In my last post on the true reason to choose term life insurance over a whole life, I explained that in order to obtain adequate coverage for a typical family person, it will be quite challenging to do it with solely whole life insurance.

I have gotten a range of feedbacks but generally, some readers were unhappy that my views were so slanted against whole life. There were also comments that stated there were some nuances that I should have considered.

I decided not to sit on the fence because I got sick hearing of all friends and ex-colleagues that were underinsured because they have $XXXX and their personal planners recommended them policies that take away all their cash flows yet not covered enough.

I think I have explained my stance and if whole life is really that great here is something to try.

You know, a common risk of pre-mature death is when a spouse passes away, the surviving spouse will have to take on the burden of the home mortgage.

A common solution is to purchase a mortgage insurance. These mortgage insurance tends to be… a decreasing term insurance.

Now suppose we have a person with $1.7 million in the outstanding mortgage. If you wish to insure such a risk, why not buy whole life insurance that covers you $1.7 million?

Perhaps that is excessive and a spouse should cover 50% of the outstanding mortgage ($850,000 in this example) with cash-value whole life insurance.

Some may argue: “But Kyith, there is a difference between the needs of mortgage insurance and typical life insurance.”

I struggle to see the difference:

- The trigger for both needs is pre-mature death

- The monetary need is a lump sum to alleviate the future cash flow of your dependents. In a mortgage, it is to offset future mortgage payments by paying off the mortgage in a lump sum. In your dependent’s needs, the sum of money offset their future expenses and perhaps some savings

The needs are pretty similar. This is why there are some who may choose to use mortgage insurance to cover the income replacement for their dependents.

If whole life insurance provides adequate coverage, then try covering $1 mil for income replacement and $850,000 outstanding mortgage with whole life insurance.

It is weird why you would choose to use term insurance to cover one aspect of pre-mature death and find it tough to accept treating insurance as an expense for the income replacement portion.

But let’s not discuss this anymore but to more interesting stuff.

The Compounded Return You Get for Using Term Life Insurance As a Savings Plan

One of my friend who happens to be a financial planner wishes to find out what I think about the concept of using term life insurance as a savings plan.

The idea is this:

- The person does not have any dependents already. Thus, he does not need such coverage to hedge the risk of premature death

- He will pass away. It is only a matter of when.

- However, he wishes to set aside money for his heirs.

- His heirs know of #2 and wish to take advantage of this “peculiar human attribute that we will one day passed away”

- So he will buy a term life insurance for 99 or 102 years old with the purpose of leaving money for his estate to be distributed to his heirs

- He will pay for the premiums or his heirs will pay for the premiums

This is basically using the term insurance as a legacy planning tool instead of the traditional universal life plan.

Term plans are generic with a certain set of features.

You can use them to address different needs and your mileage will vary depending on how you use it.

My friend appropriately calls this a “savings plan” and it is funny why he uses that term because traditionally, whole life insurance was framed as a savings plan.

I think he is trying to play down the role instead of treating it as a legacy plan. Usually, people buy universal life because they may want to make sure they “die die” have $5 million to split among their heir.

If you treat this as a savings plan, it makes me feel like the final sum when the policyholder passed away is less important.

What is more important is the rate of return you will get.

- If the policy holder passed away soon, the compounded rate of return is going to be higher

- If the policy holder passed away very late, the compounded rate of return will be lower

- If the policy holder passed away at age 110, there will be only cost and no return!

So this is a bet that the policyholder will pass away before 100 years old. If the policyholder passes away later, then it is “a waste” to have paid all those premiums for that purpose.

How Do the Compounded Returns Look Like?

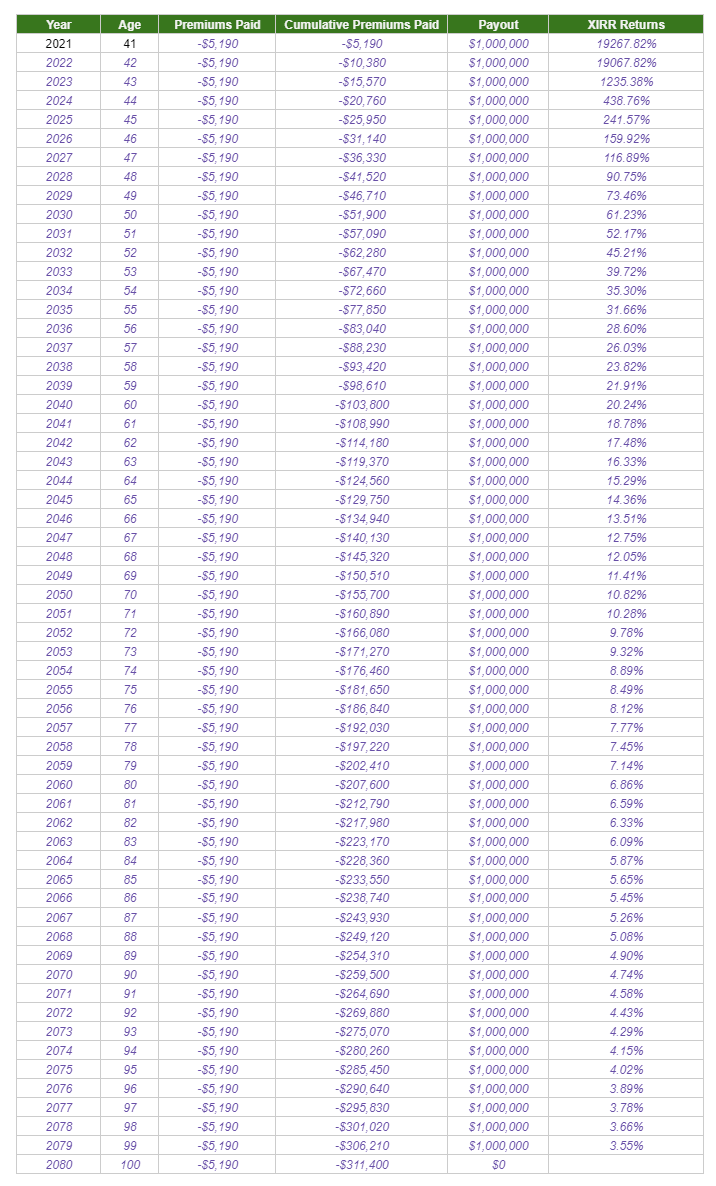

Let us use back the example of John, a person who is pretty similar to Kyith. John is a 40-year-old non-smoker.

John will buy a term life insurance covering him from 41 years old to 99 years old. His annual term life insurance premium is $5,190.

The table below shows the premiums paid over time and the compounded returns measured in XIRR:

The premiums paid by John is constant over the 60 years. If he passes away at any point, his heirs will get a $1 million payout.

If he passes away before 60 years old, his returns are astronomically high relative to the stream of premiums he paid.

What is interesting is that even if he passes away at 99 years, the XIRR return is 3.55%.

If you ask a lot of people today, they wouldn’t mind a savings account that gives 3.55% compounded return over 59 to 60 years.

The return of this payment is contingent on the insurance company issuing the term insurance.

In general:

- The higher probability phase would be after 75 years old

- If you look at the return it is still decent

- Your heirs will claim the money back for you

- It is a sort of legacy planning

Additional Things You Need to Take Note of Framing Term Life Insurance as a Weird Savings Plan

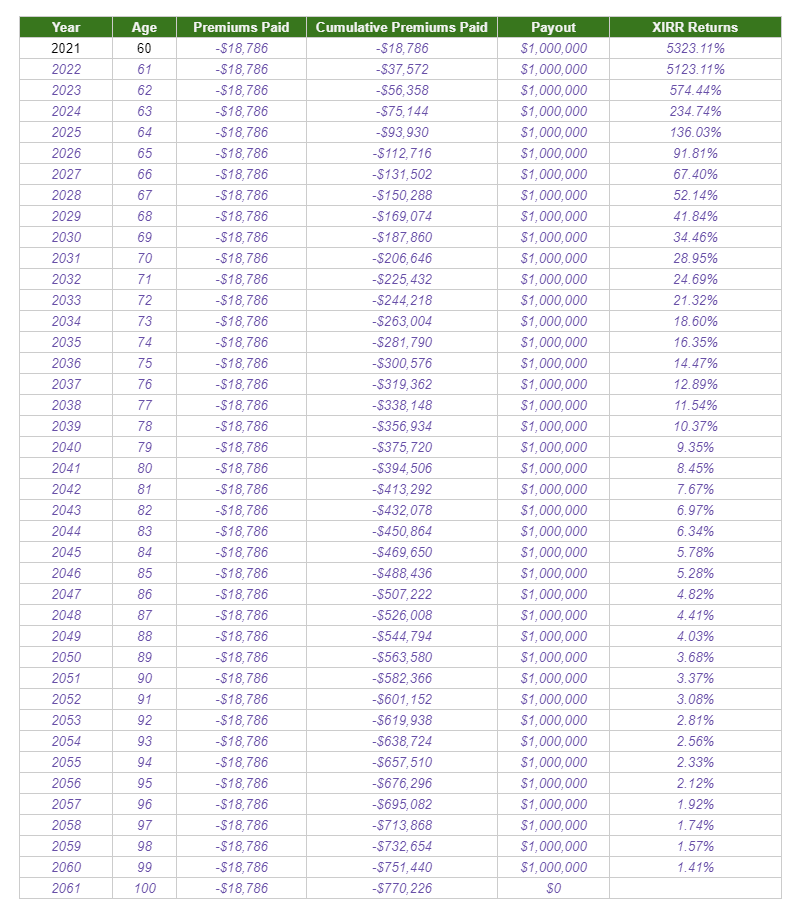

There are caveats to this plan though. Usually, there is a maximum entry age for term life insurance like this.

For NTUC’s Term Life, the maximum entry age is not more than 75 years old (I tried submitting an older one but they will only allow 60 and below for the system).

Your mileage may vary at different entry age. Here is the compounded returns profile if John purchase a $1 million term life insurance at 60 years old:

Some how the returns are less lucrative compared to buying earlier.

If John passes away after 100 years old, then this is not such a good investment.

In general, the premiums are much more expensive. Here are the annual premiums if John (age 40) insures until the following age:

| Insure until this age starting from 40 years old | Annual Premiums | Number of times Premium from $1626 |

| 64 | $1626 | 1 |

| 74 | $2572 | 1.6 |

| 84 | $3819 | 2.3 |

| 100 | $5688 | 3.5 |

In order to do this, you need to be willing to commit additional free cash flow from work income into doing this. Your return will depend on when the policyholder passed away.

The premium difference will be different if the policy holder is younger. Here is the annual premium differences:

| Insure until this age starting from 20 years old | Annual Premiums | Number of times Premium from $680 |

| 64 | $680 | 1 |

| 74 | $1073 | 1.6 |

| 84 | $1511 | 2.2 |

| 100 | $1926 | 2.8 |

The absolute premium looked much lower! But you have to remember that this policy holder also paid 20 year longer in premiums than John.

Lastly, this savings account has a maturity only at the end of a person’s life. You cannot withdraw your money from this savings account at any time.

Thus, it is only applicable if you really know what you are getting yourself into.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

- The LionGlobal APAC Financials Dividend Plus ETF Won’t Give Singapore Investors 5% Dividend Yield Always. Further personal thoughts (with some data). - April 13, 2024

Piscesal

Tuesday 23rd of March 2021

Hi Kyith,

Thanks for sharing this very interesting view on using a Term Life insurance (which is almost whole life) as part of legacy planning. I’m 41 this year and it almost looks as if your “John” scenario was personalised for me and I am very close to considering this. :)

Obviously this is fantastic plan if I die before 70 (almost 11% returns). But assuming the average mortality age of about 85 years for a male in SG, wondering how would the total returns compare if I invest all the money for insurance premiums into a traditional 60/40 passive ETF investment portfolio consistently until i die at 85. The thinking is investing in a passive ETF portfolio may potentially reap greater returns as I don’t have to pay any commission fees to the insurance company for one. Appreciate your views. Thanks!

Kyith

Wednesday 24th of March 2021

HI Piscesal, this plan feels "safer" because the risk is transferred to the insurance company. A 60/40 portfolio's return is determined by the market. your range of return will depend on the market really.

riyu G

Sunday 14th of February 2021

Should inflation be factored in to get a picture of full return of term life plans as well?

Kyith

Sunday 14th of February 2021

Hi riyu G, XIRR only shows the compounded returns. If you wish to factor in inflation, take the XIRR, deduct your desired inflation rate and you will get the real return.

Sinkie

Sunday 14th of February 2021

Yup, I used to have a colleague who mentioned he'd get a pure basic term life & "die die" commit suicide by 80. Said all his relatives & parents died in their 70s. Wants to squeeze as much out of insurance companies as possible on his death. Donate to charity also shiok. I suggested he create a charitable trust in his will with the payout monies. LOL.

Kyith

Sunday 14th of February 2021

Hi Sinkie, that is an interest way to look at things.