I think in the past two years, I been getting messages like this on Reddit on-and-off.

I probably did not think much of it but the last one that I received triggered me enough to write this post.

I got these messages due to my past contributions explaining how an endowment plan works.

Many young men and women are recommended these kind of insurance savings plan.

They are in their university. The guys are currently serving their national service.

Some were persuaded by their parents to get an insurance savings plan because it has worked out so well for them.

There were enough that wanted their money to not lose out to inflation and wanted to invest the money.

Many don’t really know what to do with their money and just want to earn a higher return.

For almost all of them, they were persuaded to get a regular-premium insurance endowment plan.

I just think this is a bad idea all-round.

I am saying it is a bad idea not because I hate endowment plans but for a whole host of reason. Let me explain.

What are Regular-Premium Insurance Endowment Plans?

In a nutshell, these are insurance plans that are less focused on insurance protection and more focus on saving and growing your money.

They come in all sorts of fancy names. For a young adult, they might not even be able to tell if they are purchasing an endowment, an investment-linked policy or something else because to a newbie, they do not know what to think.

Generally they go something like this:

- You buy this insurance endowment plan.

- Every month/quarter/year, you have to pay a fixed premium into the plan. This can be a sum like $200 a month, $500 a month, or $1,000 a quarter. This is why it is called regular premium because you pay into it regularly (the opposite is a single-premium which means you pay a single lump sum)

- You don’t stop paying until the maturity of the policy. The period of contribution will depend on your choice. It can be 5, 10, 15, 20, 25 years.

- Upon maturity, you would be able to surrender the policy and harvest a lump sum at maturity. This lump sum would include the bonus accumulated along the way. You can use a mathematical formula called Internal Rate of Return (IRR) to compute the compounded return after contributing to this policy over this long duration.

- Some endowment policies are unique in that it gives regular cashback, after typically 4-5 years. This seems to be a favourite of many because who doesn’t love passive income?

- You can’t stop paying the premiums. If you stop paying, your policies may not lapse immediately. The policy will “lend” money to pay for the premiums that you could not pay and charge you interest on the loan (estimate to be around 6% but could differ). If the policy is unable to lend you anymore, then the policy will lapse.

- If you surrender the policy early, you can get back your premiums. But at a certain point, the amount that you get back will be less than the premiums that you have paid, unless the policy is close to maturity.

So that is a summary of how it works.

Usually, there is life insurance coverage tied to the policy but the coverage is basically very close to the number of premiums you have paid. So if currently, you have paid $4,000 in premiums, your coverage will be close to $4,200.

Many Regretted Buying Insurance Endowment Plans When They Became Financially Wiser.

The 40-year old me had the opportunity to interact with people from all walks of life, of different age group, perhaps more than a 20-year old.

There are enough people that got financially-conscious later in life.

They are able to understand how insurance endowment works better. They also understand that they have a longer time horizon, understand risk and return better, and learn other kinds of financial securities that they can leverage to build their wealth.

Most admitted that they were rather thorn whether to surrender the insurance endowment policy, and take what is left, re-allocate to financial securities that matches their risk profile and time-horizon better.

They have this sinking feeling of needing to continue to contribute into this regular-premium insurance endowment plan even though they do not believe in it anymore.

However, most will still reluctantly continue to pay the premiums due to sunk cost fallacy or just treat this as a lesson learn and this be some future savings that they can re-allocate to other financial goals later in life.

At this point, I would like to say insurance-endowment is not some scam.

There is a defined risk-return profile.

You can read my article on whether your insurance savings plan can give you 3% to 5% returns as illustrated here. In the article, I listed a bunch of matured endowment plans and their returns crowd-sourced from readers.

You will get returns but it is likely due to how endowments are structured, and based on bond returns trend, the future expected returns will be lesser than in the past.

The ultimate regret is this: You are too young to know enough about wealth-building to make a wise decision.

I have seen 17, 18, 20 year-olds that are very financially-concious. They know about stocks, cryptos, FIRE movement, ETFs, robo-advisers all sorts of stuff.

However, enough young adults do not prioritize these money stuff so early in their lives.

They were recommended these products, and are making a purchase decision with a less than equipped financial mind.

The “siong” thing about an endowment plan is that once you commit to it, you tie up that cash flow. If you know what you are getting yourself into (and I mean you read this post, see all my caveat, and think you still want to go ahead), then go ahead and commit.

How Well Does Your 20-Year-Old Self Know your 25-Year-Old Self?

Regular-premium can be a 10, 15, 20, 25-year committment.

The 19-Year-Old you are making this commitment on behalf of the 40-Year-Old you.

You got to ask whether you can make a sound, financial decision that the 40-year-old you would not regret and be proud of.

If you have doubts, then clear those doubts. Learn about finance, and see if you are going to make a wise or poor decision.

My experience is… the 19-year-old Kyith probably didn’t know the level of commitment or how financially-conscious of the 25-year-old Kyith that well.

Refrain from Cash Outflow Commitment Over University

I have people asking me whether it is a good idea to commit to such a savings plan over university.

I mean… don’t you find that risky?

Some of you do part-time tuition, or jobs to earn allowance for your living expenses. You might be able to afford paying this premium.

However, that could change in an instance. I have heard of people whose healthy allowance get cut due to their family situation.

I have also heard of some university students who got so stressed because the study workload (and sometimes personal relationship workload) gets heavy, but they cannot cut back on their part-time job because… they have this insurance premium commitment.

You can cut a lot of your stress by not committing to such a fixed commitment.

Save and Build Your Wealth with a Less Commitment-Heavy Investing Strategy

Now if you want to try and beat inflation or retain purchasing power, select an investment strategy that is more capital-flexible.

You can just buy a single-premium insurance-endowment plan.

Your commitment is just one time, although your money is still locked and will get back less if you surrender in the near term.

Another sensible solution is to go with a robo-adviser and invest in one of their portfolios according to your risk-profile.

I am a bit bias so I would suggest MoneyOwl. The minimum age that can open an account is 18-years-old and the minimum amount to start is $100 so almost anyone can start.

You have a choice of 5 different portfolios based on your risk profile.

They have something similar to the regular-premium insurance endowment system called the regular-savings plan (RSP). You don’t have to opt for that.

This means that if you have $4,000 now, you can just invest $4,000. If you have $250 from your part-time job next time, you can just add $250.

If you face a cash-flow crunch, there will not be a penalty as you are not tied to a RSP plan.

In the event that you need the money, you can sell from the portfolio (although the value will depend on the performance of the portfolio at the time of the sale. The value might be less than your cost.)

Regular Premium Insurance Savings is Not Very Suitable to Use as a Contingency / Emergency Fund

I think before you are investing, you need to keep some spare cash for the unforseen circumstances.

You can read my write-up explaining Emergency Funds here.

Your emergency fund is a pool of money that you want to be able to tap upon whenever you need.

You do not want something that you would have to still contribute money to it when you need to take money out!

The advantage of an insurance policy is that you can borrow against the policy at a relatively high interest rate. If you use it prudently, it is OK.

However, the sensible thing to do is to “save” it in appropriate instruments.

These can be money-market unit trusts like Fullerton Cash Fund or if you want to push it into short-term bonds it could be things like the LionGlobal Enhanced Liquidity.

In any case, all these suggestions do not need you to commit your capital consistently.

You can Decide to Buy Insurance Endowments Next Time

When you are older, after hearing from more perspectives from wiser people, read up more about these stuff yourself, and wish to still buy insurance endowments and contribute on a recurring basis to it, then do it next time.

You are not going to miss out on too much versus the level of flexibility it affords you.

Young adult – no income, some have allowance some do not, have expenses

Young working adult – have income, no allowance, have more expenses

You can reach a state of less cash flow uncertainty if you have income. Although your expenses are likely greater. I would also caveat that there are also adults who are unable to manage their income for the longest time since they start work.

Which brings me to my next point.

Know What You Are Buying

A lot of these products were sold to you.

Good sales people have great sales process to close you.

You won’t be able to discern the real truth so well because you do not know things well enough.

The salesperson may not be lying. They can just fail to disclose vital information or scenarios that would greatly impact your own personal situation.

Sometimes, it is not their fault because the salesperson themselves is less than aware of this!

You need both someone competent and you can trust. These are rare to find.

I would hear my friends tell me they feel safe being with an adviser who is a relative. When I hear the “plan” or products recommended, I just silently shake my head.

If you wish to buy an insurance endowment, go read up about it. While it is not like 1+1 math, I think there are a lot of resources out there for you to form a better picture.

Be able to distinguish a person that is personable versus competent. We tend to gravitate to people that we feel comfortable with. The danger is that a lot of them might be less than competent.

This is applicable for what you see out there in financial Tik Tok. Or even a blogger like myself.

Compound Your Financial Knowledge When You are Young

Now, this is my personal philosophy about young adults and money which you might or might not agree with.

The money that you have at the start is small.

This is especially so when you have not started work. Usually, your 1 year of work income when you graduate is going to be more than the savings up to this point.

So this small amount is not going to matter a lot 30-40 years from now. If your $6000 becomes zero, 30-40 years later, whether you have $6000 or $0, both amounts are not adequate for your financial independence needs or your children’s education.

However, what is going to matter is your financial knowledge. That would compound over time.

If you take this amount and split it into 2 to 3 portions and invest in different ways you can maximise your financial experience and what you can learn about wealth building.

- You can learn about volatility.

- You can observe your reaction when a part of your net wealth experience volatility and how you feel.

- When you have doubts, read-up, find out more about whether you are doing the right ting. Experience and knowledge research are very powerful combination.

The most important thing is that, these knowledge stays with you even at 30-40 years. You do not lose it.

The younger you gain these information, the more they add value to your life:

- What are more fundamental sound securities or strategies.

- How wealth is built and how to implement them when you have the money.

- What you shouldn’t invest in.

- What are absolutely poor financial ideas.

Now, I know there are those of you who have a sizable sum of money when you are young. You got to taper with this suggestion.

Some kids manage to accumulate $100,000 or $300,000 at 21-year-old (don’t ask me how they got it.)

Carve out a portion to experiment and gain knowledge on. Don’t impair all your wealth. My suggestion is do it with $20,000 to $30,000.

For the rest, don’t worry about not compounding well. When you are clearer about what is the fundamental sound way to do, then you can deploy that.

Usually a sound suggestion is to invest in a low-cost, broadly-diversified equity and bond portfolio that is close to your risk profile.

A DIY exchange-traded fund (ETF) portfolio or a robo-adviser solution is not too bad. Again, with these solutions, you do not need to repeatedly commit capital to it.

Break-Even Point to Surrender Policy is Long

If you don’t want to lose the total premiums you paid when you surrender, the break-even point is usually very close to maturity date.

It varies based on the tenure of the policy.

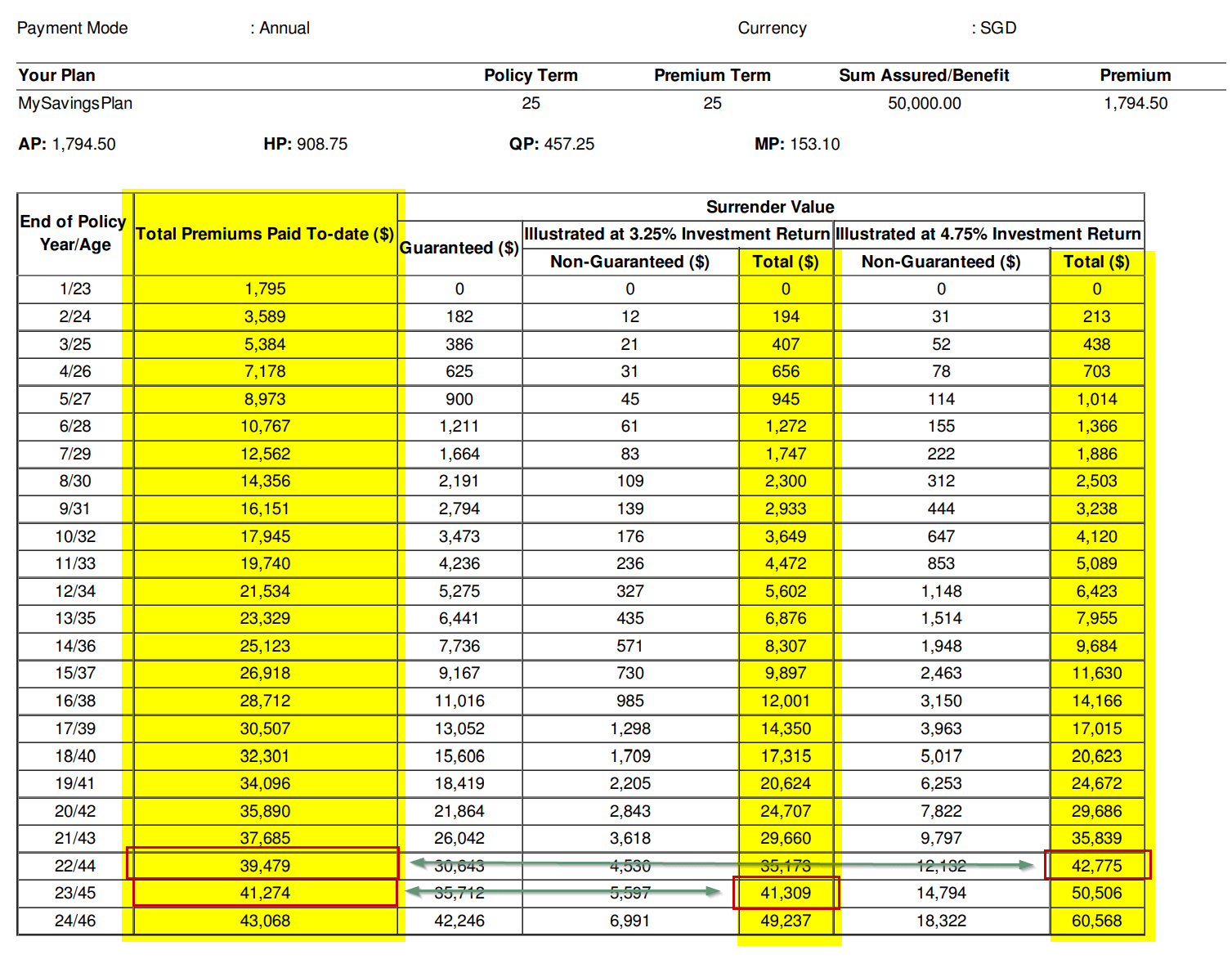

I created the benefits illustration of a 25-year insurance endowment plan for a 21-year old:

This 21-year old will contribute $1794.50 a year for 25 years.

The insurance company usually makes two projected return rate. These are the rate that their participating fund will grow at. Depending on this rate of return, there is a projected surrender value.

The surrender value is the projected value when you surrender.

The two rate of return is 3.25% and 4.75%.

Observe the three highlighted columns. The two columns on the right shows the projected surrender value at 3.25% and 4.75%.

The left column shows the cumulative premiums you paid.

If the rate of return is 3.25%, the break even is at year 23 which is like 2 years before the policy end. If it is 4.75%, it is 22 years.

Basically, if you surrender at most points, the surrender value that you got back is likely less than premiums paid.

Just to be comprehensive, if you put your money in a ETF portfolio or portfolios from robo-advisers, your money is subjected to volatility as well.

This means that if you need the money, and you placed your money in a 50% equity 50% bond portfolio, you might not get back 100% of your value. There are also a possibility that you can get back more than 100% of your capital.

Conclusion

I am making this suggestion based on a very fix young adult profile that I have observed.

Your own situation might be very different.

The general message I wish to drive home is that contributing capital on a recurring basis is a commitment.

You can start this commitment later and not at a young age. You can choose options that allow you to invest lump-sum here and there and not lose out to inflation.

Areas that you can read up:

- Insurance savings plan and endowments.

- Money-market unit trust.

- Short-term bond unit trust.

- Investing in unit trust.

- Low-cost investing.

- Robo-advisers.

Lastly, I wrote a post sharing what I learn in my 30s that I wish to tell my younger 20-something self.

It is filled with suggestions that it might help you make better financial decisions.

You can read it here: My advice to the 20 something on the path to Financial Independence

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- My Dividend Experience Investing in UCITS iShares iBond Maturing in 2028. - April 23, 2024

- We Invest into Popular Funds When They Are Popular, Exactly When They Started Turning to Shxt. - April 22, 2024

- Meal Prep 2.0 – Cooking Your “Go-to” Meal that You Look Forward to Eating Everyday. - April 21, 2024

zach

Thursday 29th of April 2021

Just a point to note is that illustrated investment reuturn is not interest rates earned by the policy, it is the returns of the company of which a lower percentage of interest will be given for the policy if it hits that return for the year.

Kyith

Thursday 29th of April 2021

Hi Zach, thanks for emphasizing on that. I probably said the same thing but perhaps I was less clear.