A few conversations I observed recently made me wonder about how much investment humility we have when we make investment or wealth decisions.

A person with investment humility generally makes investment and money decision with less overconfidence and pride. He or she would experienced enough vulnerability towards

- What they think they know but actually didn’t know enough

- How certain things are, and how much things will change or will not change

- The limits of their own intellectual and physical capacity versus the intellectual or physical capacity required to do something well

Becoming very Concentrated in their Net Wealth

I came across a conversation in a chat group about the virtues of concentrating your portfolio instead of diversification.

One person shared that many investors adopted to diversify their individual stock portfolio across more stocks, thinking this would make their portfolio safer.

The person believes that if you do deep work on a few concentrated stocks, know their risk parameters well, assess that they have asymmetric risk versus return profile, it is safer to be in a few concentrated positions than be diversified.

Your returns would be better as well with a few concentrated positions.

I think this logic is not wrong. I wrote about how you should frame the level of concentration in your portfolio in this article of my active stock investing series.

Concentrating in your portfolio is safer if you have the investment sophistication to do deep research on investments well.

However, I do wonder how many people can reach that level of investment sophistication. When I asked how many people, I am talking about pulling out from say, a pool of 3.7 million working Singaporeans.

If it is proven that out of 3.7 million working Singaporeans, 30-50% can attain that level of sophistication to run a concentrated portfolio strategy, then I got nothing to say.

I think it is less common for people to use stock investing as their primary wealth accumulation and wealth preservation vehicles. One of the reasons is likely they are less confident as they are less sophisticated.

How ready are the majority of Singaporeans to run a 20-stock portfolio let alone a 5-stock portfolio?

Your net worth is $50,000 and your annual savings from work is $25,000 a year. You can sink $50,000 into 2 stocks.

If you lack sophistication and one of them blows up and left you with $30,000, it is not a catastrophe. In a year’s time, you have new capital coming in. You can learn from this experience and get better.

Now, let us say the same advice is given to someone with a net worth of $1 million. Her future capital injection is $150,000 a year but she is scheduled to stop work in 1 years time.

If the same thing happens and her portfolio is left with $600,000, how would she feel? It is likely to affect her quite a fair bit.

Investment Humility tells us that no matter how well we do our research, there are shitty fat tails. Investment Humility also tells us that you may have the sophistication to do it, but in the spectrum, a lot of people will not or take a long while to reach that sophistication.

I do contend that a lot of people’s sophiscation is not their own but from others. They go to some course trainer to learn investing, but in the end, they depended upon the trainers picks.

The picks have already went through one round of due diligence.

While it is easy to say do your own research and due diligence, these are really unregulated financial advice.

The humility would be to ask yourself: Without help, do you have the confidence to pick 3 to 5 stocks for your $3 million portfolio like Norbet Lou of Punch Card Management (3 positions), Li Lu of Himalaya Capital Management (4 positions), Mohnish Pabrai of Pabrai Investments (2 positions).

Would you have the confidence if you will not have capital coming from work in 2 years time?

Having a High Degree of Trust in Your Financial Adviser

One of my friends told me about his friend. Lets call him Paul.

Paul knows nothing about investment so Paul trusts his friend who is his insurance agent.

Paul’s wealth building becomes saving money and buying insurance through his friend. Through the insurance, Paul will invest in the funds his friend recommends him.

There is no due diligence work done. It is pure trust. (this probably lends weight to the argument how many can build up the rigor and sophistication to concentrate their portfolios again)

I explain to my friend that Paul is a the extreme end of the spectrum where he maybe has so much humility to admit he isn’t good at, or interested in these kind of things to do even some form of investment due diligence.

Paul could end up in a very good or very bad situation.

A lot will depend on whether his trust is placed well or not. In this financial planning world, it is common to find less sophisticated planners. It is also common to find planners whose motivation is not align to yours.

Thus, it is rare to find trusted yet competent advisers.

The investment humility here is to admit that based on the math, chances of Paul finding a trusted, yet competent advisers is rare.

However, based on how the financial compliance is setup in Singapore, the investment humility may be to also admit that the chances of someone’s investment getting cut severely is lesser.

This is because…. in general a person is diversified across many policies (as the person grows older, he or she gets prospected to buy more policies. You can view each policy starting at different periods, thus diversifying across economic regimes)

If Paul finds someone trusted and competent, we should have the humility to admit that Paul may live a better life, free from spending too much time thinking about investments.

Conclusion

I have no problems with people concentrating if I can detect they have the adequate base sophistication and conscientious character to do the work.

I just think that there aren’t many that could do that. I also think there aren’t many that would do that.

Can I do that? Would I do that?

I would say I am weary of my shortcomings, what I don’t know about the markets, what everyone does not know so well about the markets, to be less concentrated.

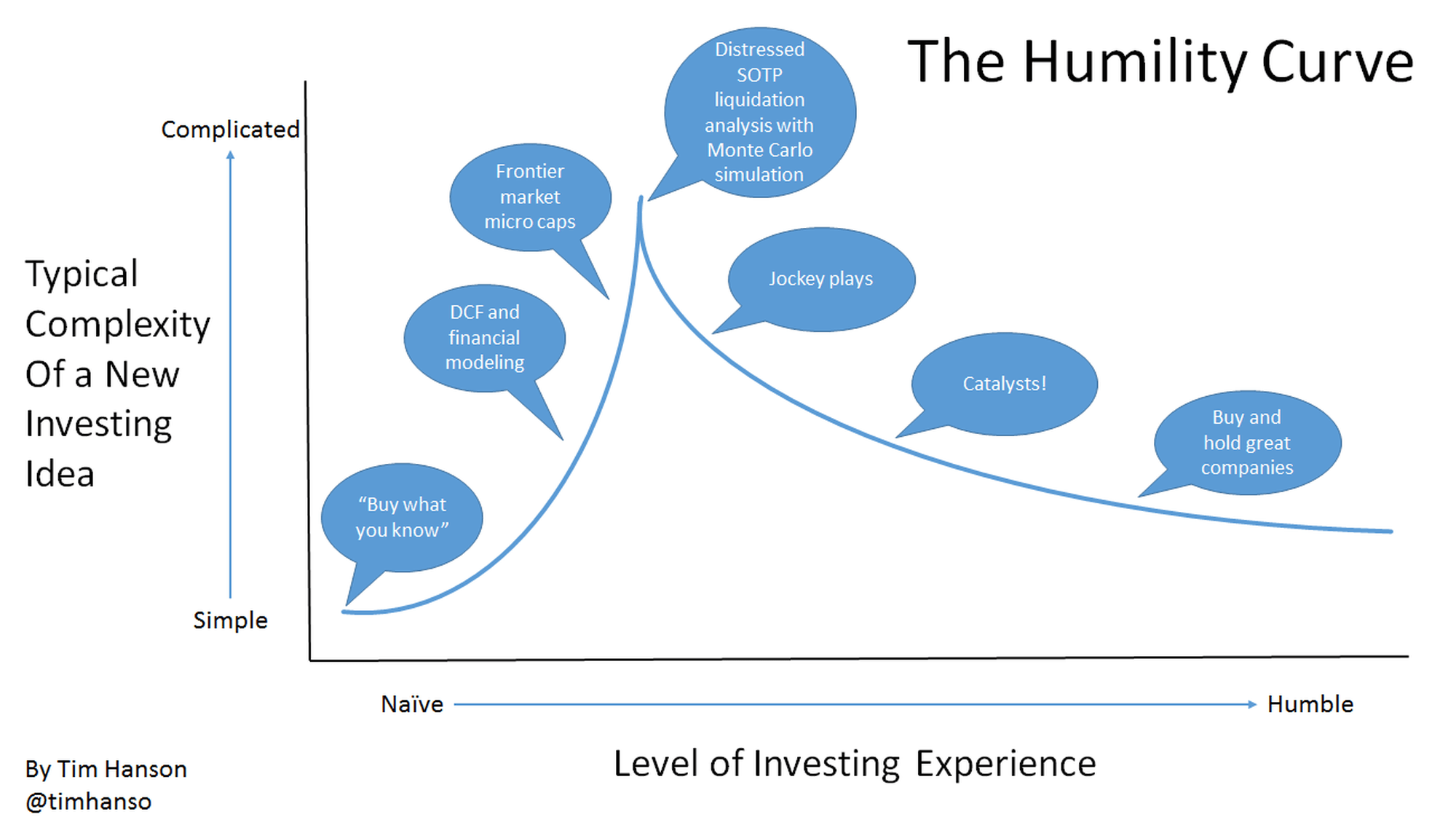

I thought this Motley Fool article on The Humility Curve illustrates that we all thought a lot of complexity in our prospecting is good, but over time, the markets and the environment taught us that we actually do not know a lot. And we should be more humble.

However, I think having humility does not mean using that as an excuse not to pursue some excellence. In all honesty, a person like Paul could have taken a bigger role in his own wealth-building. The world of financial planning has more people watching out for their own interest than watching out for your interest.

What is the moment where you realize you have attained some humility in investment or money management? Share with me here.

I invested in a diversified portfolio of exchange-traded funds (ETF) and stocks listed in the US, Hong Kong and London.

My preferred broker to trade and custodize my investments is Interactive Brokers. Interactive Brokers allow you to trade in the US, UK, Europe, Singapore, Hong Kong and many other markets. Options as well. There are no minimum monthly charges, very low forex fees for currency exchange, very low commissions for various markets.

To find out more visit Interactive Brokers today.

Join the Investment Moats Telegram channel here. I will share the materials, research, investment data, deals that I come across that enable me to run Investment Moats.

Do Like Me on Facebook. I share some tidbits that are not on the blog post there often. You can also choose to subscribe to my content via the email below.

I break down my resources according to these topics:

- Building Your Wealth Foundation – If you know and apply these simple financial concepts, your long term wealth should be pretty well managed. Find out what they are

- Active Investing – For active stock investors. My deeper thoughts from my stock investing experience

- Learning about REITs – My Free “Course” on REIT Investing for Beginners and Seasoned Investors

- Dividend Stock Tracker – Track all the common 4-10% yielding dividend stocks in SG

- Free Stock Portfolio Tracking Google Sheets that many love

- Retirement Planning, Financial Independence and Spending down money – My deep dive into how much you need to achieve these, and the different ways you can be financially free

- Providend – Where I used to work doing research. Fee-Only Advisory. No Commissions. Financial Independence Advisers and Retirement Specialists. No charge for the first meeting to understand how it works

- Havend – Where I currently work. We wish to deliver commission-based insurance advice in a better way.

Kyith is the Owner and Sole Writer behind Investment Moats. Readers tune in to Investment Moats to learn and build stronger, firmer wealth foundations, how to have a Passive investment strategy, know more about investing in REITs and the nuts and bolts of Active Investing.

Readers also follow Kyith to learn how to plan well for Financial Security and Financial Independence.

Kyith worked as an IT operations engineer from 2004 to 2019. Currently, he works as a Senior Solutions Specialist in Insurance Start-up Havend. All opinions on Investment Moats are his own and does not represent the views of Providend.

You can view Kyith's current portfolio here, which uses his Free Google Stock Portfolio Tracker.

His investment broker of choice is Interactive Brokers, which allows him to invest in securities from different exchanges all over the world, at very low commission rates, without custodian fees, near spot currency rates.

You can read more about Kyith here.

- New 6-Month Singapore T-Bill Yield in Late-April 2024 to Drop to 3.70% (for the Singaporean Savers) - April 18, 2024

- Golden Nuggets from JPMorgan Guide to Retirement 2024. - April 16, 2024

- Be Less Reliant on Banks and Build Stronger Capital Markets by Pushing for Better Shareholder Dividend and Buyback Yield - April 14, 2024

retirewithfi

Sunday 24th of January 2021

To me, investment humility is recognizing that the element of luck has a sizable influence on the outcome: https://www.collaborativefund.com/blog/ironies-of-luck/

So my action plan when/if I experience bad luck, ie a bad sequence of returns is important to me. I cannot control the portfolio returns but I can influence the outcome through asset allocation and keeping fees low. And I can control my withdrawal rate. One of the things I do is front-loading low spending: https://bonusnachos.com/front-loading-my-retirement-to-fight-sequence-of-returns-risk/

Kyith

Sunday 24th of January 2021

Thanks for the article retirewithfi, i will read this later.