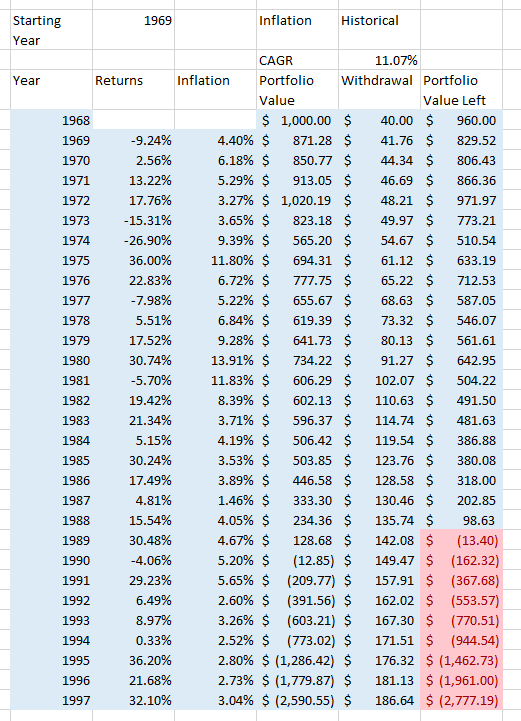

A Pure S&P 500 Portfolio

First up, S&P 500 portfolio. The annual withdrawal rose by high inflation. In 10 years, the spending doubled to $80. In 24 years, the spending have doubled again to $160.

The money was exhausted by 1989.

The compounded average growth for this period is 11.07% a year. That is not… low.

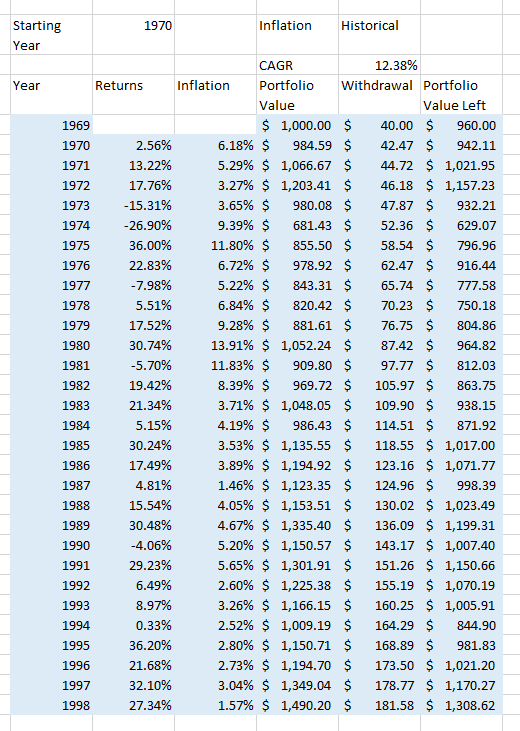

What if the Retiree’s brother retire…. just 1 year later?

Now next, think of the brother of the retiree before, only for this brother, he chose to retire 1 year difference.

His net wealth last him for the full 30 years.

You realize that he went through almost the same high inflation. His compounded rate of return is 12.38%.

How can 1 year difference matter so much??

The whole of 1961 to 1970 was a tough decade. I realize for those years in that decade, you cannot have too big of a negative years in the first 2 years. In those high inflationary years, it is less forgiving.

I do not think anyone would term a -9% return as a very bad sequence. However, this -9% is the difference between a very successful retirement from a not so successful one.

So next, what if your rate of return is high enough?

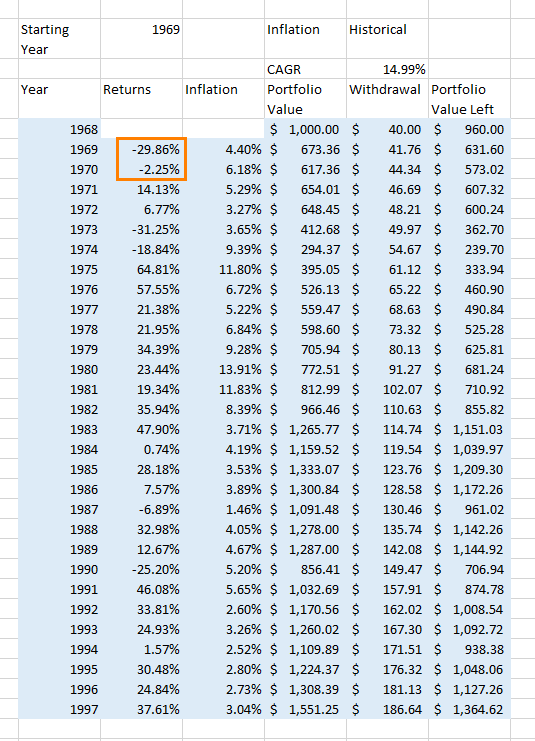

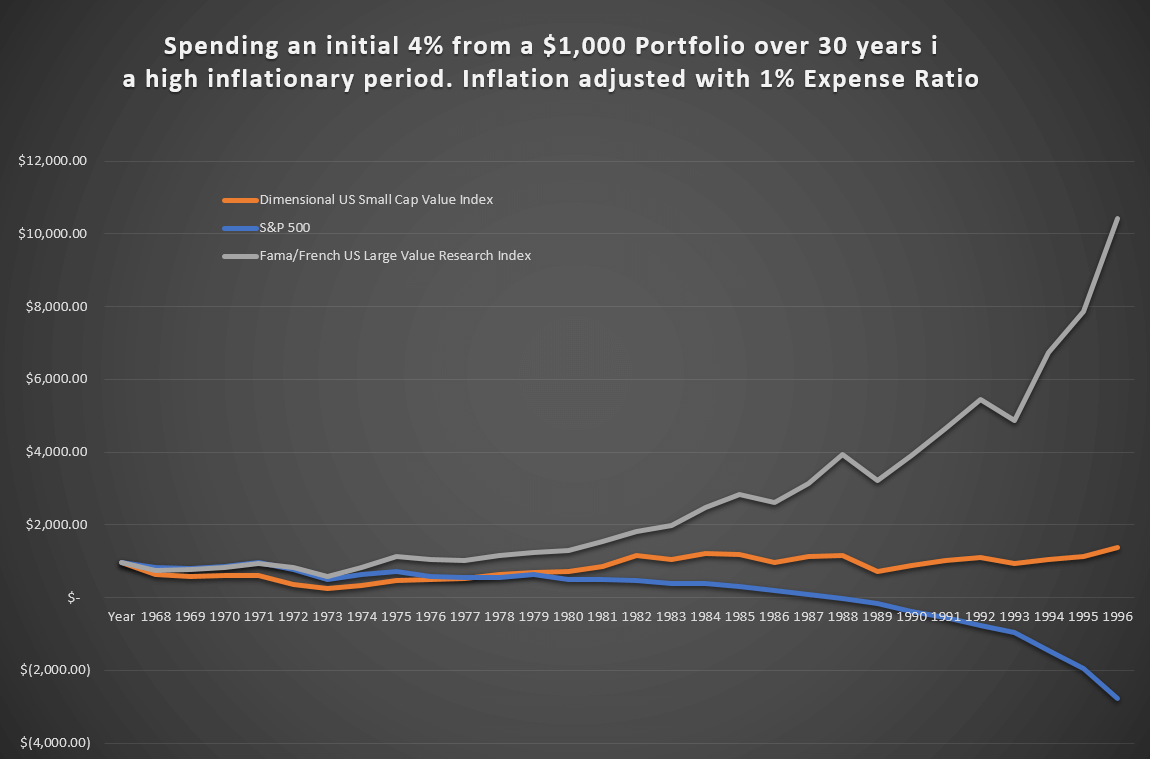

The same time frame but… with Dimensional US Small Cap Value Index

We replaced the S&P 500 with a Dimensional US Small Cap Value index. Small cap and value factors did very well in the past. The compounded average growth is much higher at 14.99% a year (after fees).

Observe that in the same sequence, the small cap value is more volatile than the S&P 500. It dropped almost 30% versus the S&P 500, which dropped almost 10%.

In 1973 and 1974, it dropped a massive 31% and 18%. That is a 44% draw down.

In 1974, the $1000 portfolio dropped to $239.

However, this sequence was able to survive because the growth from this portfolio was crazy.

What about Fama/French US Large Value Research Index?

We have another example of an index that did well. This large cap value index had a smaller draw down but still larger than S&P 500.

This portfolio ended with 10 times as more money as originally started:

- after the high income requirement in this high inflation environment

- after poor negative sequence

Conclusion

1969 was a tough retirement year.

Here is how the three pure equity portfolio stack together. I had initially thought having a great investment return may not alleviate sequence of return risk.

However, if the rate of return is high enough, apparently even if the sequence is poor, inflation is higher, things will still work.

This might make a case of choosing an index that have a high expected returns. It lends weight to the factor tilts of Dimensional Funds available to Singaporeans via MoneyOwl, Providend and Endowus.

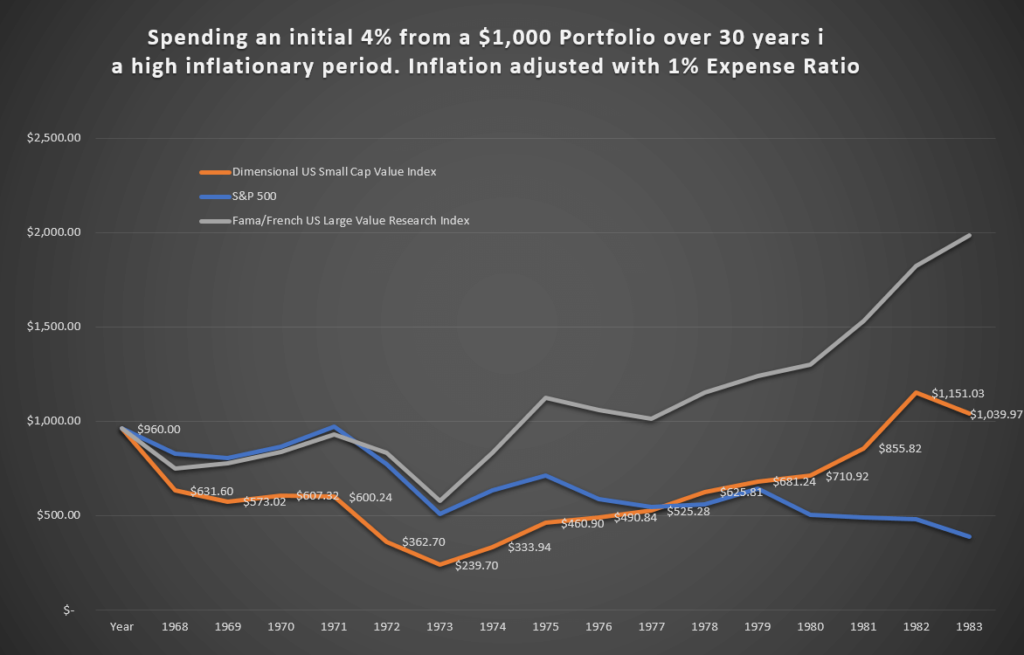

In the chart above we zoomed into the first 14 years.

I do wonder that, if you are in retirement, and you see your portfolio go down from $1000 to $239, will you keep to the plan and not make adjustment?

I think we will make adjustment because this leans very close to failure mode.

In retirement planning, we should view it less as a failure, but that the client will need to adjust his or her spending plan:

- Choose not to inflation adjust the income

- Step down the income by 20% since current withdrawal rate is too high

- Step up the income by 10% or slowly ratcheting up when you have more net wealth and can spend more.

In this way, you can be observe to be proactive and keeping up with the times.

Your plan for retirement is one:

- That you can stick with over a period of time

- And one that you are reviewing enough with someone who knows what they are doing, and adjusting when needed.

Some other take-away:

- 1969 was a bad year because 2 things add up

- High inflation increase your spending so much that it puts pressure on the portfolio

- Just a poorer sequence, although the sequence, by historical standards is actually rather livable for most

- It is hard to simulate this sequence in a Monte Carlo. How do you add up a specific scenario that is high inflation and poor sequence?

- Even if your money will last, there is every chance you will be forced to make stupid decisions

- If your rate of return is high enough, relative to inflation, relative to what you need to spend, it might work out

I will probably talk more about 1969 next time.

My other retirement articles are below in my retirement planning, financial independence page.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- New 6-Month Singapore T-Bill Yield in Late-April 2024 to Drop to 3.70% (for the Singaporean Savers) - April 18, 2024

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

Ming

Saturday 27th of July 2019

Hi Kyith,

Nice article. In actual situation, do you think most people withdrawal adjust according to yearly inflation rate? I think most people would just fix their withdrawal for most of the year and adjust after they found their withdrawal is not enough to support their spend.

Kyith

Saturday 27th of July 2019

Hi Ming, you are right about that. You can view the withdrawal system as you creating your own insurance endowment. it provides u and income while not trying to run out of money. there are much deeper stuff.

but you are right generally u will see if there is a need to increase or decrease your spending. suppose you are 85, it might be ok to take out maybe a higher amount as well.

The important question is what are the boundaries and considerations that we need to take note of.

BlackCat

Tuesday 23rd of July 2019

Hi Kyith,

I think for edge-cases (like 1969), the solution is outside the models. As you said, people will adapt their behaviour and spend less, some people can choose to choose to retire after the market has fallen, work part-time, get income from their children, move across the causeway, etc. The models tell you what can go wrong, so you can plan ahead.

For inflation, no one we know went through anything like the the US wage-price inflation spirals of the 70's: double digit interest rates & salary increments, gold going from 200 to 2000, money value halving in 10 years. We may get it again, with competitive currency devaluations. Holding REITs may guard against this. Gold is too much of a long shot for me.

Kyith

Tuesday 23rd of July 2019

Hi Black Cat, thank you for your comments. I think the difficulty is to say that we can take a job or do something. This is because sometimes we do not know whether we are in a poor sequence or not. What i wish to do is to highlight that there are some situations that... seemingly quite hard to see it is a challenging one.

I think there are a few rule of thumb that works. The main one i think recently is... during the time when you are thinking of pulling the plug, and you observe that the market valuation is not cheap, what it means is that a safer withdrawal rate is actually lower, or you can only withdraw a smaller income. There is a strong relationship between the valuation of the market and how much you can withdraw.

Another point is that i think hyperinflation is losing purchasing power, but people would rather lose purchasing power than to lose their capital or to see their income cut. this is important in the sense that maybe they are ok to not escalate their income so much.

Bob

Tuesday 23rd of July 2019

Hi,

I am never sure on these things.

Does the index include the dividends thrown off? On average the S&P has provided 2% dividend return.

This would make a huge difference, as instead of withdrawing 4% capital each year, only 2% would have to be withdrawn, provided the 4% rate ignored completely the 2% income.

Kyith

Tuesday 23rd of July 2019

Hi Bob, the returns are net of dividends. I think most should look at total returns. When we evaluate this we look at total returns.

Retiree

Tuesday 23rd of July 2019

Hi Kyith,

Are you thinking of switching part of your portfolio to DFA?

Kyith

Tuesday 23rd of July 2019

Hi Retiree, never say never. However, in this case, I can show these because I just so happen to have the data haha.